Reinet lit up the market with an exit from British American Tobacco (JSE: RNI | JSE: BTI)

Reinet just got a whole lot more interesting for me

Aside from my eternal irritation at how British American Tobacco is seen as an ESG-friendly investment (a reflection of absurd ESG rules rather than anything else), I also just don’t like the investment characteristics of the firm. It’s clearly a sunset industry that is built around putting inflationary price increases through on people who struggle tremendously to get off the product. I’ve noticed a strong trend of declining alcohol consumption among my peer group and younger, so you can imagine how few are smoking these days.

Regulators have made it almost impossible for volumes to grow in cigarettes and many regulators hate the “Smokeless World” alternatives just as much. Also, having been around people who vape and use other cigarette alternatives many times in my life, the word “smokeless” is working very hard in the British American Tobacco ESG lexicon.

Still, the company is seen as a rand hedge that pays dependable dividends and offers mid-single digit growth in earnings. There’s demand for that in many portfolios. As for Reinet though, Rupert’s international investment portfolio, that view has now changed.

For the longest time, British American Tobacco has been a cash cow for Reinet. It allowed them to earn dividends and build up investments in all kinds of other areas, including private equity funds. The other core asset in the group is of course Pension Insurance Corporation, another solid underpin that anchored the group over time.

Now, British American Tobacco will no longer be a feature of the Reinet balance sheet. Reinet isn’t just selling down the stake – they sold the entire thing! That’s a casual 24% of the net asset value of Reinet, transformed from shares into cash in a single morning. The markets really are amazing when you think about them.

How was this achieved? A placing with institutional investors of course. JP Morgan was appointed as the bookrunner, which means they picked up the phone to their little black book of major investors and took orders for the shares. Of course, they earned a juicy fee along the way.

The placing has raised £1.22 billion, which gets added to the tally of £148.5 million that was raised in November and December through on-market sales of shares.

All eyes will now be on the use of those proceeds. There are no special dividends coming. Instead, they will be used for “ongoing investment activity” – and one wonders if they have a blockbuster deal lined up!

As for British American Tobacco, this makes no difference to them. Reinet was a small shareholder and this is a transaction between shareholders, not between the company and shareholders.

The all-important Barloworld (JSE: BAW) circular for the take-private deal has been delayed due to the drafting period falling over the festive season. The Takeover Regulation Panel has granted an extension, as the rule is that it must be out 20 days after the firm intention announcement. When I worked in advisory, deals weren’t interrupted by things like holidays. Hopefully things have changed and people are living slightly more balanced lives out there!

The changes to the Murray & Roberts (JSE: MUR) board continue, with Clifford Raphiri resigning from the board. Alex Maditsi has been appointed as the interim chairman. It really is a mess on that side.

Cilo Cybin (JSE: CCC) has released its financials for the six months to September 2024. During this period, the group focused on negotiating the acquisition of Cilo Cybin Pharmaceutical, with the terms of that deal (and the rather daft purchase price) recently announced. So, in the financials, all you’ll find in revenue is interest earned on cash held in escrow from the IPO. As at reporting date, they had just over R60 million in cash on the balance sheet.

Jubilee’s copper production in Zambia was impacted by power constraints (JSE: JBL)

At least there’s a plan going forwards for power at Roan

Jubilee Metals has released an operating update for the six months to December 2024. After Gemfields reminded the market of the perils of Africa (and in this case Zambia as well) based on the reintroduction of an export tax on emeralds, there must have been some nervousness for investors around the Jubilee story as well. Copper may be different to emeralds, but it’s the same governmental exposure.

For now at least, the problems are based on electricity rather than taxes. Copper units produced reached 1,454 tonnes for the six months, way below the revised target of 1,800 tonnes and also down from 1,683 tonnes in the comparable period. This led to a build up in run-of-mine and in-process stock, which they can hopefully catch up on at some point.

An additional power agreement with a new provider should achieve steady supply at Roan, but the agreement is pending regulatory approval. This makes it hard to guess when that could come online. Here’s the problem though: Roan is now under care and maintenance due to the unstable power supply, so this agreement is key to restarting the facility.

As for the Sable refinery, it was thankfully unaffected as it is located in close proximity to the power producer. Production at Munkoyo was also unaffected by power constraints. Still, the uncertainty around Roan means that Jubilee isn’t giving guidance for copper production at this stage.

Moving on to South Africa, the successful commissioning of two further chrome processing units increased production by 35.7%. They are on track for guidance there. The same is true for PGMs.

Jubilee’s share price is down an ugly 46% in the past 6 months. It closed 8.6% higher on this update on a day of strong volumes, so that’s encouraging at least. The worry is the uncertainty of timing around this power agreement for Roan.

Life Healthcare sells the exciting LMI business (JSE: LHC)

At least they have exposure to it possibly being a knockout success in years to come

Generally speaking, value unlocks are great for shareholders when companies either (1) sell a part of the business that the market didn’t like anyway, or (2) sell any part of the business for well above the value that the market was putting on that business. In any other case, selling part of the group just means turning an investment into cash, which doesn’t create value for shareholders in and of itself.

Life Healthcare has been unique in the South African healthcare sector context due to its exposure to Life Molecular Imaging (LMI). This is by far the most exciting part of the group, especially as traditional hospitals aren’t known for being great sources of return on capital. This fact, along with a selling price for LMI that seems to be in line with where the market saw things anyway, is presumably why the Life Healthcare share price barely reacted positively to the news of a sale of LMI. It closed 3.5% higher on the day after initially spiking much higher.

The enterprise value for the deal is $350 million, or R6.475 billion on a cash free and debt free basis (a common structure). Operating profits for the year to September 2024 were $31.6 million. If we use operating profit as a proxy for EBITDA, that’s an EV/EBITDA multiple of 11x. That’s high, but not unheard of for businesses with strong growth prospects. It may well be an EBIT multiple, as companies aren’t consistent in defining operating profit as either before or after depreciation.

The buyer is Lantheus Holdings, who was also the counterparty to the RM2 sub-license agreement reached in June 2024. As part of this deal, the net economic benefit of that agreement will be delivered to Life prior to completion of the deal. Interestingly, it was during the due diligence for the sub-license agreement that Lantheus decided to make an unsolicited offer for LMI.

There are certain things that need to be settled from the proceeds, like LMI management incentives and Life Healthcare’s obligations under a profit sharing arrangement. The net proceeds are therefore expected to be $200 million or R3.7 billion. Life intends to pay a special distribution to shareholders within 12 months of the deal closing. For context, Life’s market cap is R23.8 billion.

Some upside optionality is retained through earnouts and a right to the LMI products in Africa, although it’s not clear how valuable that right really is. As for the earnouts, that’s far more measurable. The first batch runs from 2027 to 2029 and those payments are based on 23% of NeuraCeq net sales in the USA that exceed $225 million. The payments are capped at a total of $225 million for the three year period (it’s confusing that the aggregate payment cap and the annual earnout threshold are similar numbers). There are also potential earnouts in 2034 of $125 million based on Neuraceq global sales and $50 million based on pipeline products.

LMI represented 7.2% of Life’s revenue for the year ended September 2024, so it is a material part of the business. The value of the transaction (R6.475 billion) represents ever so slightly more than 30% of Life’s market cap at the time of the calculation, so this is a Category 1 deal that will require a circular to be issued and shareholders to vote. There are of course a number of conditions precedent as well.

Northam Platinum’s production from own operations has moved higher (JSE: NPH)

They can’t control the price, but they can control production

Adding to a busy day of PGM and chrome updates, Northam Platinum came in with some good news around production volumes. From own operations, they saw a 3.7% increase in refined metal production of PGMs for the six months to December 2024. On the chrome side, production was up 7.5% for the same period.

Interestingly, equivalent refined PGM from third parties fell by a nasty 28.1%. They attribute this to general PGM sector dynamics.

Full-year production guidance is unchanged.

Schroder European Real Estate’s property valuations are under pressure again (JSE: SCD)

Perhaps we haven’t seen the bottom in Europe just yet

After it looked as though property valuations were finally on the up in Europe, the latest numbers from Schroder European Real Estate suggest otherwise. Only the industrial portfolio went the right way (up 2.2%), while the office portfolio fell 2.4% and the “alternative portfolio” decreased by 2.4%, in that case driven by a mixed-use data centre. There is only one remaining retail asset in the portfolio and it fell by 3.2%.

Overall, the direct property portfolio decreased by 0.9%. I couldn’t help but shake my head at Schroder calling this a “marginal decrease” – a drop of 0.9% is material in a market like Europe, especially when it was saved entirely by the industrial portfolio.

Tharisa has a tough start to the year (JSE: THA)

PGM and chrome volumes are down

Tharisa has released a production update for the three months to December 2024, which represents the first quarter of the financial year. Production needed to be strong, as PGM prices remained subdued vs. the preceding quarter and chrome prices came off sharply by 13.7%.

Sadly, production has fallen. The quarter-on-quarter decrease in PGMs is 19.4% and in chrome is 12.3%. That’s no good at all, contributing to a drop in group net cash from $108.9 million to $89.0 million in the past three months.

The reasons? Management references drilling equipment availability and a need to mine sub-optimal areas as a result, with lower grades and recoveries. The focus in the second quarter is of course on addressing this issue.

On pricing, the PGM market continues to struggle and chrome needs to recover, with Tharisa sharing a belief that current chrome prices are unsustainable and will need to increase to reflect the levels of stainless steel demand.

Full-year production guidance is between 140 and 160 koz of PGMs. They produced 29.9 koz in this quarter, so they are behind the run-rate there. As for chrome, guidance is between 1.65 Mt and 1.8 Mt of concentrates. They managed 374.4 Mt in this quarter, so they seem to be particularly behind there.

Tharisa’s share price closed only 2.7% lower on the day. Although it is down more than 22% in the past 6 months, it is actually flat over 12 months.

Director dealings:

The company secretary of Redefine Properties (JSE: RDF) bought shares worth R170k.

Few truisms ring as clear as “high-risk, high-reward” in finance. However, the adage should, in truth, read “higher reward requires higher risk” as risk needs, of course, not deliver returns; but the underlying message remains clear. To assume otherwise would be akin to ordering a free lunch. Despite this, the cost of reward lesson is sometimes forgotten when risk is ignored either through ignorance (where investors indulge in too-good-to-be-true investments) or through design (where clever financial engineering at times hides, without removing, risk – specifically of the systemic kind).

But perhaps it is possible to have one’s cake and eat it. The sweet spot is to construct an index that aims to preserve the upside while limiting the down. It turns out that lower risk doesn’t have to mean lower reward, as we show through our Satrix Low Volatility Equity ETF case study.

The Low-Volatility Signal

We define the low-volatility signal as a composite of price volatility and fundamental risk (e.g., sales and earnings volatility). A high score means a company has a high-risk label compared to other companies. Our research has shown that across several distinct markets (including our own, the US, UK, East-Asian, and Australian markets), the low-vol signal contains no consistent return predictive information over time. This means that more stable companies do not outperform their more volatile companies over time, and vice-versa. What is interesting, though, is that the signal shows very strong predictability of volatility itself – meaning the companies with historically high volatility tend to experience higher realised volatility in future.

This means that using the signal to pick a set of companies to invest in simply does not work – picking only stable companies means investors would very likely experience less risk, but also earn less reward. There’s no free lunch here. But how can we use this signal better?

The Low-Volatility Recipe

In designing a low volatility index, we aimed to harness the strong predictive power of the low volatility signal in predicting future volatility, but not through the traditional means of exclusion.[1] Instead, we use it as a means of tilting (or marginally increasing exposure) towards more stable companies while preserving the inherent structure of the benchmark index. The aim is to share consistently in the market’s upside while limiting the downside by holding proportionally more stable shares. Tilting is, therefore, the key (managing risk), not sub-setting (avoiding risk altogether) – and this makes all the difference.

In designing the low volatility index, we manage portfolio active risk compared to the FTSE/JSE Capped SWIX to be 4%, making it an investable core alternative to the benchmark index. Other controls are also in place to manage single share- and sector risk concentration, turnover, and other portfolio efficiencies. Ultimately, this means the low volatility index is not designed to be the lowest risk equity strategy available but rather to have a similar, albeit lower risk profile than the representative benchmark (Capped SWIX) through time.

The result of this portfolio construction methodology is interesting, and comparable to other global indices that we tested (including the S&P 500, the FTSE 100, German DAX, ASX 200 and the KOSPI indices). When tilting towards lower volatility shares in a risk-controlled manner, both realised volatility and rolling three-year drawdowns are significantly and consistently improved (by around 2% annualised on average).

Importantly, this lower volatility is not achieved by paying away upside. On the contrary, upside beta is largely preserved. And this is the key, as investors compound more over time, not necessarily by finding alpha, but instead by more effectively and consistently avoiding losses. Lowering exposure to higher risk companies in the index (while not excluding them) provides exposure to their upside, while sharing less in their downside.[2] Alpha through effective risk management is less sexy but can be equally as powerful when done right.

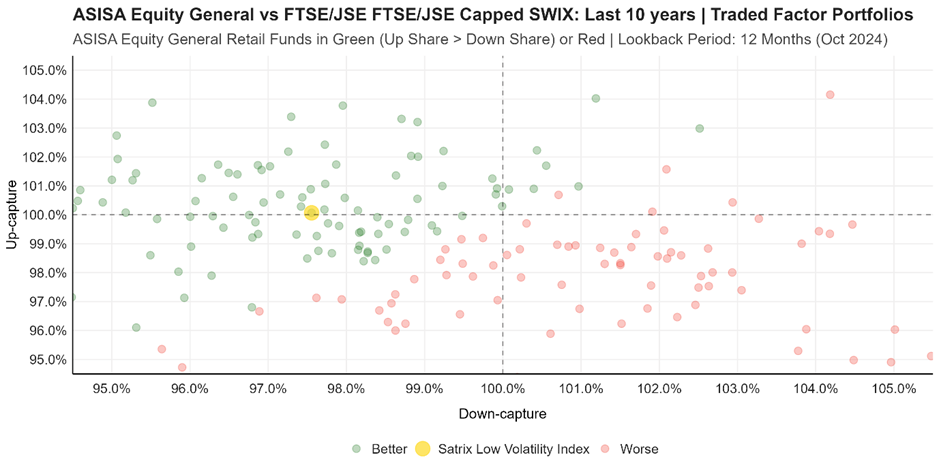

To illustrate the impact of this principle more clearly, we created the following graph that illustrates the “upside vs downside” capture of active local equity managers in the ASISA SA Equity General Category over the past 10 years. For each active manager at each month, we calculate the 12-month upside- vs-downside capture compared to the FTSE/JSE Capped SWIX. Ideally, managers share more in market upside than downside – which is illustrated by colouring such managers green (red implies managers below the 45-degree line, meaning they share proportionally more in downside than upside).

The yellow bubble in the graph shows the Satrix Low Volatility Index. Its ability to preserve beta over this period while sharing significantly less in the downside (below 98% down-capture), is what makes its investment case clear.

Source: Satrix. Data: Morningstar and FTSE/JSE. A methodologically consistent back-test is applied to the Satrix Low Volatility Index. For active managers considered, we strip out fund-of-funds and index tracker unit trusts and control for survivorship bias. We deducted conservative annual Total Investment Charges of 30bps from the FTSE/JSE Capped SWIX Index and 60bps from the Satrix Low-Volatility Index.

The net impact of improved downside risk management is that investors can expect a smoother return profile with less downside while having index-like returns otherwise. Over time, investors can expect to earn more simply by losing less – a powerful investment building block to supplement alpha-seeking strategies.

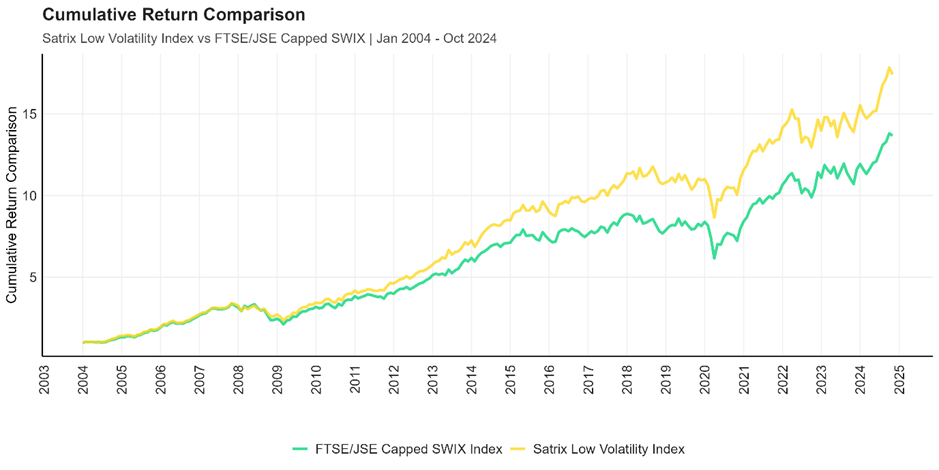

The below graph shows the methodologically consistent back test with a consistent low volatility tilt applied with active risk management compared to the FTSE/JSE Capped SWIX as discussed above.

Source: Satrix. Data: Morningstar and FTSE/JSE. A methodologically consistent back-test is applied to the Satrix Low Volatility Index. We deducted conservative annual Total Investment Charges of 30bps from the FTSE/JSE Capped SWIX Index and 60bps from the Satrix Low-Volatility Index.

Not only do we see lower drawdowns over this 20-year period (lower 78% of the time), but the index also experienced significantly lower realised volatility (just over ~2% less, annualised, on a rolling three-year basis), meaning it had a smoother return profile. It seems that, by systematically reducing (not fully avoiding) higher risk shares, one might after all have one’s cake and eat it.

*Satrix is a division of Sanlam Investment Management

Disclaimer Satrix Investments (Pty) Ltd is an approved financial service provider in terms of the Financial Advisory and Intermediary Services Act, No 37 of 2002 (“FAIS”). The information above does not constitute financial advice in terms of FAIS. Consult your financial adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaim all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information. Satrix Managers (RF) (Pty) Ltd (Satrix) is a registered and approved Manager in Collective Investment Schemes in Securities and an authorised financial services provider in terms of the FAIS. Collective investment schemes are generally medium- to long-term investments. With Unit Trusts and ETFs, the investor essentially owns a “proportionate share” (in proportion to the participatory interest held in the fund) of the underlying investments held by the fund. With Unit Trusts, the investor holds participatory units issued by the fund while in the case of an ETF, the participatory interest, while issued by the fund, comprises a listed security traded on the stock exchange. ETFs are index tracking funds, registered as a Collective Investment and can be traded by any stockbroker on the stock exchange or via Investment Plans and online trading platforms. ETFs may incur additional costs due to being listed on the JSE. Past performance is not necessarily a guide to future performance and the value of investments / units may go up or down. A schedule of fees and charges, and maximum commissions are available on the Minimum Disclosure Document or upon request from the Manager. Collective investments are traded at ruling prices and can engage in borrowing and scrip lending. Should the respective portfolio engage in scrip lending, the utility percentage and related counterparties can be viewed on the ETF Minimum Disclosure Document. For more information, visit https://satrix.co.za/products

[1] Typically, low volatility strategies use a subsetting approach – whereby a selection of companies with the lowest volatility scores are picked. E.g. local strategies have considered the 20 least volatile companies out of a selection of mid- and large caps, which is in line with global index design methodologies too.

[2] This makes sense arithmetically, as the nonlinearity of returns imply a positive 10% return followed by a 10% loss does not equate to parity – instead it is a 1% loss from the initial position. The bigger the loss, the bigger the net impact.

Gullwing doors, fairy curses, cocaine busts and sneaky accounts in Panama. As it turns out, being the world’s most recognisable time machine isn’t even the most interesting part of the DeLorean story. Buckle up, dear reader, because we’re taking a little drive down memory lane – and where we’re going, we don’t need roads.

There was a bit of a fistfight going on in the automotive industry a while ago, and you’ll never guess why. Blame it on retro-nostalgia: not one, but two designs for a modern take on the famous DeLorean were doing the rounds on social media in 2022, getting petrolheads whipped into a frenzy of excitement.

One design was being punted by the DeLorean Motor Company, which bought the right to use the name from John DeLorean after he declared bankruptcy in the late 90s:

The other was championed by Kat DeLorean – John DeLorean’s eldest daughter:

And neither one of these parties wants the other to build their car.

Legal action was threatened in both directions in the early part of 2024, and the stage was quickly set for what looked like a meaty court battle over the DeLorean legacy. And then… crickets. The concept cars have remained concepts, CEOs have come and gone, and die-hard DeLorean fans have been left waiting and wondering if they’ll ever have a chance to buy either car (rumour has it 2025 might be the year).

Then again, real DeLorean fans know that empty promises are as much a part of this car as its iconic gullwing doors.

Let’s start with the man behind the name

John Z. DeLorean was born in Detroit, Michigan in 1925. The eldest of four children, John showed promise early on and was accepted into Cass Technical High School, a school for Detroit honour students, where he signed up for the electrical curriculum. His academic record and musical talents earned him a scholarship at Lawrence Institute of Technology in Highland Park, the alma mater of some of the automobile industry’s best engineers.

Following a number of interruptions – including being drafted into the army during WWII and then moonlighting as a life insurance salesman for a few years – John eventually attended the Chrysler Institute of Engineering. He graduated with a master’s degree in Automotive Engineering and joined Chrysler’s engineering team.

But he didn’t stay at Chrysler for long. After less than a year, John traded Chrysler for Packard Motor Company, and before long he was headhunted from there straight into General Motors. Given his choice of a job in any of GM’s five divisions, John chose Pontiac and made a name for himself by developing cars such as the Pontiac GTO, the Firebird and the Pontiac Grand Prix. His next promotion saw him receive the keys to the Chevrolet castle, and by 1972, he was appointed to the position of vice president of car and truck production for the entire General Motors line.

John seemingly had everything going for him. He was ambitious, intelligent, and his non-conformist style of doing business made people sit up and listen to what he had to say. Everything he touched seemed to turn to gold. But just when it seemed like the top position of GM president was within his reach, he did the unthinkable. He turned his back on GM and went off to start his own business: DeLorean Motor Company.

The long and bumpy road

In the mid-1970s, John DeLorean unveiled his vision for the future of sports cars: the DeLorean Safety Vehicle (DSV), a two-seater prototype with a bodyshell designed by none other than Giorgetto Giugiaro of Italdesign fame. The car would eventually shed its “Safety Vehicle” moniker and emerge as the mononomic DeLorean, complete with its unmistakable unpainted stainless steel body and those gullwing doors that looked like they were borrowed straight from a sci-fi movie. Under the hood sat the “Douvrin” V6 engine, a joint creation of Peugeot, Renault, and Volvo, also known as the PRV.

To bring this steely dream to life, a manufacturing plant sprouted up in Dunmurry, a Belfast suburb, bankrolled bya cool £100 million from the Northern Ireland Development Agency. Renault built the factory, Lotus fine-tuned the chassis and bodywork, and at its peak, over 2,000 workers were churning out cars. The factory went on to produce just over 9,000 DeLoreans, though not without a hefty amount of production delays along the way.

When the DeLorean finally hit the streets in January 1981 – nearly a decade after its inception – it landed with what can only be described as a thud. The timing couldn’t have been worse: the US economy was in a nosedive, and consumers weren’t exactly itching to drop serious cash on a sports car. Even the super-rich were unconvinced. American Express tried to cajole the 1% with an ad for limited-edition DeLoreans plated in 24-carat gold, priced at $85,000 a pop – or around $340,000 in today’s money, which is roughly the current price of a new mid-range Ferrari. The pitch was that only 100 would ever be made. The reality was that only four were sold.

Critics weren’t kind, either. Sure, the doors turned heads, but the steep price and underwhelming horsepower left most cold. By early 1982, the wheels were really starting to come off. More than half of the DeLoreans produced were gathering dust in showrooms, DMC was drowning in $175 million of debt, and the Dunmurry factory was placed in receivership.

In January 1982, the British government uncovered what someone had been trying very hard to hide. Despite producing just 8,500 cars, a staggering £23 million – nearly half the funds allocated to DeLorean back in 1974 – had mysteriously detoured into a Panamanian account under the name “General Product Development Services”. This shell company was allegedly set up to funnel money to Lotus, whose mastermind, Colin Chapman, had helped develop the DeLorean. But the cash never made it to Lotus, and Chapman himself happened to pass away just as investigators started following the money trail. Odd timing, right?

After DMC went into receivership in February 1982, the factory squeezed out another 2,000 cars, but the writing was on the wall. By late October, John DeLorean was arrested on unrelated charges (more on that later). Liquidation proceedings kicked off, and the British government finally seized the ill-fated Dunmurry factory.

According to the Irish locals, the factory was doomed from the start because John DeLorean allegedly destroyed a fairy fort during construction. If true, it’s a classic case of “mess with the fae, pay the price”. So, was it bad business decisions, financial misdeeds, or a vengeful fairy curse that tanked the DeLorean dream? Take your pick.

And then there was the whole cocaine thing

On October 19, 1982, John DeLorean was charged by the US government withtrafficking cocaine. This followed a videotaped sting operation in which he was recorded by undercover federal agents while agreeing to bankroll a massive cocaine smuggling operation.

The operation’s spark came from James Timothy Hoffman, a former neighbour of DeLorean’s who turned FBI informant. Hoffman claimed DeLorean reached out to him about arranging the drug deal, but in reality, it was Hoffman who made the call. Why? Hoffman was facing his own cocaine trafficking charges and figured setting up DeLorean would win him a lighter sentence. Hoffman later admitted that he was aware of DeLorean’s financial troubles before he contacted him, and had heard him admit that he needed $17 million “in a hurry” to prevent DMC’s imminent insolvency.

At trial, DeLorean’s lawyers cried foul, arguing entrapment. They pointed out that Hoffman, a casual acquaintance at best, baited DeLorean into the scheme by preying on his financial woes, with the full backing of the FBI and DEA. The jury agreed, and on August 16, 1984, DeLorean was found not guilty. But by then, the damage was done – DMC was long bankrupt, and DeLorean’s reputation lay in tatters.

A year later, DeLorean faced new charges, this time for defrauding investors and committing tax evasion by allegedly siphoning millions meant for his company into his own pocket. Once again, he walked away acquitted, but by then, his rags-to-riches-to-scandal story was the only thing associated with the DeLorean name. When asked after his acquittal if he planned to resume his career in the auto industry, DeLorean bitterly quipped, “Would you buy a used car from me?”

The closing of the curtain

In 1985, the DeLorean roared back into the spotlight – not for its performance on the road (that was never going to happen), but for its performance on the big screen. Back to the Future transformed the stainless steel wonder into a bona fide cultural icon practically overnight. John DeLorean was so delighted that he wrote to the film’s writer and producer, Bob Gale, to personally thank him for immortalising the car. Talk about a silver lining for a tarnished legacy.

But while his car was traveling through time, DeLorean was stuck fighting his past. By 1999, after battling around 40 lawsuits in the aftermath of his company’s implosion, DeLorean filed for personal bankruptcy and sold the DeLorean Motor Company name to a Texas-based firm that provides parts and professional restoration to DeLorean owners. The fallout also forced him to sell his sprawling 434-acre estate in Bedminster, New Jersey. It was bought by Donald Trump and transformed into agolf course (of course).

DeLorean died from a stroke in 2005, at the age 80. His final years were spent dreaming up and designing a new vehicle, which he called the DMC2. His tombstone shows a depiction of a DeLorean with the gullwing doors open.

Legacy at the crossroads

As we stand at the start of 2025, the future of the DeLorean remains uncertain. The fanbase has responded positively to the idea of an updated car, but the IP battle to get it made promises to be a doozy.

On the one hand, the Texas firm that bought the rights to the name back in the 90s has kept the DeLorean Motor Company alive for two and a half decades. On the other hand, Kat DeLorean has lived with the DeLorean name and its consequences her whole life (she often jokes that the abbreviation DMC actually stands for Destroy My Childhood); she watched her father’s passion for an unsellable idea drag him and their family down to the point of bankruptcy, and she saw him carry dreams of its resurrection to his death. There’s somewhat of an emotional pull in the idea of her continuing the family legacy and righting the wrongs, so to speak.

All we know for sure at the moment is that there are two hands on the chalice and two parties vying to drink from it. Perhaps the biggest irony is that neither knows for sure whether it holds poison or wine.

Would you like to see a return of the DeLorean? And would it make a difference to you whether the car is coming from the daughter of the founder or an unrelated investor? Let us know in the comments!

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.

At exactly the wrong time, the Zambian government has reintroduced a 15% export duty

Nothing makes African governments happier than taking steps to obliterate the few companies that actually operate sustainably, while employing people and paying taxes. It happens over and over and over again across a wide variety of countries on the continent. It’s quite rare these days to see South African companies making a song and dance about plans in the rest of Africa, as there have been many corporate casualties in recent years.

Unfortunately, Gemfields doesn’t exactly have the choice. The emeralds are in Zambia and the rubies are in Mozambique. They have already been trying to navigate a very different political environment in Mozambique, with recent headaches on the emeralds side coming from market conditions rather than specific problems in Zambia. Sadly, there’s now an additional problem: the Zambian government has reintroduced a 15% export duty on emeralds.

Combined with the existing 6% mineral royalty tax, Gemfields’ Kagem business in Zambia now faces an effective tax on revenue of a whopping 21%. Imagine the government knocking your profit margin down by 1,500 basis points with the swish of a pen. For context, other major emerald producers like Brazil and Colombia have total royalties of 2% and 2.5% respectively. Corporate taxes really aren’t that different across the three countries (between 30% and 34%), so the Zambian royalties are now a total outlier.

Worst of all, there was no prior consultation here. At a time when the emerald market is struggling and Gemfields is finding it difficult to sell at sustainable prices, the Zambian government has taking the route of a greedy money-grab.

People often talk about China being uninvestable. Frankly, it’s time to start talking about how the rest of Africa is uninvestable. The returns simply don’t compensate for the risks.

Gemfields dropped another 10% on this news. Just look at how the share price has spectacularly washed away in recent months due to pressures on the group:

There are still question marks around Wesizwe Platinum’s going concern status (JSE: WEZ)

An all-important letter of supportis still in the approval process

Wesizwe Platinum is currently being kept alive by its majority shareholder. There are huge shareholder loans where repayment terms have been extended. In addition, there is a need for further funding for the Bakubung Project.

The majority shareholder has made it clear that the support is there, but there’s a legal process getting in the way. Ongoing support requires approval from the China National Development and Reform Committee and anything that has “committee” in its name is capable of dishing out nasty surprises. Therefore, going concern status isn’t a guarantee until that approval is in place.

They hope to complete the process by the end of June 2025, which is a full six months away. This gives you an idea of how slowly the wheels turn. In the meantime, Wesizwe Platinum shareholders are suffering, with the share price down 40% in the past year.

Nibbles:

Director dealings:

There’s absolutely no liquidity in Deutsche Konsum (JSE: DKR) on the JSE, but I’ll still make mention of off-market purchases by associates of a director to the value of EUR4 million.

There’s a management change at Powerfleet (JSE: PWR), with the Chief Technology Officer having resigned from the group. A Chief Innovation Officer has been hired. In a company like this, these are key roles.

Naspers and Prosus suffer from jitters around Tencent (JSE: NPN | JSE: PRX)

Although there’s no related SENS announcement, this is very important news

Despite all the capital that has been plowed into investments beyond Tencent, the reality is that the Naspers and Prosus valuation is still largely tied to the fortunes of the Chinese giant that made those groups so wealthy in the first place. This means that geopolitical risks are never far away, particularly as US – China relations can be dicey at the best of times. Under Trump, this is likely to worsen.

The latest news is that the US Department of Defense has designated Tencent as a “military company operating in the US” – and that’s not good. In theory, this could lead to Tencent not being able to have its securities traded in the US, where they currently trade on an over-the-counter basis. The bigger issue for South African investors is the extent to which this might lead to international investors trying to get out of Prosus and Naspers, as a sudden sell-off of shares always leads to a sharp drop in price.

Naspers closed over 10% lower for the day, while Prosus fell down 8.4%. Some may see this as an opportunity, as the designation of Tencent as a military company seems very odd. Also, there are examples of companies that have been removed from this list, so we’ve seen this movie before with other Chinese companies. This would then support a rebound in the valuation.

Given all the good work that I’ve seen from new Naspers/Prosus CEO Fabricio Bloisi, I was very tempted by this and I pulled the trigger in the late afternoon. Beyond the capital flows and potential shock reactions, it’s not obvious how this designation impacts Tencent’s business which is focused on China. I’m therefore hoping that the market has dished out a little gift here, although my position sizing was such that I can put in more if it suffers another major sell-off. This is an important technique when buying into an uncertain dip.

Schroder European Real Estate sells an asset in Germany (JSE: SCD)

This is a mature asset with limited scope for further improvement

When it comes to property, some funds talk about “asset management opportunities” as an umbrella term for the initiatives that increase the value of a property. The sky is the limit here obviously, with all kinds of potential projects ranging from improving the parking through to creating better flow of people through the mall.

The end goal is always the same: improve the rental and tenant profile and get a better valuation yield on the property, which equates to a higher value. When this is achieved, it’s usually time to sell the property to someone looking for a more passive investment. The proceeds can then be recycled into new asset management opportunities.

Schroder European Real Estate is the latest example of this, selling a grocery-anchored mall in Frankfurt, Germany for €11.8 million. This is in line with the September 2024 valuation, so that is encouraging for shareholders who need to believe in the company’s disclosed net asset value.

Don’t get too excited about the returns that were achieved here: Schroder bought the property in April 2016 for €11 million. That’s a total capital return of a rather paltry 7.3% over nearly 9 years – in addition to the rentals earned, of course!

Germany simply hasn’t been a great story in recent years.

Nibbles:

Director dealings:

Acting through Titan Fincap Solutions, Dr Christo Wiese has bought a substantial R54 million worth of Brait exchangeable bonds. The bonds specifically trade under the ticker JSE: BIHLEB and should not be confused with the ordinary shares (JSE: BAT).

The company secretary of Datatec (JSE: DTC) sold shares worth R14.7 million.

The company secretary of Redefine Properties (JSE: RDF) sold shares worth R308k. Although this was related to a share award, the announcement isn’t explicit on whether this was purely to cover taxes.

A director of a subsidiary of Capital Appreciation (JSE: CTA) sold share awards worth R32k. There’s no indication of whether this is only the taxable portion, so I must assume that it isn’t.

At Trustco’s (JSE: TTO) general meeting, shareholders approved the resolutions for the Legal Shield Holdings transaction.

Vunani (JSE: VUN) has renewed the cautionary announcement related to the potential disposal of a minority interest in a subsidiary. Negotiations are still underway, so the cautionary has been renewed.

A director and member of the audit and risk committee of Labat Africa (JSE: LAB) has decided not to stand for re-election at the next AGM. It seems to be quite a sudden decision and no reason has been given.

Acsion Limited (JSE: ACS) is moving its listing to the general segment of the main board of the JSE, following in the footsteps of a bunch of small- and mid-caps that did the same thing last year in search of a less onerous regulatory framework.

Catastrophe at ArcelorMittal – the Longs business is being shut down (JSE: ACL)

The impact on areas like Newcastle and Vereeniging will be severe

Remember when the ArcelorMittal share price jumped based on the announcement of stimulus in China? The share price has done crazier things than a heart monitor strapped to someone on a rollercoaster, as you can see below:

Those who made money in the chaos of October were very lucky and those with short positions were hammered. Anyone who was brave enough to be short in the aftermath of that squeeze has now made money from a sudden 31% drop in the price as the news broke of the Longs business finally being shut down.

The effect of this goes far beyond the share price. Many lives are being impacted here in economically vulnerable areas where alternative employment is hard to come by. There are 3,500 direct and indirect jobs that may be affected, with knock-on impacts for those households and the businesses that service them. ArcelorMittal has been warning for a while that this day could come, with efforts throughout 2024 to try and save as many jobs as possible and create a sustainable future for the business. Despite the efforts, including from government, the structural problems in the industry and an ongoing deterioration in global conditions have now made it necessary for ArcelorMittal to pull the plug.

Things will move quickly now, with the wind-down of production expected to be complete in the first quarter of this year. There are nuances of course, like an expected continuation of Newcastle’s coke-making operations. Overall, there is no time to waste, as the muted market response to Chinese stimulus has seen steel prices return to low levels, punished by the extent of Chinese exports that have been flooding global markets. There’s a shocking statistic that ArcelorMittal includes in the announcement to drive the point home: since 2018, steel exports from South Africa are down 40% and imports are up 50%!

Against this backdrop, it doesn’t sound so bad that ArcelorMittal’s revenue is expected to be down “only” 5% in 2024 vs. 2023. The problem is that with such a high fixed cost structure (i.e. the level of operating leverage in the group), this revenue drop is a financial disaster that leads to huge losses. You know the saying of revenue dropping to the bottom line? Well, the loss of revenue also drops to the bottom line in a business like this – just in the other direction.

Although this isn’t reflective of the cash charges, it’s worth noting that the expected cost of asset impairments, wind down and severance charges is R2.7 billion. They don’t give cash guidance in terms of the costs, but ArcelorMittal is obviously working with lenders to ensure that the balance sheet is sustainable going forward.

Note that the words “potential recapitalisation” have reared their ugly heads. This usually means that a rights issue could be coming down the line, if equity holders need to chip in to keep the bankers happy.

With the headline loss per share expected to worsen from R1.70 per share to between R4.06 and R4.41 per share, ArcelorMittal has become an even riskier play. It’s been speculative for a long time now and is a reminder of how dangerous these trades (otherwise known as gambles) can be.

Here’s a chart that may truly shock you:

Nibbles:

Director dealings:

A director of PBT Group (JSE: PBG) bought shares worth R420k.

There’s an awkward start at Cilo Cybin Holdings (JSE: CCC), where results for the six months to September 2024 have suffered an “unforeseen” delay and will only be released on 14 January.

Salungano Group (JSE: SLG) has withdrawn the cautionary announcement related to business rescue proceedings at Keaton Mining. This is because agreements with suppliers and a management agreement in terms of the section 155 compromise proposal have been finalised, so production at Vanggatfontein has recommenced.

A couple of Powerfleet’s (JSE: PWR) subsidiaries increased their facility with a bank from $10 million to $20 million. Although this isn’t exactly big news, it shows that the balance sheets of those entities must be in decent shape if banks are willing to increase facilities.

The chairman of Oando (JSE: OAO), whose official title is very colourful (His Royal Majesty, Oba Adedotun Gbadebo, CFR, the Alake of Egbalan), has stepped down as chairman and retired as a board member. The new chairman is Mr. Ademola Akinrele, SAN – a far less dramatic business card.

Sail Mining Group (JSE: SGP) has withdrawn the cautionary announcement related to a subsidiary of the group. Although this technically means that “shareholders don’t need to exercise caution” when trading in the shares, the challenge is that the shares are still suspended from trading!

Listen to the podcast to get the details on these insights from December 2024:

Is Italtile’s share price a Christmas miracle?

Bloisi’s first acquisition at the helm of Prosus is a fascinating one in Latin America

Renergen was the most interesting announcement in the dead week between Christmas and the new year, revealing yet another risk for the business

Metair’s selling price for the Turkish business has all but evaporated

Bell’s share price may prove to be a cautionary tale about greed, with regret surely kicking in for those who voted against the scheme at R53 per share

The Ghost Wrap podcast is proudly brought to you by Forvis Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Forvis Mazars website for more information.

Listen to the podcast here:

Transcript:

1. Italtile’s share price: a Christmas miracle?

If you’re still looking for a Christmas miracle, then look no further than the Italtile share price. At this stage, I’m more likely to believe in Santa again than in the reasons why this stock is trading at a close to 52-week highs.

Management has given the market nothing but an honest appraisal of the state of play in the manufacturing side of the business – and it’s not good, as South Africa has an overcapacity of tile manufacturers, leading to revenue in that part of the business dropping by a further 1.6% between 1 July and 30 November. That’s after it fell 5.9% in the base period, so that’s particularly ugly over two years.

In director dealings announcements in the past few months, directors have been selling shares, so there’s another strong bear indicator. And if you’re hoping that the retail sales side will give you something to hang onto, then you would need to be happy with just 2.2% growth in system-wide sales.

I can only imagine that investors are hoping for interest rates to drop further and the two-pot system to filter through into home improvement projects. I would remind you at this point that hope is not a strategy.

I’m long Cashbuild in this sector and if you draw a 1-year chart, you’ll see that Cashbuild caught up the performance differential in December very nicely against Italtile:

If Italtile was more liquid, this would be quite the fun pairs trade I think, with my view being long Cashbuild and short Italtile. Instead, I just have to be content with my long Cashbuild position, something that I’m still happy with as we head into 2025 because they do not have a manufacturing side to their business.

As for Italtile, don’t be surprised if there’s a big shock in the market when results are released in March. You certainly can’t claim that management didn’t warn you, all while the share price is close to 52-week highs. It just doesn’t make sense to me.

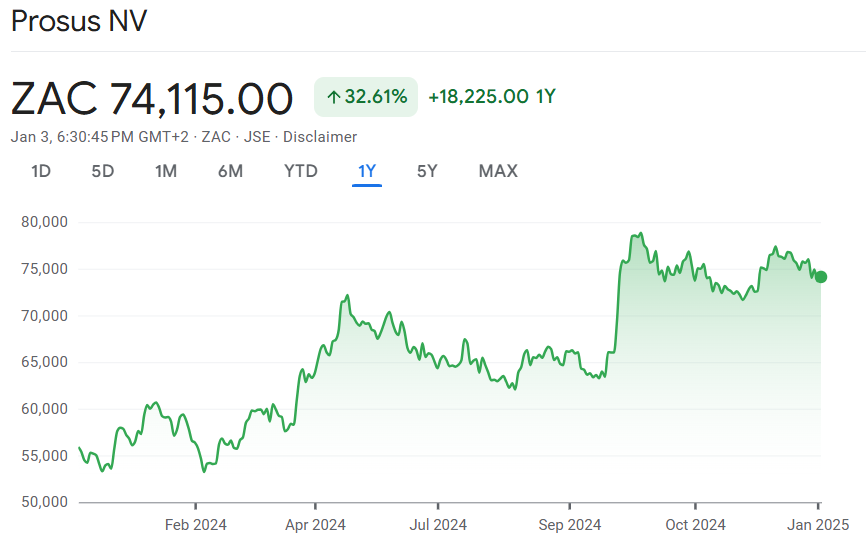

2. Bloisi pulls the trigger on Despegar for Prosus

Just before Christmas, Prosus announced the acquisition of Despegar in Latin America. Now, this is particularly interesting as recently appointed CEO Fabricio Bloisi has tons of experience in that region. That’s where he built iFood, a company that he subsequently sold to Prosus.

This hardcore experience as a successful founder and scaler of businesses is exactly why I’m a fan of Bloisi. It’s not just me – the Prosus share price is up 32% in the past year:

Now, we need to avoid making the mistake that people make all the time in Africa, which is assuming that a continent is actually just one big country. iFood was built in Brazil and Despegar was founded in Argentina. Importantly though, Despegar has scaled across Latin America, so I do think that Bloisi’s Brazilian expertise (and certainly his Latin American network) is helpful here in assessing this deal.

Either way, Bloisi clearly liked what he saw and Prosus is pulling the trigger on a $1.7 billion acquisition for what is described as a leading online travel agency. Weirdly, it suddenly sounds less exciting, doesn’t it? As you imagine Flight Centre at scale and shake your head, consider how valuable it is to have higher income South American consumers constantly on your platform, particularly in a region where the likes of Mercado Libre have shown us how powerful a platform can be.

If you want to be depressed about what Takealot has built vs. what can be built, just take a look at Mercado Libre’s story. Perhaps some of that DNA is in Despegar as well?

In terms of pricing for the deal, Prosus is paying a revenue multiple of just over 2.4x and that’s after offering a 34% premium to the 90-day VWAP (Despegar is listed). I think that’s a reasonable price for a platform in a high growth market. Let’s see how this plays out. This is Bloisi’s first big acquisition in charge and the market will hold him accountable for it.

3. Renergen: here’s another risk to add to the list

Between Christmas and the New Year, Renergen was the only announcement that I felt was particularly interesting. The company’s fight with Springbok Solar is heading to court in February 2025 for an interdict application. This really does seem like a bit of a ridiculous issue right now where someone is behaving badly. Renergen certainly wants us to believe that it is Springbok Solar, and once it gets to court, we will find out for sure.

In the meantime, Renergen needs to run their business and get access to more money for near-term liquidity. They hope to conclude negotiations in the first quarter of 2025 to get their hands on that cash.

Of course, what would help tremendously is if helium production was going smoothly. The latest headache (and yes there is another one) in this regard is that there wasn’t a helium iso container available in South Africa for a direct fill, so there’s yet another risk that you can add to your bear case for this business model. Renergen tried to mitigate this using an onsite storage container and although there were some challenges, they reckon they’ve got a solution now.

The teething issues continue, the company needs money on a regular basis and they have an awkward battle in court on the horizon. Things are never boring at Renergen, that’s for sure.

With the share price down 53% in the past 12 months and recently making new 52-week lows, they desperately need an improvement in momentum and the market will watch each of these issues very closely.

4. Metair is anything but a Turkish Delight

I finish off with cautionary tales and there are two of them. They are both in the industrials space and they are both strong reminders about risk in the markets, something you should always keep in mind.

The first is Metair, where the amount of money they are getting out of Turkey just kept getting smaller and smaller – and then even smaller! In fact, it’s now down to just $1 million, with the potential for it to be $2 million depending on how things play out as the deal closes. When the deal was first announced in September, which is just a few months ago, the price on the table was $110 million! They talked about the price being subject to customary adjustments for working capital and net debt.

Now, such adjustments are indeed customary, because as the balance sheet evolves every single day, you’re not sure how it will look when the deal closes and you make an adjustment at the time – nothing unusual. But what isn’t customary is the rate at which the Turkish business was absolutely obliterating its balance sheet. This is why the purchase price basically disappeared into nothingness. It’s also why Metair took steps to accelerate the deal, before they found themselves in a position where they were paying someone to carry the dead business away.

Owning businesses in faraway lands can be very risky, especially in countries where they have major macroeconomic concerns. With Metair’s share price down 43% in the past 12 months, at least that particular nightmare is behind them. If they can just have a bit of positive luck this year, something they’ve seen very little of recently, perhaps the share price chart can start heading the other way.

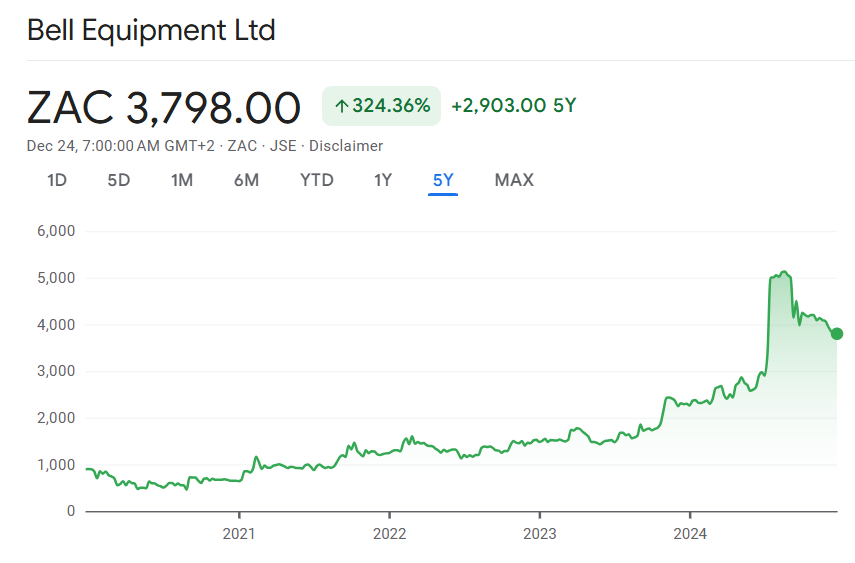

5. Is regret kicking in yet for Bell Equipment shareholders?

The second and final cautionary tale is Bell Equipment, where I am genuinely concerned about where this ends for the minority shareholders who wanted to accept the take-private deal and weren’t able to because the scheme failed.

The price on the table was R53 per share. Currently, it’s trading at just over R40 – well down from there!

An updated trading statement in December gave the unfortunate news that HEPS is expected to be at least 40% lower for the year. This suggests HEPS of up to 478 cents and quite possibly lower. The offer price of R53 would’ve been a forward earnings multiple of 11.1x based on that HEPS number. As HEPS could come in lower, the multiple might have been higher.

Will shareholders who didn’t vote in favour of the scheme end up kicking themselves? Only time will tell of course, but there’s got to be some kind of lesson in here about greed. Even if Bell does get back to those share price levels at some point, the mining cycle will need to play out accordingly and that could take years.

The old adage in the markets is worth remembering as we head into a new year of opportunity: the bulls make money, the bears make money and the pigs get slaughtered.

In 2025, don’t be a pig! Be a bull, be a bear, learn, be as consistent as you can – and most of all, join me for another fun year in the markets!

The future is fixable – at least, that’s what consumers would like to see. Big businesses are still digging in their heels when it comes to open repairs, but new legislation may be increasing pressure soon.

For as long as people have been making things, they’ve also been finding ways to sell us the next version of those things. Take Apple, for example. In the 17 years since the first iPhone launched in 2007, the company has released 29 versions of their flagship smartphone. In late 2017, iPhone users discovered thatolder models were slowing down after iOS updates, sparking accusations that Apple was deliberately throttling performance to drive sales of new phones.

Apple denied this (of course), explaining that the feature was designed to prevent unexpected shutdowns by managing the strain on degraded lithium-ion batteries. To address the backlash, they introduced an iOS update allowing users to disable the throttling feature (though they advised against it) and launched a battery replacement programme, reducing the service cost from $79 to $29 for six months. The catch? Batteries could still only be bought and installed at Apple stores, ensuring that Apple retained its monopoly over every phase of the iPhone consumer’s journey.

From a business perspective, this seems like a great strategy – especially if your business makes expensive goods that could last a long time before needing to be replaced. But how long will cash-strapped, conscious consumers continue to put up with planned obsolescence? And will the growing repair economy (and increasing right to repair legislation) force businesses to rethink their ways?

Made to replace

Though there is no evidence that he was the first to come up with this idea, one of the most influential players in the quick-replacement game was Alfred P. Sloan, an executive at General Motors way back in the 1920s. Alfred didn’t just embrace obsolescence: he turned it into a finely tuned business strategy. Under Sloan’s leadership, GM decided that the best way to keep customers coming back wasn’t just making reliable cars but by making them feel outdated within a year or two. By introducing annual updates to car models, with tweaks to style, features, or performance, GM created a perpetual cycle of desire. Consumers weren’t just buying transportation; they were an antidote to the fear of falling behind.

By constantly dangling the “next big thing” in front of consumers, GM not only drove up sales but reshaped the American car market entirely. Competitor Ford, which had built its empire on the rock-solid dependability and affordability of the Model T, suddenly found itself playing catch-up. Consumers who had once been content with a car that “just worked” were now being wooed by sleeker designs, brighter colors, and features they didn’t even know they needed. GM’s strategy proved so effective that by the 1930s, it had overtaken Ford as the largest automaker in the United States, cementing planned obsolescence as not just a marketing tactic but a cornerstone of modern capitalism.

Ford may have been in the backseat when it came to releasing new models, but they owned the after-sales journey. Back in the 1910s, Ford created a network of certified dealerships and service centers, encouraging customers to use genuine Ford parts rather than turning to independent mechanics or aftermarket suppliers. To tighten control further, Ford pushed for standardised pricing, enforcing flat fees for repairs across their network. It was a win for Ford, but a major headache for small repair shops, which struggled to keep up with constantly changing parts, most of which were exclusively provided to Ford service and repair centres.

In 1947, one enterprising business owner had the bright idea of refurbishing old spark plugs and reselling them. The problem was that he was selling them under a trademarked brand name, which landed him in legal hot water. This case, Champion Spark Plug Co. v. Sanders, would go on to shape the rules for how repaired or refurbished goods could be sold. While the business owner was rapped on the knuckles for copyright infringement, the court’s decision upheld the right to resell repaired or refurbished items, as long as they were clearly labeled to avoid misleading consumers. This ruling laid the groundwork for modern Federal Trade Commission guidelines on resale practices.

Let the people repair

In the early 2000s, the automotive industry successfully shut down the first attempt to pass a right-to-repair bill tailored to its sector. It was a decisive win for car manufacturers, who had little interest in making repairs easier for anyone outside their authorised networks. They pointed to the National Automotive Service Task Force (NASTF), an industry-backed organisation that launched an online directory to provide access to manufacturer information and tools. Progress, right? Not so fast. A study by the Terrance Group revealed that, despite the NASTF, nearly 59% of independent repair shops were still struggling to get hold of diagnostic tools and parts. In short, the directory was more PR than practical help.

Meanwhile, cars themselves were becoming harder to fix. As technology continued to evolve, the share of electronic components in cars skyrocketed, from just 5% in the 1970s to over 22% by 2000. Hybrid cars, while revolutionary, made things even trickier. They required specialised tools and software that manufacturers shared only with their authorised repair services. Independent mechanics were increasingly boxed out, left grappling with limited resources while trying to stay relevant in an industry moving faster than they could catch up.

Despite these challenges, the push for a right to repair didn’t fade. Initially driven by automotive consumer protection agencies and after-sales service providers, the movement soon crossed over into other industries. As gadgets like smartphones and computers became ubiquitous, the demand for repairability gained even more momentum. Even farmers joined the fray, fighting for the ability to fix their increasingly tech-heavy equipment without paying steep fees to manufacturers. Climate change activists weren’t far behind, arguing that repairing products rather than replacing them could help curb the growing e-waste crisis.

What started as a niche debate in the auto industry became a global movement, challenging the idea that manufacturers should hold a monopoly on repair. But the fight was (and still is) far from over.

A long way to go – but some progress on the way

In the United States, 20 states are currently considering legislation aimed at giving consumers more power to fix their stuff. The scope varies – some bills focus on everyday gadgets, while others target farm equipment and cars. Unsurprisingly, the pushback from big players like Apple, Microsoft, and Dyson has been fierce, with lawsuits keeping much of this legislation tied up in courts for years.

Across the Atlantic, the European Union has taken a more decisive approach. A new EU directive now mandates manufacturers to design products with sustainability in mind. Think less waste, lower energy consumption, and easier repairs. Crucially, they’re also required to guarantee spare parts for up to 10 years for products like white goods and lighting. It’s all part of the EU’s broader mission to create a sustainable, circular economy where products are reused, not just tossed away. Down in Australia, the Bower Reuse & Repair Centre is leading the charge for similar reforms. They argue that a truly sustainable future hinges on embracing a circular economy, and at the heart of that is the right to repair.

South Africa may be playing catch-up with the EU when it comes to repairing consumer electronics, but the motoring industry has seen meaningful progress on the right-to-repair front. Thanks to persistent advocacy by the local chapter of the Right to Repair Campaign, the Competition Commission introduced new guidelines in July 2021. These rules are designed to shake up the vehicle repair industry and give consumers more options. Whether you want to take your car to an independent mechanic or roll up your sleeves and handle the repairs yourself, these guidelines aim to make it easier (and fairer) for you to do just that.

With mounting support from consumers, independent repairers, and environmental advocates, the repair economy is poised to reshape how we think about ownership and consumption. The question now is whether industries will adapt willingly or continue to resist as the demand for repairable, sustainable products becomes impossible to ignore.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.

The losses at Accelerate have accelerated (JSE: APF)

At least interest costs have come down thanks to capital raising efforts

Accelerate Property Fund is in a bad space. They’ve had to dispose of assets and raise R200 million through a rights issue to give some support to the balance sheet, yet the loan-to-value ratio has improved by just 100 basis points to 46.7%.

For the six months to September 2024, the headline loss per share worsened substantially from 2 cents to 6.32 cents. This is despite a reduction in finance costs based on the capital raising activities and resultant decrease in debt.

At the moment, lenders are still refinancing the debt – mainly because they believe that they can keep squeezing juicy amounts of interest out of this thing. At least the banks are getting something, as equity holders can’t expect much when you see underlying metrics like a huge vacancy rate of 17.9% at Fourways Mall. Accelerate is working with Flanagan and Gerard as well as the Moolman Group to try and improve things there, but there have been difficulties in getting a contract implemented.

Notably, the BMW Fourways building suffered a negative reversion of 25% after the renewal of a ten-year lease, showing exactly what has happened in the Joburg property market (and the automotive sector) in the past decade. This contributed to the total negative reversion of 7% for the fund.

As should be obvious by now, there is no dividend for shareholders. The share price is down 29% year-to-date.

Dezemba weirdness at AECI (JSE: AFE)

The CFO is on her way out, practically immediately

‘Tis the season for weird SENS announcements and AECI hasn’t disappointed, with news that CFO Rochelle Gabriels is stepping down on “mutually agreed terms” with effect from 31 December 2024.

Ian Kramer has been appointed as acting CFO. He is currently Senior Finance Advisor to the group – a rather odd title that makes it sound like he only has one foot in the door there.

No further details are available at this point. This is the kind of stuff that sets off alarm bells for investors.

Bell’s earnings are falling through the floor (JSE: BEL)

That rejected offer of R53 per share must be a cause of regret by now

When the Bell offer was made and a few activist investors fought hard for it to be higher, I feared at the time that people might live to regret not taking the R53 offer. The share price is currently at around R38 and an updated trading statement for the year ended December doesn’t give us much reason to believe that it will be heading higher from here.

The initial trading statement suggested that HEPS would be at least 25% lower for the year. Now, the company has guided that HEPS will be at least 40% down on last year. This implies HEPS of a maximum of 478 cents and possibly lower.

The take-private offer would’ve ended up being a forward multiple of at least 11.1x for a cyclical group with heavy exposure to the mining industry. Hindsight may be perfect, but there’s also that old story about how the pigs get slaughtered.

This isn’t a chart that I would like to own:

Cilo Cybin: one of the highest valuation multiples you’ll ever see (JSE: CCC)

You might want to be sitting down for this one

Cilo Cybin is a special purpose acquisition company (SPAC) that was set up to facilitate the acquisition of Cilo Cybin Pharmaceutical, a private company that was started in 2018 to focus on the medical cannabis industry. Despite a lot of very impressive paragraphs about their facilities, the net asset value was -R18.7 million as at March 2024 and the loss after tax was R5.9 million.

No matter, because in cannabis startup land, this doesn’t stop the business from being sold to the SPAC for R845 million. And no, there isn’t a missing decimal there. You’ll need to give me something a lot stronger than medical cannabis before I feel comfortable about that valuation.

For the six months to September 2024, things improved to a profit after tax of R13.6 million and a net asset value of R1.3 million. Clearly, the trajectory is strong and the valuation is based on immense growth and a hope that the multiple unwinds quickly. Many startups tend to forget the impact of competition and a slower growth curve as a business matures.

We will have to wait and see what happens here. Forgive me, but paying a 650x price/book multiple is somewhat outside of my comfort zone.

Gemfields takes drastic steps to navigate a difficult market (JSE: GML)

Mining is risky and the mining of pretty things is even riskier

As I wrote some months ago, the back-end of 2024 was absolutely critical for Gemfields. They have been on quite the capex spree, with more planned for 2025. At the same time, prices for emeralds and rubies haven’t really been playing ball, especially in the case of the green stones.

Things have now come to a head, with ongoing problems of oversupply in the emerald market leading to Gemfields taking the decision to suspend production for up to 6 months at Kagem Mining. They will focus on processing ore stockpiles at Kagem while the emerald market hopefully comes right. The problem is that if the Zambian competitor can somehow keep selling emeralds at a discount, then this could get very painful indeed.

The rubies aren’t free of issues either, with fewer premium rubies coming out of the ground in Mozambique recently and worries around civil unrest. Still, construction of the second ruby processing plant is a critical project and it remains on time and on budget, with planned completion by the end of H1 2025. The civil unrest is taking its toll though, with all non-essential capex in northern Mozambique suspended.

That’s not all, folks. They are “assessing strategic options” in respect of Fabergé, a luxury jewelery business that they frankly should’ve sold ages ago. They are also very keen to sell the gold project Nairoto Resources Limitada, going so far as to put contact details in the SENS in case anyone is interested!

Perhaps they should try Facebook Marketplace as well?

Somehow, despite this, the share price closed 10% up for the day. It’s down 44% year-to-date.

Prosus and Naspers deepens exposure to Latin America with the acquisition of Despegar (JSE: PRX | JSE: NPN)

The new CEO knows how the region works and I think it creates a great opportunity

We don’t see enough deals in Latin America by JSE-listed companies. Historically, local executives liked to create emigration opportunities by making acquisitions in places like the UK and Australia. These days, we at least see more of a tilt towards higher-growth markets in the developed world. Yet, for some reason, our execs are scared of other emerging markets despite navigating all the challenges that South Africa throws at them.

Aside from rare examples like Pepkor acquiring Avenida in Brazil a while ago, South Africans tend to limit their exposure to Latin America to watching football games.

Fabricio Bloisi is the man in charge these days at Prosus / Naspers and he knows the region intimately, having been born in Brazil and having built iFood there. So, when the group announces a deal in Latin America, you can be sure that there’s proper on-the-ground experience being applied.

Prosus is acquiring Despegar, Latin America’s leading online travel agency, for $1.7 billion. Now, this may sound like a business model from last century, but they understand platform businesses over in that part of the world, as evidenced by how developed a competitor like Mercado Libre has become. Prosus can find ways to cross-pollinate the various platforms in the group with different service offerings, with access to over 100 million customers in the region.

Despegar generated revenue of $706 million and EBITDA of $116 million in 2023. The deal has therefore been priced at a revenue multiple of just over 2.4x, representing a 34% premium to Despegar’s 90-day VWAP. In my view, that’s really not a bad price for a quality platform business.

Thungela invests further in Australia (JSE: TGA)

They will now have an effective 77.475% in Ensham

Thungela acquired an effective 62.475% in Ensham back in September 2023 in an effort to diversify exposure away from South Africa (and mainly Transnet, if we are honest). I can understand the appeal of a country with working infrastructure.

Although there were critics at the time, mainly because everyone just wanted Thungela to be a cash cow, the board was more interested in creating a group with reasonable risk exposures. Ensham has been a solid performer and is now contributing 35% of the group’s EBIT.

Thungela is now increasing its stake to an effective 77.475%, so that profit contribution can be expected to increase if the good times continue at Ensham and if things don’t materially improve in South Africa.

The structure is that Thungela holds 73.5% in Australian subsidiary Sungela Holdings, which in turn originally acquired 85% in Enham. The other 15% holder in Ensham will now sell to a different subsidiary (Thungela Resources Australia) which is 100% held by Thungela. In other words, the minority holder in Sungela Holdings isn’t getting any exposure to this additional 15%.

One of the benefits of this deal is that Thungela will look to deepen synergies with Ensham, particularly with the external direct shareholder in Ensham out of the way. This includes a desire to open up markets in Japan and Malaysia.

The deal is too small to be categorisable under JSE rules, so there are no further disclosures at the moment.

The PBT Group (JSE: PBG) scrip dividend received a reasonable amount of support in the end, allowing the group to retain more than half of the dividend in cash. The end result was a cash dividend payout of R13.1 million and an issuance of shares to the value of R14.9 million. I’ve included this note in this section as a number of directors elected the scrip dividend alternative and received shares instead of cash.

MAS plc (JSE: MSP) has renewed the cautionary announcement regarding negotiations with Prime Kapital to acquire the 60% interest in PKM Development Limited. The company reckons that contracts should be concluded by the time that results for the six months to December 2024 are released.

Labat Africa (JSE: LAB) is still catching up on its financials, rather hilariously releasing a trading statement for the six months to November 2023 (not a typo) and then the results for that period on the same day. At least they made an operating profit in that period, although the numbers are so old that I’m not sure they are very useful.

Here’s another one catching up on financials: Kibo Energy (JSE: KBO) has released results for the year ended December 2023. Again, not a typo. The company is currently a cash shell, so these results are literally pointless as they relate to assets that aren’t even owned anymore!

Tongaat Hulett (JSE: TON) continues to make progress with the business rescue plan, with the latest update being the sale of the Zimbabwe business to the Vision consortium.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.