Beltone Venture Capital has acquired a 20% stake in Egypt’s digital home and décor brand, ariika. The Series A investment will accelerate the brand’s expansion to Saudi Arabia.

BIO and EDFI AgriFI are co-investing €6 million in gebana Faso to enhance integrated and sustainable food supply chains in the region. gebana Faso is a subsidiary of the gebana Group and specialises in processing and exporting Fair Trade and Organic cashew nuts and dried mangoes from Burkina Faso.

PZ Cussons Nigeria has announced that PZ Cussons Holdings wants to buy out the other existing shareholders at ₦21 per share via a Scheme of Arrangement. The deal is subject to board, shareholder and regulatory approval. PZ Cussons has been present in Nigeria since 1899 and the move is aimed at strengthening and simplifying the Nigerian operations.

Btrust has acquired Nigeria’s Qala, which has been rebranded as Btrust Builders Programme.

Galileo Resources has entered into a joint venture agreement with Cooperlemon Consultancy in respect of the exploration for copper at large scale exploration license 28001-HQ-LEL situated in Northwest Zambia. A series of earn-in and exploration expenditure will see Galileo take a 65% stake in the joint venture.

Global Investments Holding Ltd has acquired a 30% stake in Eastern Company, a tobacco producer in Egypt. The sale will reduce the Holding Company for Chemical Industries’ stake from 50.9% to 20.9% and is part of the Egyptian government’s ongoing programme of privatising state-owned assets. The deal was valued at US$625 million.

Uganda’s Asaak has entered the Latin American market through the acquisition of FlexClub Mexico. The fintech did not disclose the value of the deal.

Nigeria’s Itana has raised US$2 million to push forward its plans to establish a digital free zone. The funding was provided by LocalGlobe, Amplo, Pronomos Capital and Future Africa.

AfricInvest has invested US$40 million in The British University in Egypt. This is one of the largest foreign direct investments in the education sector in the North African country. The funds will go towards the university’s expansion and transformation plans.

Renew Capital Angels has invested an undisclosed amount in Kenyan fintech FlexPay.

Kenyan crypto payments startup, Kotani Pay has closed a US$2 million pre-seed round led by P1 Ventures. Other investors include DCG/Luno and Flori Ventures.

Lagos-based fintech, Anchor, has secured US$2,4 million in a seed round led by Goat Capital. Other investors include FoundersX, Rebel Fund, Pioneer Fund, Y Combinator, Byld Ventures and Future Africa. Since launching in August 2022, the embedded finance fintech has processed more than $550 million in annualised total transaction volumes and achieved a 30% month-on-month growth in revenue.

Sehatech, an Egyptian health insurtech, has raised US$850,000 from A15 and Beltone Venture Capital. The funds will be used to grow the staff contingent and to invest in product development.

Moroccan edtech Smartprof has raised an undisclosed amount of funding from Digital Africa’s Fuze. Part of the funding will be used to help the company accelerate its expansion into West Africa.

To strengthen its ESG agenda, Safaricom, has announced a new multi-billion Sustainability Linked Loan with four banks – Standard Chartered Bank, Stanbic Bank, ABSA Bank and KCB. This is the largest ESG linked loan facility in East Africa and the first Kenya Shilling denominated sustainability linked loan in the market. The loan is valued at KES15 billion, which can be increased to KES20 billion by accordion.

The adoption of sustainability-linked financing (SLF) instruments by borrowers is primarily driven by their growing realisation that these instruments are a valuable tool to achieve their ESG objectives, which outweighs the associated costs.

This was the topic of a recent podcast hosted by Khurshid Fazel, in a discussion with borrowers and a lender.

The banks’ financing decisions shape the economy, so the way that they structure SLF can be used to bring about positive impacts. SLF presents borrowers with an opportunity to embed sustainability into their operations and activities in a manner that promotes accountability. In this way, SLF creates a symbiotic relationship between lenders and borrowers.

Practical examples

Two examples of how SLF was used to achieve impact outcomes are demonstrated by a property group and a diversified industrial group.

The property group secured SLF to install solar PV on the rooftops of its warehouses, for its tenants. The lending bank discussed appropriate key performance indicators (KPIs) and milestones that had to be achieved in order to obtain preferential terms, and the achievement of these targets had to be independently verified. This data helps to give confidence to investors, lenders, and the property organisation that it is following the right path.

The advantages for tenants in this example were not only that the solar PV reduced their energy cost and provided reliable power, but also that some of them have international customers that impose certain sustainability requirements on the companies with which they do business. Taking steps to be a sustainable business can help a business get more contracts. Also, with reliable and relatively cheaper power, tenants can produce more efficiently and price more competitively. The driver of SLF in this case was accountability and commitment. For the borrower, what gets measured, gets done.

In a second case, a diversified industrial group with operations in Africa and Asia has put considerable effort into programmes that epitomise sustainability. This group, which publishes its sustainability KPIs on its website, has taken on four financing instruments that are ‘green’ or sustainability-linked, including a gender bond which is listed on the JSE.

The listing of the gender bond introduced new global investors, enabling the business to tap new sources of funding. Impact investors are looking to invest in companies that contribute to the common good while delivering a return. The gender bond has two goals: transforming the gender ratio of employees and seeking more female-owned businesses to participate in the supply chain. After the launch of the gender bond, female-owned businesses have come forward, instead of having to be searched for. In this example, SLF was used to raise awareness on an important issue for the borrower, and to inspire action on the issue amongst its stakeholders.

Accountability, awareness and action are drivers of SLF

Setting out sustainability KPIs on a public platform means that the world can see them. If a business does not fulfil its commitments, not only will there be a pricing adjustment on the SLF, but the public will be aware that the business fell short, which carries reputational risks. Companies that claim a commitment to sustainability but whose actions do not reinforce the message are likely to be accused of greenwashing.

There are often significant costs for the borrower associated with putting the necessary systems in place to fulfil its commitments, pursuant to the SLF. Firstly, the commitments require buy-in from the whole organisation and key stakeholders, because sustainability touches on many different aspects. Secondly, the sustainability programme must have oversight from the board of directors. A company that thinks carefully about what is important to its stakeholders and community, and tailors its funding and strategy around those objectives, may be better able to achieve its KPIs than one which is merely pursuing sustainability because everyone else is.

Thirdly, a company may already have certain sustainability objectives, but taking on SLF and making its KPIs public is likely to make fulfilment faster and more effective than if the goals are internal, with moveable deadlines. But this comes with reputational risk if targets are missed.

Some borrowers may consider the marginal adjustment on the SLF that is gained by meeting the KPIs agreed with the bank as insufficient to offset the cost of putting measurement systems in place and bringing in verification agencies. But the margin adjustment on the loan does not appear to be the ultimate driver or advantage of SLF. The starting point should be a careful consideration of the levers of sustainability that the business should put in place to drive revenues, keep costs down, and build a brand in the market. Purpose is important, but so is profit.

Setting stretch targets

A borrower has to travel a journey with its lender before reaching the stage of drawing up a term sheet. Some borrowers have established sustainability strategies, but if their targets are not particularly ambitious, the bank is likely to raise the possibility of doing more. In evaluating whether the current targets are ambitious or not, it will look at how the organisation has performed in the last two to five years or against its peer group, and how material its commitments are to its size and power. For some borrowers who do not yet have the building blocks in place, the bank can give advice.

One of the ancillary benefits of setting sustainability targets, taking on an SLF instrument and monitoring progress against KPIs is that it helps to strengthen governance in an organisation. As SLF matures in SA, it will become more regulated – the JSE has already put out sustainability disclosure guidelines – and choosing legal and financial partners who understand the underlying values of SLF will smooth the journey.

Khurshid Fazel is a Partner | Webber Wentzel.

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Africa, the world’s second-largest and second-most populous continent1, has long been seen as a land of untapped potential. However, in recent years, a wave of economic growth and development has been sweeping across the continent, making it an increasingly attractive destination for global investors, poised to benefit from its vast natural resources, youthful population, improving infrastructure and burgeoning middle class. This article will delve into the reasons why Africa continues to hold immense promise, and explore the growth potential that awaits those who are willing to venture into this exciting market.

RAPID ECONOMIC GROWTH

Africa’s economic landscape has been transforming rapidly in the past decade. According to the African Development Bank’s (AfDB) African Economic Outlook 2023 report, several African countries have consistently recorded impressive GDP growth rates, outpacing global averages. While growth on the African continent was impaired by the residual effects of the COVID-19 pandemic, “the continent performed better than most world regions in 2022, with the continent’s resilience projected to put five of the six pre-pandemic top performing economies — Benin, Côte d’Ivoire, Ethiopia, Rwanda and Tanzania — back in the league of the world’s 10 fastest-growing economies in 2023–24”.2 Growth on the continent has been driven by a combination of factors, such as increased political stability, economic reforms, and a growing consumer base. Furthermore, the continent’s middle class has tripled to 313 million people over the last 30 years, according to the AfDB, which will significantly drive consumption and demand for goods and services.

ABUNDANT NATURAL RESOURCES

Africa is rich in natural resources, including oil, gas, minerals and arable land. The continent boasts significant reserves of minerals such as gold, diamonds, copper, cobalt and platinum, among others. With the global demand for these resources on the rise, Africa presents a tremendous opportunity for investors in extractive industries. Additionally, the continent’s vast agricultural potential remains largely untapped, making it an attractive destination for investments in agribusiness and food production. The potential for agri-investment on the continent can be seen by the fact that world cereal yields have increased nearly three times since 1960, but Africa has only increased yields by 90%. As Africa’s population growth outpaced cereal productivity over this period, this has resulted in significant demand locally, with continued potential to secure global off-takers.3

YOUTHFUL AND DYNAMIC WORKFORCE

Africa is the continent with the youngest population in the world.4 This demographic advantage presents both a challenge and an opportunity. By harnessing the potential of its youth through education, skills development, and job creation, Africa can unlock its productive capacity and drive economic growth. Investors can tap into this growing pool of talent and leverage it for innovation, entrepreneurship and productivity gains in various sectors, including technology, manufacturing and services.

INCREASING URBANISATION AND CONSUMER DEMAND

Africa is experiencing rapid urbanisation, with the number of cities on the continent having more than doubled in the last 30 years from 3600 to 7600, with their cumulative population increasing by 500 million people.5 This urban growth is accompanied by a rise in consumer demand, as a growing middle class seeks access to better housing, healthcare, education and consumer goods. The continent’s rising urban population presents significant investment opportunities in infrastructure development, affordable housing, retail, e-commerce and financial services.

INFRASTRUCTURE DEVELOPMENT

Historically, Africa has faced infrastructure challenges, which hindered its economic growth. However, significant progress has been made in recent years to address these gaps. Governments and international partners are investing heavily in building transport networks, energy systems and digital infrastructure across the continent. These investments not only create opportunities for infrastructure-focused investors, but also unlock new markets and facilitate regional integration.

INNOVATION AND TECHNOLOGY

Africa has witnessed a remarkable surge in technology adoption and digital innovation. With limited legacy infrastructure, the continent has leapfrogged into the digital age, embracing mobile payments, e-commerce and digital services. Tech hubs are emerging in various cities, such as, Lagos, Cairo, Nairobi, Cape Town and Kigali, fostering a vibrant startup ecosystem.6 Investment in African tech startups has been steadily increasing, with annual investment between 2015 (US$185 million) and 2023 (US$3,3 billion) having grown by 1,694%.7 Sectors like fintech, agritech, cleantech, edtech and healthtech offer attractive prospects for investors, while it is clear that platform and software businesses are becoming increasingly important to investors.8

FAVOURABLE BUSINESS ENVIRONMENT

Many African countries are implementing reforms to improve their business environments and attract foreign direct investment. Simplified regulations, streamlined bureaucratic procedures and enhanced legal frameworks are being put in place to make it easier for investors to do business. Furthermore, improved political stability and governance across many African nations have created a conducive environment for investment. Governments are increasingly implementing pro-business policies, streamlining regulations, and enhancing transparency. Additionally, regional economic communities, such as the African Continental Free Trade Area (AfCFTA), being the largest free trade area in the world by country participation, are promoting intra-African trade and integration, further bolstering the investment climate and encouraging cross-border trade and investment, with the goal of creating a single market of over 1.3 billion people and a combined GDP of approximately US$3,4 trillion.

UNTAPPED POTENTIAL

Despite the growing interest, Africa remains largely untapped, with vast opportunities for investors. Numerous sectors are ripe for development, including manufacturing, tourism, renewable energy, infrastructure, financial services, healthcare and agriculture. Markets like Egypt, Morocco, South Africa, Nigeria, Kenya and Rwanda, among others, are attracting significant attention from investors looking to capitalise on their potential.

CONCLUSION

Africa’s potential as an investment destination must not be underestimated. The continent’s growing population, expanding consumer market, rich natural resources, improving infrastructure, technological advancements and improving governance provide a solid foundation for investment opportunities. While challenges for investors exist, such as regulatory complexities, infrastructure gaps and political risks, these can be mitigated by partnering with local businesses, conducting thorough due diligence, and adopting a long-term perspective.

Investors who recognise Africa’s potential and are willing to embrace its unique opportunities stand to reap the benefits of being early movers in the next big frontier. Africa’s rise is not a question of ’if’, but rather ’when’. The time to invest in Africa is now, as the continent continues its transformative journey toward sustainable development, economic growth and prosperity.

1.Population in Africa 2020, by country, published by Lars Kamer, June 22, 2023. https://www.statista.com/statistics/1121246/population-in-africa-by-country/ 2.African Development Bank’s African Economic Outlook 2023 report. https://www.afdb.org/en/knowledge/publications/african-economic-outlook 3.David Ndii, December 2022, https://carnegieendowment.org/files/202212-Ndii_-_Africa_Agriculture.pdf 4.According to the United Nations. http://surl.li/jelsr. 5.OECD/UN ECA/AfDB (2022), Africa’s Urbanisation Dynamics 2022: The Economic Power of Africa’s Cities, West African Studies OECD Publishing, Paris, https://doi.org/10.1787/3834ed5b-en 6.According to the World Economic Forum, Nigeria, Egypt, Kenya and South Africa receive 92% of Africa’s investment in technology, which accounts for a third of the continent’s start-up incubators and accelerators. The significant investment in these African countries has led to emerging tech hub cities in each of these countries. 7.The African Tech Startups Funding Report 2022, https://disrupt-africa.com/wp-content/uploads/2023/02/The-African-Tech-Startups-Funding-Report-2022.pdf 8.Lay and Tafese (2023) based on Crunchbase data. (https://iap.unido.org/articles/how-new-wave-tech-startups-driving-development-africa)

Mish-al Magiet is a Director | PSG Capital

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this episode of Ghost Wrap, I looked at some of the more interesting stories in a busy few days of news.

Bowler Metcalf is evidence of how share buybacks can turn financial water into wine.

City Lodge was permanently damaged by the pandemic, but at least the company is profitable again.

Shoprite’s astonishing performance was blunted by Eskom, which means share price performance is also well off where it should be.

The Foschini Group’s trading update reflects the impact of pressure on like-for-like sales, a drop in gross margin and debt on the recent acquisition.

Bidvest’s second half of the financial year was all about generating cash, which was helpful for the dividend payout ratio.

AVI’s results look good provided you exclude I&J, which tells us something about the different segments in the group.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

I discussed Shoprite on Kaya Biz with Gugulethu Mfuphi on Tuesday night:

Aspen takes a step towards filling its capacity (JSE: APN)

The company is focused on landing pharmaceutical manufacturing contracts

Build it and they will come. This is some of the worst business advice ever given to startups, with Aspen experimenting with this strategy at scale. The recently expanded sterile manufacturing capacity is ready to go and needs contracts for it to generate revenue and a return on the investment, especially after the COVID vaccines fizzled out.

Aspen has announced the fourth such contract, in this case with an unnamed multinational pharmaceutical group to manufacture medicine for a chronic disease. They really are as vague as that, so this agreement clearly comes with some pretty strong NDAs.

With R6 billion having been invested in the facility in Gqeberha, investors won’t really care what the product does, as long as its legal! Aspen can manufacture a variety of drugs at this facility and has positioned itself as a manufacturing gateway to Africa for global pharmaceutical players.

Calgro M3 has a good news story for shareholders (JSE: CGR)

A trading statement has flagged a 20% jump in HEPS

Trading statements range from being light on details through to giving a detailed operational update. The Calgro M3 announcement is the former, simply flagging a jump in HEPS and confirming that results will be released on approximately 16 October.

The company expects HEPS for the six months ended August to be at least 20% higher than the comparable period. This implies HEPS of at least 68.40 cents for this interim period.

I must remind you that the minimum change that triggers a trading statement is 20%. When a company releases such a bland trading statement with “at least 20%” as the guidance, it can literally mean anything from 20.1% through to any number you can imagine. Some companies release a “further trading statement” and others just hit you with the results.

Time will tell how this one pans out.

Capital & Regional completes the Gyle acquisition (JSE: CRP)

This looked like a solid acquisition to me

In August, Capital & Regional announced the acquisition of The Gyle Shopping Centre in Edinburgh for £40 million. The asset has been acquired at a net initial yield of 13.51%, which seems like an attractive price. The debt is being provided by Morgan Stanley at a fixed cost of 6.5% for 5 years.

To get the deal done, the company raised equity capital on the local market. This has sadly become a rare occurrence in South Africa, with very few companies tapping the local market for growth capital.

With an underwrite from controlling shareholder Growthpoint (JSE: GRT), Capital & Regional raised the capital and the acquisition has now become effective. This is a good example of a grocery-anchored community shopping centre, which fits right into the company’s strategy. The company also highlights the opportunity for active management of this asset, improving income and thus the valuation.

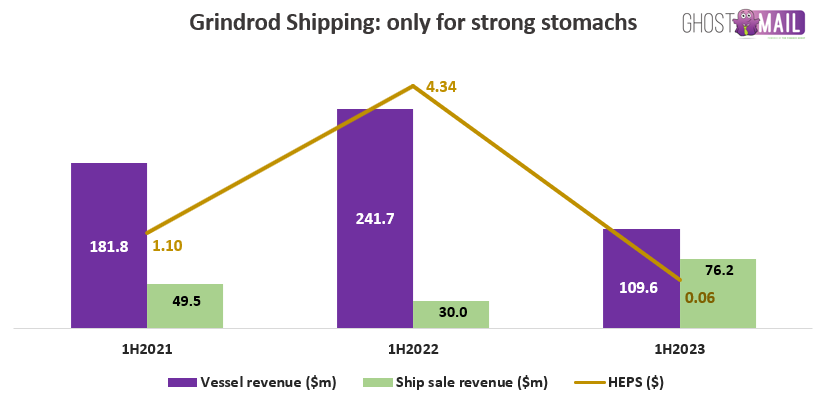

Grindrod Shipping: a lesson in cycles (JSE: GSH)

It’s hard to think of a more volatile sector than shipping

Unless you were living under a rock during the pandemic (OK – scrap that – we all were), you would’ve been reading about supply chain problems and how retailers just couldn’t get stock. As we emerged from that mess, pent-up demand for goods was extraordinary and people literally couldn’t get their hands on stuff quickly enough. That was a golden opportunity for shipping companies to make massive profits.

As is always the case, these supply-demand distortions tend to right themselves. This chart of Grindrod Shipping’s revenue and HEPS should hopefully illustrate the point:

I want to particularly draw your attention to how close ship sale revenue has been to vessel revenue in the past six months. Shipping companies regularly buy and sell vessels to right-size the fleet based on levels of demand. The proceeds are either used to reduce debt, execute share buybacks or pay special dividends, depending on the company’s balance sheet.

In Grindrod Shipping’s case, a capital reduction of $45 million was approved by shareholders in August. Because of this, no further dividends will be declared in 2023.

The focus area for the company is on the combined management of the Grindrod and TMI fleets and realising the associated synergies. The company is also hoping for a “gentle” structural recovery in the Chinese economy in 2024.

Little Bites:

Director dealings:

An associate of a director of Nampak (JSE: NPK) has bought shares in the company worth nearly R1.9 million.

A director of Richemont (JSE: CFR) bought shares in the company worth roughly R540k.

In a long announcement that says a lot without actually saying very much at all, AYO Technology (JSE: AYO) reminded the market that Khalid Abdulla’s fine and censure is the subject of a reconsideration application at the Financial Services Tribunal. This isn’t anything that the JSE didn’t already tell us. The company also reiterated its commitment to Abdulla regardless of this situation, which is another good example of why I’m not an investor in this group.

For those following the Lighthouse Properties (JSE: LTE) trades, the results of the scrip distribution are now in for directors. Des de Beer will receive R42 million worth of shares under this distribution, adding to his numerous recent purchases of shares in the company. There’s a few million bucks worth of shares in total being received by other directors as well.

Anglo American Platinum (JSE: AMS) announced that Sayurie Naidoo has been appointed as acting CFO of the company. This is an internal appointment, as Naidoo has been with the broader Anglo American group for 15 years.

Richemont (JSE: CFR) announced a couple of senior changes. Gary Saage is an ex-CFO of Richemont and has been proposed for appointment to the board and as the chairman of the audit committee. Among other changes, I couldn’t help but smile at the appointment of a new CEO of the Laboratoire de Haute Parfumerie et Beauté – an incredibly pompous title to help the six Maisons involved in fragrances to reach critical mass. His name? Boet. There is officially a Boet in charge there, of the non-Fourways variety. He should surely enhance his name to Boët and give it a luxury spin!

Congratulations to Mazars on their appointment as auditors of Hosken Consolidated Investments (JSE: HCI)

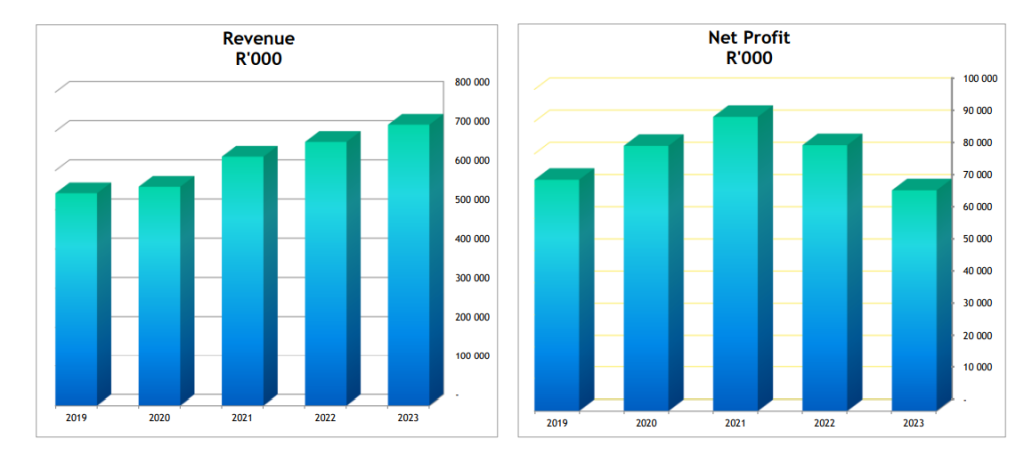

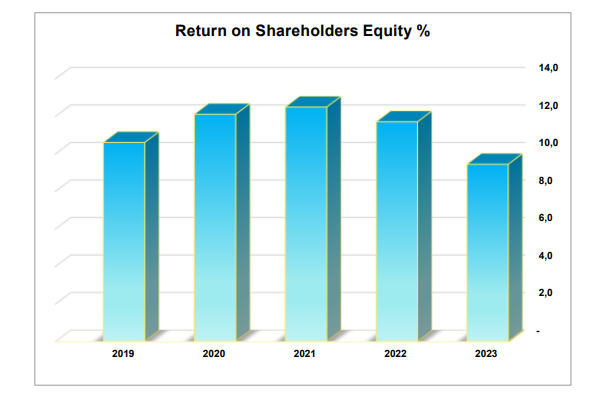

Bowler Metcalf’s net profit margin continues to drop (JSE: BCF)

For the sake of bringing back memories of outdated formatting, I won’t change their charts

On the local market, it’s a bit of a cult thing to be one of the companies that truly doesn’t care about formatting in official documents. I can only assume that to be the case at Bowler Metcalf, as nobody on earth releases charts like these and thinks they look modern:

These are your charts of the day, just for the hell of it. I can’t bring myself to change that formatting or redo them. But more importantly, I’m actually grateful to the company for including charts like these and making it easier for investors to see what is going on.

The revenue chart looks good, doesn’t it? the net profit chart, not so much. Net profit margin was 13.3% back in 2019. It’s now dropped all the way down to 9.6% for the year ended June 2023, which means net profit in absolute terms is lower than it was four years ago despite revenue being 32% higher.

It takes working capital to generate revenue and so it isn’t surprising to see a deterioration in return on equity, down from 10.6% in 2019 to 9.4% in 2023. The only good news about return on equity is that they used slightly different formatting:

Yet despite this, HEPS has somehow increased from 88.10 cents in 2019 to 102.96 cents in 2023. Welcome to the world of share buybacks, with 15% fewer shares in issue now than in 2019. The share price is trading ahead of the levels seen in 2019 after the payment of a very large special dividend, so this strategy of buybacks has saved the day for shareholders. It’s made all the more impressive by ordinary cash dividends having been paid along the way as well.

Perhaps capital allocation is more important than chart formatting after all?

City Lodge shows us what a normal year looks like (JSE: CLH)

Well, as normal as South Africa gets

After such a terrible period during the pandemic, City Lodge had to make big changes to its business model and really improve the overall efficiencies in the group. Nothing breeds innovation quite like a crisis, with the benefits of these initiatives to be felt for years to come.

In a trading statement for the year ended June 2023, we can now see what a “normal” year of trading looks like for the company. The announcement came out at around 4pm and the share price jumped over 5%, yet it is still only flat year-to-date.

This is because although the percentage increase in HEPS looks ridiculous (as the company was loss-making last year), the range of 29.6 to 31.3 cents still isn’t exactly exciting compared to a share price of R4.97.

Time will tell on this one, but I haven’t shared the bullishness of some commentators on Twitter / X because the valuation really doesn’t look appealing. It doesn’t matter what the replacement cost of the hotels would be if they can’t generate proper returns on capital. People simply wouldn’t replace them with hotels then!

Coronation is off to the Constitutional Court (JSE: CML)

The tax matter isn’t necessarily over yet

After the Supreme Court of Appeal ruined the party (and the dividend) at Coronationthis year based on upholding an appeal from SARS for a huge tax bill, Coronation decided not to give up. The dispute relates to profits in the international operations, together with interest and costs.

Coronation applied to the Constitutional Court for leave to appeal the judgement. Much to the joy of the lawyers involved, the Constitutional Court has agreed to hear the application for leave to appeal and arguments on the merit of the matter. It will be set down for hearing in due course.

Mustek suffers financial fraud at an associate owned by none other than AYO Technology (JSE: MST | JSE: AYO)

The announcement tries to soften the blow by calling it “irregular expenditure”

Whatever you want to call it doesn’t really make a difference, as the impact is that shareholders of Mustek have suffered a loss thanks to financial shenanigans at Sizwe Africa IT Group. Mustek has director representation on the board there in a non-executive capacity, which means tea and biscuits every few months and a pretty board pack. Non-executives directors are worse than useless at picking up financial fraud, with endless high profile examples of this.

The internal audit function at Sizwe Africa picked up the issue. This is what internal auditors do, although ideally the controls should already have been there to stop it happening. The employees linked to the “irregular expenditure” have been suspended.

For the year ended June 2023, the impact on Mustek’s HEPS is estimated to be between 30 cents and 40 cents. That’s material on a share price of R14.05. Despite this, the company doesn’t need to issue a trading statement, so HEPS won’t be more than 20% different from the prior period.

The real question is why a respectable company like Mustek has an investment in a subsidiary of AYO Technology, as Sizwe Africa is part of that group. It’s incredible that on the same day, the JSE can censure an AYO director (see more details in Little Bites) on a legacy matter, with the company then reporting a new financial issue as well.

And then people wonder why several banks distanced themselves from AYO and friends?

Orion Minerals keeps SENS ticking over (JSE: ORN)

It’s typical of junior miners to announce every possible bit of good news

Junior mining is all about making progress as quickly as possible and showing investors that there is hope of getting some tasty commodities out of the ground. This is why you’ll see companies in this sector announce just about anything they can, down to what the CEO had for breakfast that morning.

There’s an Orion Minerals announcement for the second day in a row, this time dealing with the award of a trial mining contract for Prieska Copper-Zinc to Newrak Mining Group. Newrak is a South African contract mining company and the idea here is to compare a fleet of conventional loaders with a continuous loading machine.

Think of it as a test drive, but for mining equipment.

Rebosis offloads another R650 million in properties (JSE: REA | JSE: REB)

The price is a large discount to the April 2023 valuations

In the first round of sales in this public sales process as part of the Rebosis business rescue, the selling price was pretty close to the valuations of the properties. Not so this time, with a sale of properties valued at R1.07 billion for R650 million. That’s quite the haircut.

The buyer is Hemipac Investments, a subsidiary of property group SKG Africa.

These are office buildings with various vacancy rates, in some cases an extraordinary 100%! I suspect that redevelopment is on the cards but I’m just speculating here. Some of them are fully tenanted, so perhaps those are to be kept as rental opportunities.

The net operating income on the portfolio is R58.5 million so the price of R650 million is decent in that context. The value of R1.07 billion was clearly blue sky stuff.

Sanlam’s alliance with Allianz has become effective (JSE: SLM)

And there’s good news for Santam shareholders (JSE: SNT) off the back of this

It takes a long time for major corporate activity to actually work its way through the regulatory approvals required for these transactions. Sanlam’s proposed joint venture with Allianz SE was first announced in May 2022. We are now in September 2023 and the deal has finally closed.

The structure of the deal is that Sanlam and Allianz will contribute their African operations to the joint venture, creating a genuinely Pan-African financial services group.

The initial split in the joint venture was agreed as being 60% Sanlam, 40% Allianz. Post-closing adjustments are provided for in the agreements as the deal has taken well over a year to close, so the performance over that period needs to be taken into account. Although a material deviation from that number is unlikely, it may move slightly.

Importantly, Allianz has the option to increase its shareholding at a later stage to 49%. This means that Sanlam will remain in charge of this joint venture. Another important point is that Sanlam’s Namibian operations will be contributed to the joint venture company at a future point in time.

In a separate announcement but linked to the same transaction, Santam previously announced that it would dispose of its 10% interest in SAN JV to Allianz. This deal became effective on the same date as the Sanlam joint venture, which means Santam received R2.6 billion in cash from the sale.

R2 billion of those proceeds will be declared by Santam as a special dividend. This works out to R14.24 per share, which is roughly 4.7% of the current share price.

The Brackenfell Bruisers look unstoppable (JSE: SHP)

Shoprite is going for the kill

It’s not often that I read something on SENS and genuinely have to sit back in my chair to let it sink in. The Shoprite results are, quite frankly, ridiculous. The Supermarkets RSA business grew 17.8%, so Shoprite won record levels of market share (140 basis points) this year.

The losers? Clearly, competitors. I think you may need to Pick n Pray for a miracle if you are taking a view against Shoprite.

Perhaps the most impressive thing about this result is that the growth hasn’t just been at the top end in Checkers. That side of the business has certainly done well, with an increase in sales of 18% and Sixty60 managing an astonishing performance of 81.5% growth. The group is also doing well with lower income consumers, as Shoprite and Usave increased sales by 15.6%.

I must note that the 92 Massmart stores have been integrated into the Shoprite and Usave operations, so that is giving the sales number a boost. Still, the point remains that the company is resonating with consumers everywhere.

Some pricing pressure has come through the system to support this market share growth, with gross margin down from 24.5% to 24.1%.

The blemish on the result is obvious: Eskom. There’s nothing that Shoprite can really do about that, as fridges need to be kept cold. R1.3 billion was incurred on diesel costs. Although there’s an offset from not paying Eskom instead, the reality is that this is still a very big number in the context of profit before tax of R9.1 billion.

By the time we work through the Eskom pain, sales growth of 16.9% is blunted to HEPS growth of just 9.6%. The dividend is 10.5% higher.

This is an annoyance for shareholders in the context of what might have been. But with a longer term view, the momentum at Shoprite is beyond incredible. Unless you have some retail experience, it’s hard to appreciate just how good this performance is.

And in case you’re wondering, Supermarkets non-RSA grew sales by 16.4% in rand terms (9.6% in constant currency). Furniture sales grew 5.1%. Other operating segments were up 13.3%, with OK Franchise sales up by 13.7%.

Finally, as another good example of how South Africa makes life far harder for our corporates than it should be, insurance costs were up by R185 million because of premium increases since the 2021 social unrest and the need for additional cover.

South Africa is a treacherous minefield for food retail at the moment. Shoprite seems to know where all the mines are. The share price told a different story on the day, with a significant drop. I would attribute this to the return of stage 6 load shedding and the realisation by the market that Shoprite’s multiple is high for a company that faces this many headwinds to profit growth, even with revenues growing quickly.

This is exactly why it is possible to (1) have massive respect for this management team and (2) avoid any exposure to this sector entirely. The uncontrollable macroeconomic problems make it too risky for even the best management teams.

The Foschini Group flags a big drop in HEPS (JSE: TFG)

Watch the share price action on Wednesday when the market opens

The Foschini Group released a trading update for the 22 weeks ended 26 August, as well as a trading statement for the six months ending September. This is because they already know that HEPS for this period will suffer a negative move that triggers the release of a trading statement.

We begin with the 22 weeks, where group turnover grew by 11.3%. This includes Tapestry, the recent acquisition.

We need to dig deeper to see the effect of that acquisition, with TFG Africa up by 16.1% including Tapestry and 9.7% excluding Tapestry, with clothing as the major contributor here with much higher growth (11.8%) than categories like cosmetics (3.8%) and cellphones (2.5%). Like-for-like growth in that business was a paltry 3.3%, so new stores are adding a lot to the story. Encouragingly, cash turnover growth in TFG Africa was 21.8%, so credit sales are growing really slowly at just 2.9%. Cash turnover contributes 73.4% of total TFG Africa turnover.

The international story is far less encouraging because it is coming off a high base, with TFG London down by 12.4% in GBP and TFG Australia down 6.6% in AUD.

Online turnover was up 23.2%, with the online contribution increasing from 9.1% to 10.1%. The launch of Bash was a major driver here, taking the contribution of online sales in TFG Africa to 4.2%. Online sales contribute 40.9% of TFG London and 6.0% of TFG Australia.

Although this sounds like a decent revenue outcome at group level, there are other problems like a 300 basis points drop in gross margin in TFG Africa as stock was cleared. The impact of inflationary increases on costs and of course load shedding means that HEPS will be 15% to 25% lower. The finance costs on the group debt definitely wouldn’t have helped matters here either.

The HEPS range for the interim period is 348.5 cents to 394.9 cents and the share price response on Wednesday will be important to watch, as this announcement came out after market close. I expect it to be negative, with my view on TFG being highly bearish at the moment because of the level of debt in this consumer environment.

Little Bites:

Director dealings:

You guessed it – Des de Beer has bought another R8.4 million worth of shares in Lighthouse Properties (JSE: LTE)

Now here’s an interesting one – the CEO of Murray & Roberts (JSE: MUR) bought shares in the embattled company to the value of R605k.

And from large trades to very small ones – the spouse of the CEO of Calgro M3 (JSE: CGR) bought shares worth under R3.5k,

In a long announcement that lays bare exactly why I would rather invest in a dying earthworm than AYO Technology (JSE: AYO) or any of the companies related to this group of people, the JSE has explained why Khalid Abdulla has been censured in his capacity as a director of AYO. There are a couple of reasons, including a related party asset management agreement that wasn’t adhered to and instructions given to make changes to financial statements while the former CFO was on leave. The JSE has imposed a very embarrassing public censure and fined Abdulla R2 million for his failure to comply with the listings requirements. This censure comes after a court process that included an attempted interdict against the JSE from publishing the ruling. There is still a reconsideration application to be heard by the Financial Services Tribunal.

enX Group (JSE: ENX) renewed the cautionary related to the potential sale of the stake in Eqstra Investment Holdings. Negotiations are still ongoing.

NEPI Rockcastle (JSE: NRP) has confirmed that the scrip distribution price is R104.70715169, a 3% discount to the 5-day VWAP (less the final dividend) as at 4 September. The company will hope that many shareholders take up the scrip alternative so that it can hang on to more capital. Based on strong recent results, there’s a good chance of that happening I think!

Featured: Naspers and Prosus finalises the capitalisation issue

In a complicated transaction, Naspers (JSE: NPN) and Prosus (JSE: PRX) have released a finalisation announcement for the capitalisation issue that effectively removes the cross-holding structure that the market was very unhappy with during its relatively short-lived existence. You can get all the details in this announcement>>>

Featured: RCL Foods needs a brighter Rainbow

Our poultry industry in South Africa is in a lot of trouble

Revenue at RCL Foods increased by 17.3% for the year ended June 2023. That sounds strong, but things go very badly as we move down the income statement. EBITDA fell 24.5%, or 11% excluding material once-offs. HEPS fell by 42.4% overall and by 45.7% from continuing operations. In the same way that they calculated the 11% drop in EBITDA, HEPS was down 20.2%.

The numbers aren’t pretty, which is why there’s no dividend this year.

The special levy raised by the South African Sugar Association got a lot of attention this year. Despite that levy, the sugar business actually delivered a solid result. The baking segment was flat year-on-year. The grocery segment didn’t get any tails wagging, with pet food production down by almost 50% from November 2022 to April 2023 because Eskom is the furthest thing from a good boy.

But to find the real pain, you need to go looking for rainbows. The chicken business is taking severe strain, with Rainbow’s underlying EBITDA down by 74.9% because the market simply cannot absorb the pricing increases that would be required to offset input cost pressures.

Notably, the Vector Logistics segment has been classified as a discontinued operation at year end. The disposal of that business was completed at the end of August.

You can get full details on the announcement at this link>>>

African Rainbow Minerals on the wrong end of Transnet (JSE: ARI)

Local infrastructure continues to hurt our mining houses

African Rainbow Minerals reported a drop in headline earnings of 21% for the year ended June 2023.

The group generates 61.6% of its headline earnings from the ARM Ferrous division, which fell 17% with pressure on iron ore (down 11%) and manganese (down 34%).

ARM Platinum took the most pain, tanking 52% in line with what we’ve seen with the rest of the industry. That segment now contributes 16.3% of group headline earnings.

For some good news, you can look at ARM Coal with headline earnings up by 65%. It only represents 17% of the group total, so this wasn’t enough to save the result.

In general, lower commodity prices have been the driver of the decrease, with logistical challenges at Transnet and Eskom doing nothing to help the situation.

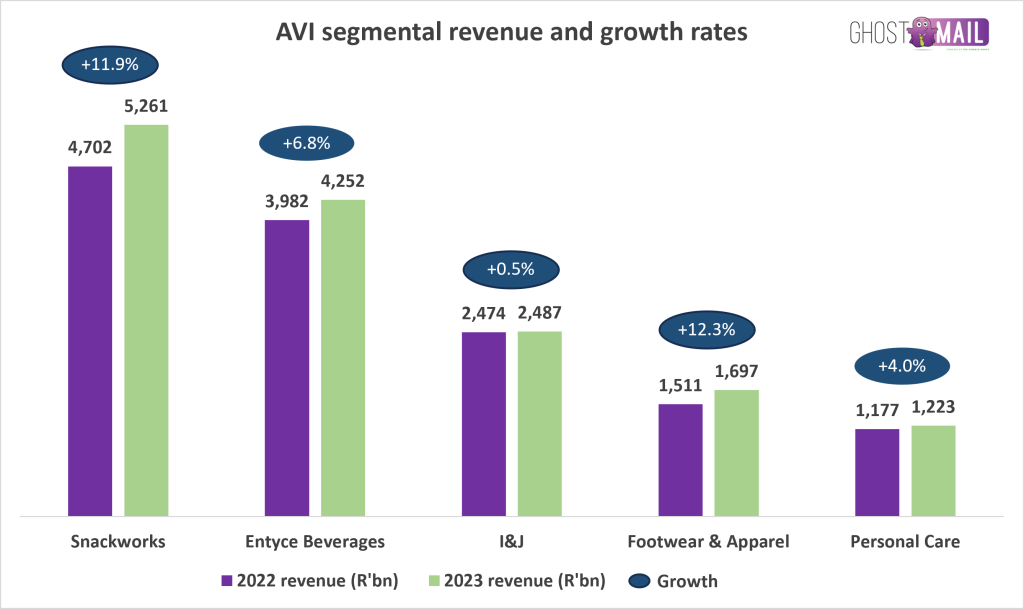

AVI looks pretty good excluding I&J (JSE: AVI)

Unfortunately for shareholders, they can’t just exclude I&J

For the year ended June, AVI’s revenue increased by 7.8%. This was no thanks to I&J (16.7% of the business) which was flat year-on-year on the revenue line. If I exclude I&J from the numbers, revenue grew by 9.3% which is a bit more interesting.

The difference is far larger at operating profit level. I&J’s flat revenue isn’t what you want to see in a time of inflationary pressure, with operating profit down by 36%. Operating profit excluding this business was up by 12.7%. The blended group result is a 6.9% increase in operating profit.

By now, you must be wondering what went wrong at I&J. Fishing is a tough business, with catch rates and fuel costs as major variables. In the first half of the year, lockdowns affected the abalone sales mix as well.

The good news story in these numbers is that AVI has decent pricing power, with gross margins stable in this environment. You can see strength in the numbers beyond I&J. This helped drive HEPS growth of 4.3%, a result that is admittedly below inflation but still on the right side of zero. A decent result in terms of cash conversion means that the final dividend of 310 cents per share is also 4.3% higher.

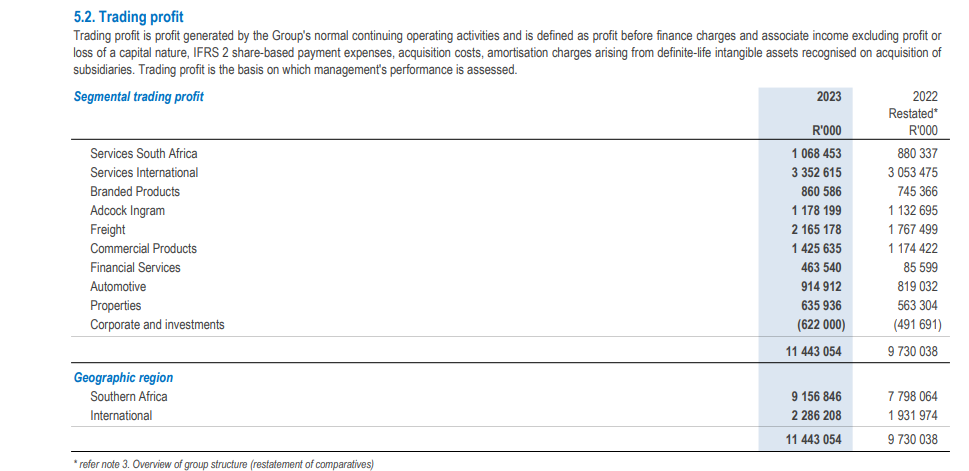

Bidvest’s focus on capital discipline pays off (JSE: BVT)

The second half of the year was all about generating cash

For the year ended June, revenue at Bidvest increased by 15% and trading profit jumped 17.6%. That’s a good story for operating margins. It also helps that cash generated from operations was R12.2 billion vs. trading profit of R11.4 billion, with R10.4 billion of that cash generated in the second half of the year!

This cash flow performance supported dividend growth of 20.6% vs. HEPS growth of 17.7%.

Bidvest is a highly diversified business and the result has been driven by various factors across the group. It’s certainly notable that the Freight division reported trading profit that is double the level reported three years ago. There were seven divisions that reported double-digit trading profit growth in this period.

Return on Funds Employed (ROFE) improved from 37.6% to 38.3%. Return on Invested Capital (ROIC) might be a measure that you are more familiar with, up from 17.1% to 17.3%. This is well above the cost of capital, which means that Bidvest is generating genuine economic profits.

The note on trading profit gives you a great idea of how diversified the business is:

Brimstone reports a drop in intrinsic NAV (JSE: BRT)

You need to go to the website to find the intrinsic value calculation

Brimstone’s financial results aren’t really as important as the calculation of intrinsic NAV. This is because Brimstone is an investment holding company and thus the value of the underlying portfolio is more important than a set of numbers that is partially consolidated and partially based on other accounting methods.

Oceana and Sea Harvest collectively contribute 73% of the portfolio and are both listed, so the market value per share is used in the intrinsic NAV calculation. There are positions in Equites, Phuthuma Nathi, STADIO and MTN Zakhele Futhi that get the same treatment, with listed positions contributing 85.4% of the portfolio.

There are a variety of unlisted investments, with FPG property fund as the largest with a 6.2% portfolio weighting.

Intrinsic NAV fell by 6.7% between December 2022 and June 2023. An 11.3% increase at Oceana was the only meaningful highlight, with substantial drops at the likes of Sea Harvest and Equites as major contributors to the overall decline.

The intrinsic NAV per share has fallen from R14.193 at the end of December 2019 to R12.362 at the end of June 2023. The share price’s discount to intrinsic NAV has also increased from 46.1% to 55.9% over that time period, so it really hasn’t been a happy time for shareholders.

Cognition Holdings: all about the cash (JSE: CGN)

The current value has very little to do with the earnings

After selling its controlling stake in Private Property, Cognition Holdings unlocked a massive amount of cash and recognised a R66.7 million profit on the sale. Of total assets of R266 million on the balance sheet, almost R215 million is attributable to cash.

This is why the share price of 95 cents makes sense compared to net asset value per share (103.37 cents) rather than HEPS (3.15 cents).

The underlying operations aren’t doing very well I’m afraid, with revenue down 13.6% and gross profit down 8.2%. Because of significant cost cutting, EBITDA managed to increase by around 10x to R4.8 million. This shows you how tiny the remaining operations actually are.

The company is working with its parent company Caxton & CTP (JSE: CAT) to figure out the best way to return value to shareholders.

There’s no interim dividend at property group MAS (JSE: MSP)

This debt environment is starting to really hurt some of the property funds

A property fund relies on having a decent mix of debt and equity on the balance sheet to drive returns. This makes the sector vulnerable to not just rising rates, but a tighter lending environment in which banks are more cautious.

Some companies are proactive and take a more conservative approach to cash management before there’s an issue. Others run head-first into the fire and then look all surprised when they end up in serious trouble.

Although the market gave MAS an 8.5% knock on the news that the interim dividend won’t be declared this year, the company does deserve credit to taking a safer approach to its self-imposed debt limitations.

Alongside this news, the company also released results for the year ended June 2023. The operational performance looks strong, with adjusted distributable earnings per share up by 30.7%. The exposure to Central and Eastern Europe continues to work well for funds in that region. But despite this, Moody’s downgraded the fund based on the difficult funding environment for real estate companies and this becomes a self-fulfilling prophecy, as demand for sub-investment grade bonds has declined and the cost of new funding has increased.

Although the downgrade from Ba1 to Ba2 didn’t take it below the investment grade threshold (even Ba1 has “speculative elements” on the Moody’s scale), every move further down the ratings scale has an impact.

The company thus has to be mindful of bond maturities in 2026 and what the funding environment might look like at that point. The board has dropped the loan-to-value limit from 40% to 35%, although they are already below that level so that’s a bit of a non-event from what I can see. As a further step, the company is raising debt against unencumbered properties (assets that aren’t already pledged as security for debt), with those proceeds aimed at reducing risks associated with the bond maturity.

As a final step in de-risking the business, residential property projects in Romania have been put on hold in the group’s construction joint venture. Unsold units will be retained for rental.

This feels like an incredibly conservative approach, which tells us a lot about both this management team and the outlook on interest rates and debt.

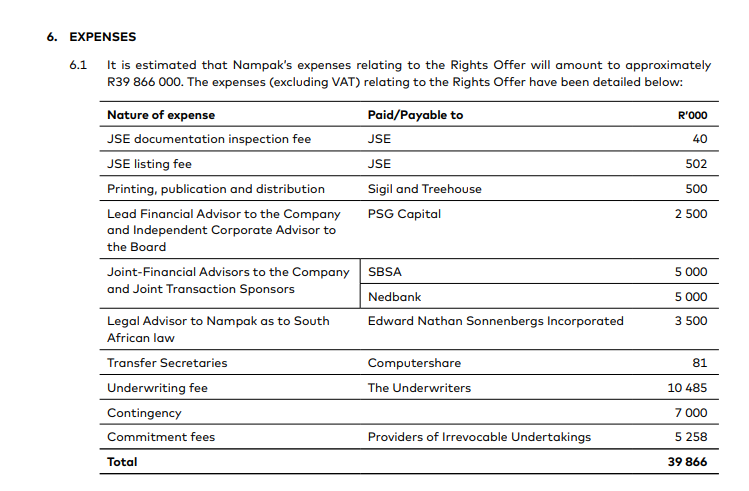

Nampak lays out the details of the rights offer (JSE: NPK)

The circular has been released to the market

In case you’ve been living under a rock, Nampak is in serious trouble. The company needs to raise R1 billion in equity to fix the balance sheet.

If you read the circular, you’ll find a section called “rationale” that lays the blame for the capital raise squarely at the door of the decision to expand into Africa in 2011. Between 2011 and 2014, Nampak invested heavily in Africa and funded that expansion in US dollars. You can refer to this article to see the comments by none other than Andre de Ruyter when he was CEO in 2014, talking about the vote of confidence in Africa.

Hindsight is perfect, of course. Many companies have learnt the hard way that even when the operations in Africa look good, funding those operations with US dollar debt is almost financial suicide. It’s extremely difficult to expatriate dollars from African countries to service that debt.

There were other issues, like the South African businesses coming under pressure as well. This was the tipping point for the group. Despite various management interventions, the company still operates in 10 countries on the continent and is thus highly exposed to volatile currencies that are often dependent on a single commodity.

With strong management having been appointed to restructuring positions, Nampak needs capital to sort out this spider web of pain and agony.

R1 billion is the target for the capital raise and R950 million is already in the bag. Commitments worth R500 million were received from major shareholders A2, Allan Gray, Old Mutual and PSG Asset Management. These shareholders will receive a 1% fee for the pleasure of having given a commitment. That’s what underwriters used to get paid when the JSE was an easier place to raise capital a few years ago!

Speaking of underwriters, R450 million has been underwritten by Coronation (R300 million), A2 (R100 million) and Numus (R50 million). The fee to each of those parties is 2.33%.

The cost of this capital raise comes in at nearly R40 million, or approximately 4% of the amount being raised. This includes the commitment and underwriting fees. Here’s how that amount gets used:

PPC announces another international executive as CEO (JSE: PPC)

Having an international executive join the group at such a difficult time worked out very well with van Wijnen, so PPC has clearly felt confident about doing it again. Matias Cardarelli has been named as the incoming CEO, having moved to South Africa five years ago to run Natal Portland Cement. That means that dealing with cement imports should be second nature to him, which is useful to PPC.

Cardarelli has worked in countries like Egypt, Paraguay and Mozambique as well. This bodes well for the next phase of leadership at PPC.

Sea Harvest takes you to foreign waters (JSE: SHG)

The international revenue mix is up to 45%

For the year ended June 2023, Sea Harvest grew revenue by 18%. That most interesting part of that story is that international revenue now contributes 45% of the total, up from 39% last year. This is because MG Kailis in Australia has been included for the full year, so the Aussie business is up by 94% in revenue. That didn’t translate into operating profit because of higher fixed expenses and selling and distribution costs, with operating profit of just R2 million vs. R4 million a year ago.

The operating profit trajectory wasn’t very exciting in South African fishing either, with revenue up by 10%, but profits up by just 1% to R238 million as margin dropped from 17% to 15% thanks to a jump in fuel costs and other inflationary pressures.

The best profit story was in the aquaculture segment, with revenue up by 11% and EBIT swinging wildly from a loss of R19 million to profit of R79 million. Before you get too excited, this segment made an operating loss of R16 million. The rest of the swing is primarily driven by a gain on purchased loans related to the Viking Aquaculture deal.

At Cape Harvest Foods, revenue increased by 9% but operating profit fell by 48%, not least of all because of the double digit increase in the milk price in cost of sales and R15 million in load shedding costs. Profit decreased from R55 million to R29 million.

So, it doesn’t exactly sound like a great story in the core business, yet HEPS is up by 19%. Headline earnings increased by 17% from R182 million to R213 million. The gain on purchased loans is R93 million, so the result would look a lot worse without that transaction.

The share price fell 4% on the day.

Little Bites:

Director dealings:

Des de Beer really opened up his wallet this time around, buying R10.7 million worth of shares in Lighthouse Properties (JSE: LTE). He’s also been giving Resilient (JSE: RES) some love, buying R545k worth of shares.

A prescribed officer of Standard Bank (JSE: SBK) bought shares worth R97k.

BHP Group (JSE: BHG) announced that the court in Brazil ratified the judicial reorganisation plan of Samarco, the entity owned 50-50 by BHP and Vale that was at the centre of a terrible dam disaster in 2015. This will allow Samarco to restructure its debt. Samarco is responsible for $1 billion of Renova Foundation remediation and compensation program costs until 2030, with BHP and Vale on the hook for any excess cash needed above that cap on a 50-50 basis.

Orion Minerals (JSE: ORN) announced the expansion of the Okiep Copper Project after securing prospecting rights over the Nigramoep Mine and other nearby areas. This is key to the investment case, as the plan has been to consolidate several mining opportunities in the area under a central operational hub.

Lighthouse Properties (JSE: LTE) announced the results of the scrip distribution. It looks as though holders of 56% of shares in issue elected the scrip alternative. The issue price ended up being just below R5.40 vs. the current traded price of R5.25.

Oando (JSE: OAO) is acquiring 100% of Nigerian Agip Oil Company from Eni. No value for the deal was mentioned in the announcement.

Peter Todd has resigned as CEO of Conduit Capital (JSE: CND) and will continue as CEO of the subsidiary companies that are being sold. Peter joined to try and steady the ship when Conduit imploded. The current Chairman, Leo Chou, takes over as CEO and lead independent director Melvyn Lubega is now the Chairman.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this episode of Ghost Wrap, I looked at some of the more interesting stories in a busy few days of news.

Cher once asked us if we believe in life after love. I’m not sure about that, but we can believe in life after REIT based on the latest numbers from Fortress.

The recent results from Truworths need a careful read based on important and justifiable adjustments, with the core results revealing a decent period for the company.

Load shedding really hurts food retail, as evidenced by comparing Woolworths’ Food business to its Fashion, Beauty and Home business.

Bidcorp’s numbers for the year ended June are practically faultless.

Cashbuild is in a perfect storm right now, with ongoing difficulties in this trading environment.

KAP may need to rebrand to KLAP, because that’s exactly what the company got given in the latest period by Safripol and Unitrans.

Motus is a reminder that you always need to read to the bottom of the income statement, with finance costs eating up growth in operating profit.

Honestly, I miss writing. I particularly miss writing something that doesn’t necessarily have a purpose as I begin, morphing into something interesting and largely unexpected. That’s what is happening here. As I type this, I don’t know what the next sentence will be.

It’s refreshing, if I’m honest. The words flow quickly and there’s an excitement in sitting down and writing something without referring to a SENS announcement, especially from the likes of Blue Label Telecoms with more confusion than a session of parliament.

I’ve always been more interested in the stories behind the numbers rather than the numbers themselves. This is why I’m so passionate about the work I do with Mohammed Nalla in Magic Markets and especially Magic Markets Premium, with a strong focus on the strategy rather than note number 647 of the financial statements. Aside from helping auditors earn a living, those notes don’t add a huge amount of value.

Anyway, this isn’t a Magic Markets sales pitch*. It’s me writing about stuff that I’m passionate about. I just can’t help but be passionate about a great product delivered to South Africans at an accessible price point!

Be careful what you wish for

When I started Ghost Mail, it was a weekly mailer that was purely a fun project that I figured might have a future. I just didn’t know what it would be. Over three years later, it turns out that the project became a daily newsletter with around 100,000 engaged readers every month. That’s a gigantic number, though it all becomes a blur above a certain level.

I can still remember getting excited when 10 new people would sign up in a given week. I took it quite personally when someone unsubscribed, though I eventually got over that feeling.

The best part about the weekly mailer was that I could write about anything. It wasn’t my full-time income at the time, so I could pick anything with a slight finance angle and turn it into an interesting read. I loved it.

Before you get worried, I absolutely love what I do in Ghost Mail on a daily basis, but it’s become formulaic out of necessity. People depend on me to read SENS properly every day and deliver a comprehensive but concise view of what happened on the local market. Like everyone, I make mistakes, but I like to think that I keep them to a minimum.

Sometimes the mailer goes out at just after 5am because I had enough energy to finish it the night before. Sometimes it goes out at 7am because I had to wake up at 6am to write the actual mailer, having finished Ghost Bites at some truly ghostly hour the night before. Sometimes the mailer goes out when the technology decides it would be appropriate to actually work, an issue that is thankfully rare these days.

As I focus again on writing what I “feel” like writing rather than what I “must” write, I thought it would be appropriate to reflect on a wonderful passage in the Terry Pratchett biography. He is one of my all-time favourite writers and the biography was written with no shortage of influence of his signature style. I’m going to try and read the Discworld novels from start to finish over the next 18 months or so. There are a lot of them, but they are worth it. I have spent the past decade feeding my brain non-fiction and it’s time to get my imagination going again.

Pratchett has sadly departed this world, having gifted a lifetime of extraordinary writing to humanity that will stand the test of time. The world would be a much poorer place if he hadn’t made an effort and taken the risks to pursue what he was born to do. There’s a lesson in there for all of us.

Anyway, here’s the passage I was talking about:

“So, what with one thing and another, Terry had reached that precarious point where the business of being Terry Pratchett was threatening to prevent him from doing the thing that had made him Terry Pratchett in the first place.”

Terry Pratchett official biography by Rob Wilkins: A Life With Footnotes

I’ve spent a lot of time thinking about that. It simply means that it’s very easy to get too busy and stressed to remember why you did something in the first place. For entrepreneurs, I think the risk of this happening is extremely high.

I need to get back to finance-type stuff for the rest of the day, but it felt good to write this. Thanks for reading it. Most of all, thanks for supporting the Ghost Mail story and being part of my efforts to significantly close the gap in understanding between individual and institutional investors.

I’ll attempt to write something interesting and random every 10 days or so. Or every 9. Or every 11. After all, if I put an exact number to it, then I’m already destroying the randomness before I’ve even gotten started.

Until next time.

The Finance Ghost

*In honour of Terry Pratchett, I decided to use a footnote. You’ve now found the sales pitch. I would’ve killed to have access to this kind of research in Magic Markets Premium during my career, especially at R99/month. Don’t miss the opportunity that I never had.

Improving everyday life for people through technology

Shareholders are referred to the declaration announcement published by Naspers on SENS on Friday, 25 August 2023 (the Declaration Announcement), advising, inter alia, that the Naspers Board intends to proceed with the Naspers Capitalisation Issue and the Naspers Share Consolidation in connection with the removal of the Cross-Holding Structure pursuant to the Proposed Transaction, the implementation of which was subject to certain conditions precedent outlined in the Declaration Announcement.

The Naspers Board is pleased to advise Shareholders that the Proposed Transaction is now unconditional insofar as it relates to Naspers.

The purpose of this announcement is to provide Shareholders with finalisation information on the implementation of the Naspers Capitalisation Issue and the Naspers Share Consolidation in accordance with the JSE Listings Requirements.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")