")

Blue Label Telecoms takes another step towards taking control of Cell C (JSE: BLU)

Getting regulatory approvals out of way is always worth celebrating

Blue Label has announced that Cell C has obtained approval from ICASA for the transfer of telecommunications licences held by Cell C to The Prepaid Company, a wholly-owned subsidiary of Blue Label.

Now, the plan isn’t actually to transfer the licences. They will still be held by Cell C. Instead, they are clearing the way for a change in control of Cell C, which has the same overall effect in terms of ownership of the licence. Blue Label’s plans are for The Prepaid Company to own more than 50% of Cell C, so they are getting the regulatory approval done in the meantime.

This tells you a lot about how tricky these approvals can be.

Reinet had a strong finish to 2024 (JSE: RNI)

Of course, the market is focused on the British American Tobacco sale

Reinet has reported its net asset value (NAV) as at December 2024. They do this every quarter, so one of the metrics they include is the percentage growth between September and December. In this case, they managed growth of 5.1% in that quarter, so it was a great finish to the year.

Reinet also makes a point of reminding the market that the compound annual growth rate (CAGR) is 9.2% since March 2009, including dividends. British American Tobacco has been the underpin of that journey and the big change going forwards is that Reinet has sold all its remaining shares in that company.

A smaller disposal happened in the quarter and therefore impacted the NAV growth in that period. The big clean out happened in January though, so British American Tobacco is still part of Reinet’s NAV as at December 2024 – for the very last time!

In case you’re wondering about the traded discount, the NAV as at December 2024 was EUR 38.12, or around R737 at current exchange rates. Reinet is trading at R453, so there’s a hefty discount here for a company that just turned a big chunk of NAV into cash. The market doesn’t seem to be expecting a special dividend or large buyback here. If Rupert springs a surprise and takes that route, the share price could do some exciting things.

Bash seems to be doing the heavy lifting at The Foschini Group (JSE: TFG)

These numbers don’t look good alongside Mr Price

The Foschini Group (TFG) has released an update for the quarter ended December, which also gives us nine-month year-to-date numbers. Although the third quarter was a positive swing in momentum (group sales growth of 8.4%), the first half was so poor that the year-to-date numbers are still uninspiring with sales growth of 1.6%.

A silver lining is that gross profit is up 5.7% over nine months. That’s still nothing special by any means, but at least gross margin went the right way – especially in TFG Africa.

The gold lining (if you’ll allow me to invent such a thing) is the growth in Bash, the online platform that aggregates the entire TFG offering into a single platform. This approach clearly works, with sales up 47.2% for the quarter and 20.8% year-to-date. Astonishingly, there are still naysayers out there about eCommerce. Online sales are now 11.3% of total retail sales for the group. You really need to have your head in the sand to think that this isn’t relevant.

When we look at the regions, the cracks really start to show. TFG London sales fell 0.1% for the quarter if you exclude the acquisition of White Stuff – and of course, that’s a very important adjustment to make. White Stuff grew sales 18.3% year-on-year, so perhaps that deal will inject some energy into TFG London. TFG Australia was down 3.0% for the quarter.

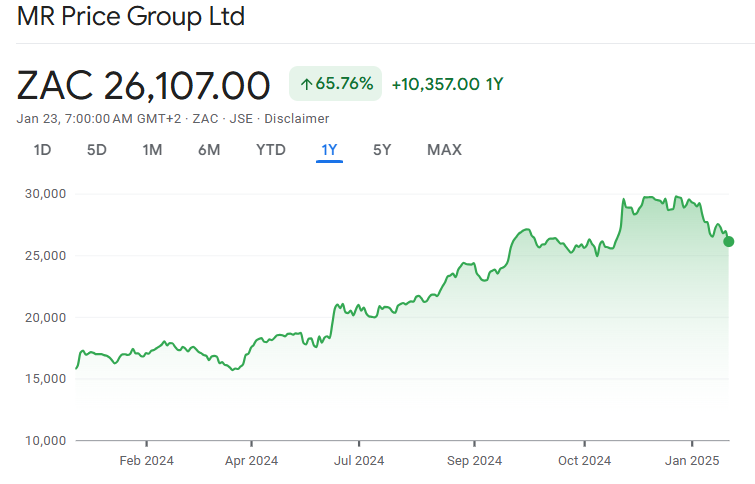

In terms of category level insights, I was surprised to see that Homeware in TFG Africa grew 5.5%, ahead of Clothing at 5.3%. Given the success of the apparel business in Mr Price at the moment, TFG seems to have a pretty serious problem there. Another negative surprise was a 2.6% decline in cellphones, which is also at odds with what we saw from Mr Price. Beauty is the highlight of the TFG offering, up 19% for the quarter. It’s not a fluke, as the year-to-date performance in Beauty is 14.7%.

This performance did nothing to improve the negative sentiment in the sector that has plagued share prices this month, with TFG closing 3.8% lower for the day. The market didn’t even get excited about sales growth in TFG Africa of 14.6% for the three weeks to 18 January, which is clearly a strong start to the year.

TFG is planning a substantial expansion of the footprint this year. Given the underperformance of the bricks-and-mortar offering, I’m not convinced that more is more. It feels like they need to focus on sorting out what they already have and getting the growth up to scratch vs. peers.

York has raised the funding for the Stevens Lumber Mills deal (JSE: YRK)

An increase to an existing term facility got it across the line

Back in June 2024, York Timbers announced the acquisition of several properties (and the trees on them) from Stevens Lumber Mills. One of the conditions related to financing, naturally.

Thankfully, in April 2024, York had entered into a term loan facility with Nederlandse Financierings-Maatschappij Voor Ontwikkelingslanden N.V. (just rolls off the tongue, doesn’t it?) of R350 million. This facility turned out to be the key that unlocks the finalisation of the deal with Stevens Lumber Mills, with an increase in the facility of R75 million.

The York Timbers share price benefitted from the general improvement in sentiment in 2024, with a 12-month performance of 22.2%.

Nibbles:

- Director dealings:

- An executive at Richemont (JSE: CFR) sold shares worth R9 million. Separately, another executive sold shares worth R13 million linked to share options.

- Acting through Titan Premier Investments, Christo Wiese has bought R415k worth of shares in Brait (JSE: BAT).

- A director of Mantengu Mining (JSE: MTU) has bought shares worth R89k.

- As you might expect, various directors of Sirius Real Estate (JSE: SRE) have accepted shares in lieu of dividends under the dividend reinvestment programme.

- I don’t usually comment on changes to major shareholders, but I think it’s worth highlighting that All Weather Capital has rapidly increased its stake in Trencor (JSE: TRE) from 6.66% to 13.29% between 19 December and 22 January. I’m not sure if they held shares before that but it hardly matters – the direction of travel is clear here. Trencor is a cash shell that is due to be wound up in the near future. Perhaps that future isn’t far away now?

- African Dawn Capital (JSE: ADW) announced a deal back in October 2024 that would see EXG Partners invest R5 million in wholly-owned subsidiary Elite group for a 50% stake in that company. They would also provide a loan of R15 million to Elite. The commercial terms seem to have stayed the same, but there’s been a change of ownership in EXG Partners that turns this into a related party transaction as the CEO of African Dawn Capital and his son have now become beneficial indirect holders of EXG Partners. This means that the Category 1 circular will need to be a related party circular and will include all the protections that are needed for minority shareholders, like a fairness opinion by an independent professional expert.

- The latest in the Trustco (JSE: TTO) saga is that the listing has been suspended as Trustco hasn’t released financial statements for the year ended August 2024 in time. Then again, they are currently “trading” under cautionary because they might drop all their listings. This is also the same company that has made noise about wanting to be on the Nasdaq, but can’t get financials out in time. It’s a soap opera.

- AYO Technology (JSE: AYO) finds itself involved in another court action, this time after a minority shareholder with a stake of 0.13% lodged a notice of motion in the High Court to wind up AYO. At this stage, the board believes that this isn’t a price sensitive development, with the company’s legal advisors having considered the claim and its probability of success. Of course, anything is possible. There really is never a dull moment with this company.

")

")

")

")

")

")

")