")

Accelerate sells Cherrylane at a loss (JSE: APF)

The selling price is also below the latest valuation on the company balance sheet

Accelerate acquired the Cherrylane Shopping Centre back in December 2013 for R70.07 million and is now selling the property for R65 million. This is a classic example of buy high, sell low. Yes, you’re right, that’s the wrong way around.

The last valuation on the book was similar to the purchase price and the selling price is over 7% lower than the book value, though ironically this is still a great deal based on the discount to NAV that the market is currently putting on Accelerate.

In fact, if Accelerate sold ALL its properties at a 7% discount and returned the cash to shareholders, it would create incredible value. Don’t hold your breath.

EPE Capital Partners reports a modest increase in NAV (JSE: EPE)

There are 21 portfolio companies and investment exposure is R2.6 billion

In the results for the six months ended December for Ethos Capital (or EPE Capital Partners), you have to be quite careful with which metrics you focus on.

A useful number to consider is LTM maintainable EBITDA. In simple terms, this means operating profit (excluding once-offs) over the Last Twelve Months i.e. on a rolling basis, even though this is an interim result. This metric is up by only 1%, so all the improvement in the portfolio valuation came from multiple expansion, with the portfolio EBITDA multiple up from 7.7x to 8.2x.

Most of this uplift was driven by the Optasia business, which raised capital at a 22% premium to EPE’s previous valuation. In addition to the cash realised through this partial sale of Optasia, the group realised cash from Crossfin’s sale of Retail Capital to TymeBank. There were various follow-on investments during the period as well, as the portfolio is always being actively managed.

The listed assets in the portfolio had a tough time. Brait, the Brait exchangeable bonds and MTN Zakhele Futhi all dropped. This offset much of the growth in the unlisted portfolio.

The net asset value per share is reported based on two alternatives: Brait at its net asset value per share or Brait at its market value. Those are unfortunately very different numbers. If you use the former, EPE’s NAV per share is R10.80. If you use Brait’s market price instead, EPE’s NAV per share is R8.51.

The market isn’t interested in either of those numbers, with EPE trading at R5.60. The management fees payable to Ethos (soon to be The Rohatyn Group) is a big reason for the layered discounts.

Fairvest was a day late with this one (JSE: FTA)

The strategic rationale for this deal should’ve been announced on the same day as the deal

It’s hardly the end of the world though, as the market already knew that Fairvest’s stake in Indluplace was considered non-core. Fairvest will offload the stake to SA Corporate Real Estate (assuming the scheme of arrangement goes ahead) and will move on with its life.

If the investment is sold, the Fairvest portfolio will be skewed more towards lower LSM and convenience retail. The proceeds will be used to reduce unhedged debt, which makes an enormous amount of sense in this rising interest rate environment.

The loan-to-value ratio is expected to reduce by approximately 500 basis points.

It’s worth pointing out that the net asset value (NAV) per Induplace share is R6.61, so the selling price of R3.40 is way below the NAV.

The Grand Parade mandatory offer isn’t finalised yet (JSE: GPL)

Regulatory wheels are slowly turning

With a mandatory offer from GMB Liquidity Corporation of R3.33 per share on the way, the Grand Parade Investments share price is anchoring to that number (currently at R3.36).

Regulatory approvals are still outstanding, so the offer isn’t finalised yet and actual cash flow is still some time away. This is a mandatory offer, so the offeror cannot just decide to walk away. This is an important point.

Growthpoint’s dividend increases by 4.6% (JSE: GRT)

Tourism (and general Cape Town awesomeness) has done great things for the V&A

I’m one of those annoying semigraters (I think it’s been 8 years now) who loves Cape Town. Growthpoint loves it too, certainly far more than Sandton where the office portfolio remains a huge headache.

In the six months to December, the V&A Waterfront grew net property income by 23% vs. the comparable period. This is no indication of conditions in the rest of the portfolio. And for all the excitement around the V&A as the flagship property, it’s only R9.2 billion out of a group portfolio of R174.1 billion.

Looking beyond the biggest tourism attraction in South Africa, we find a portfolio which has seen renewal success drop from 75.1% to 61.2% and reversions worsen to -16% from -12.8% for the period ended June 2022.

This is why the overall result is only a slight improvement year-on-year. Net asset value (NAV) per share is down 2.2% but the FFO per share (a measure of cash profits) has increased by 2.1%. The dividend is up by 4.6%.

With R26.2 billion worth of Office properties in the R73.2 billion South African portfolio, Growthpoint remains exposed to the economic difficulties. The vacancy rate in that part of the portfolio improved marginally from 20.7% to 20.4%.

The group loan-to-value ratio increased from 37.9% at June 2022 to 38.8% at December 2022.

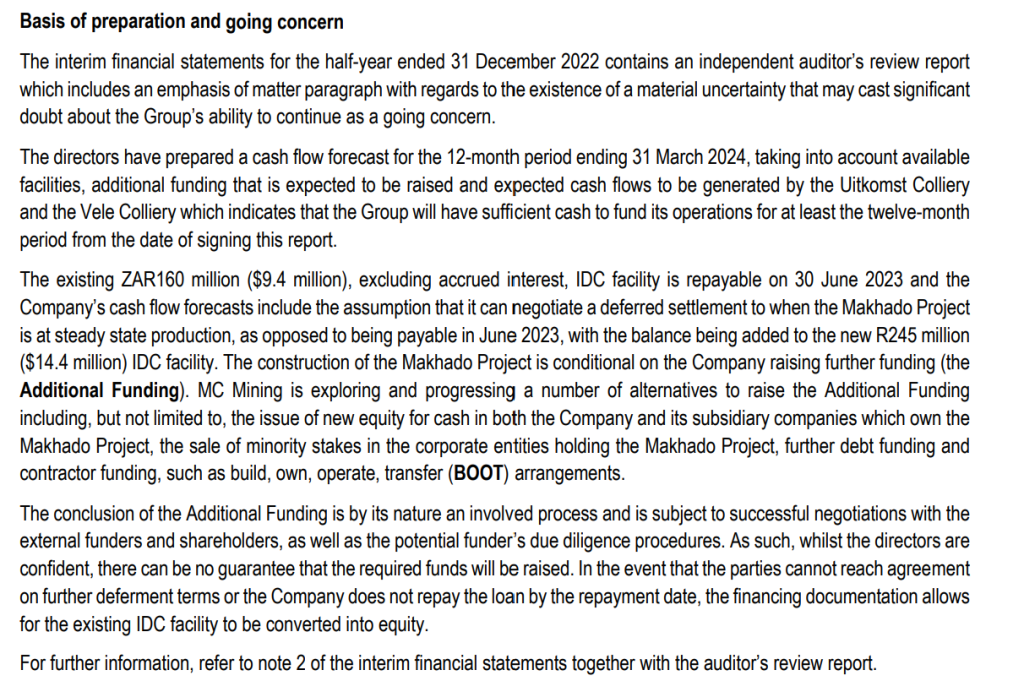

The fine print matters at MC Mining (JSE: MCZ)

The IDC loan is an important overhang for this stock

MC Mining has released results for the six months ended December. Revenue is up 8% and the headline loss per share improved from -0.54 cents to -0.50 cents. Clearly, it’s still a loss.

As a reminder, the company undertook a fully underwritten rights offer in November 2022, raising proceeds of $21.4 million.

Although there are functional operations in this group, the Makhado Coking Coal Project is the major focus. It’s also the reason for a detailed paragraph in the financials that talks about the IDC facility that is repayable in June 2023. If the company cannot defer that settlement or raise additional funding, the facility can be converted into equity. That would be very painful for shareholders.

Here’s the full paragraph, in case you’re interested in this stuff:

Good news for Merafe: the ferrochrome price (JSE: MRF)

Despite this, the share price closed flat as the broader market panicked

At Merafe, an increase in the European benchmark ferrochrome price is usually met by a higher share price. On Wednesday, the market was on fire and Merafe’s intraday gains couldn’t be maintained by the close.

The price for the second quarter of 2023 is 15.4% higher than the first quarter, so this was hardly a small move. I’ll be interested to see if the market wakes up to this update at some point when the panic subsides.

Orion announces Clover Alloys as a major investor (JSE: ORN)

This is a privately owned South African mining group with deep pockets

Newbies regularly make the mistake of thinking that large companies are only found on the JSE. These days, there are incredibly deep pockets in the private market in South Africa and the Orion deal is proof of that.

Clover Alloys apparently has an “outstanding track record” in developing and operating chrome operations. Orion is looking to raise A$13 million and Clover has come in as the cornerstone of the raise, subscribing for shares worth A$6.7 million. The company’s technical expertise will also be useful to Orion, so this goes beyond just the money.

Delphi Group and Tembo Capital are collectively coming in for A$2.6 million, with Tembo accepting shares as repayment for an existing loan facility.

Interestingly, those participating in this placement are also being given “attaching options” to sweeten the deal. It sounds like dodgy English, hence the quotation marks so you don’t blame me, but these are basically the rights to subscribe for further shares down the line at a price similar to the current market price.

This puts Orion in a very strong position to move forward, as you’ll recall that packages were also raised from Triple Flag Precious Metals and the IDC.

STADIO dishes out the cash to shareholders (JSE: SDO)

The dividend payout ratio has increased substantially

When STADIO gave us a teaser of the latest earnings, the market didn’t like what it saw in terms of student growth. Momentum slowed down, with second semester growth of 8% vs. 11% in the first semester.

An increase in revenue of 11% was good enough to drive HEPS growth of 18%, as the benefits of operating leverage came through the system. This is why investors tend to favour STADIO over Curro at the moment, as STADIO follows more of an asset-light model.

The surprising line for me was the dividend per share, which is up by 89% to 8.9 cents. Based on HEPS of 20 cents, that’s a pretty big payout ratio for a growth stock.

You’ll probably be interested to know that the semester one 5-year CAGR growth in contact learning student numbers is only 4%, whilst distance learning is 11%. In the past year, contact learning was down 4% and distance learning grew 14%. Obviously, this is skewed somewhat by STADIO’s strategic focus, but it’s still a good sign of where demand is.

It gets even more interesting in semester two, which has historically been a slower growth semester. It seems the market may have overreacted to the recent update about semester two vs. semester one growth. The difference is more significant in distance learning, so it seems that people either drop out halfway or get too busy midway through a year to register for distance learning.

Long story short: semester two is historically a slower period. This doesn’t mean that STADIO is losing momentum overall.

Little Bites:

- Director dealings:

- An associate of a director of Safari Investments RSA (JSE: SAR) has bought shares worth R26.5k.

- As anger mounted around Transaction Capital (JSE: TCP) and the share price tanked hard again on Wednesday, the company released a clarification announcement around previous dealings by a trust linked to CEO David Hurwitz. Was the trade legal? Yes, it seems that way. Does it look terrible optically, with investors sitting with huge losses just a few months later? Yes. Will his career survive this? Only time will tell. This has been a spectacular fall from grace for what was a highly respected management team on the JSE.

- Emira Property Fund (JSE: EMI) confirmed that Castleview Property Fund (JSE: CVW) now owns 55.38% in the company.