")

Anglo American reports a big drop in earnings (JSE: AGL)

A drop of 55% in HEPS isn’t pretty

The mining industry has been dealing with a drop-off in commodity prices this year. Cycles are nothing new to mining, with volatile earnings as standard practice in this game. That’s even true for the likes of Anglo American, with a diversified portfolio.

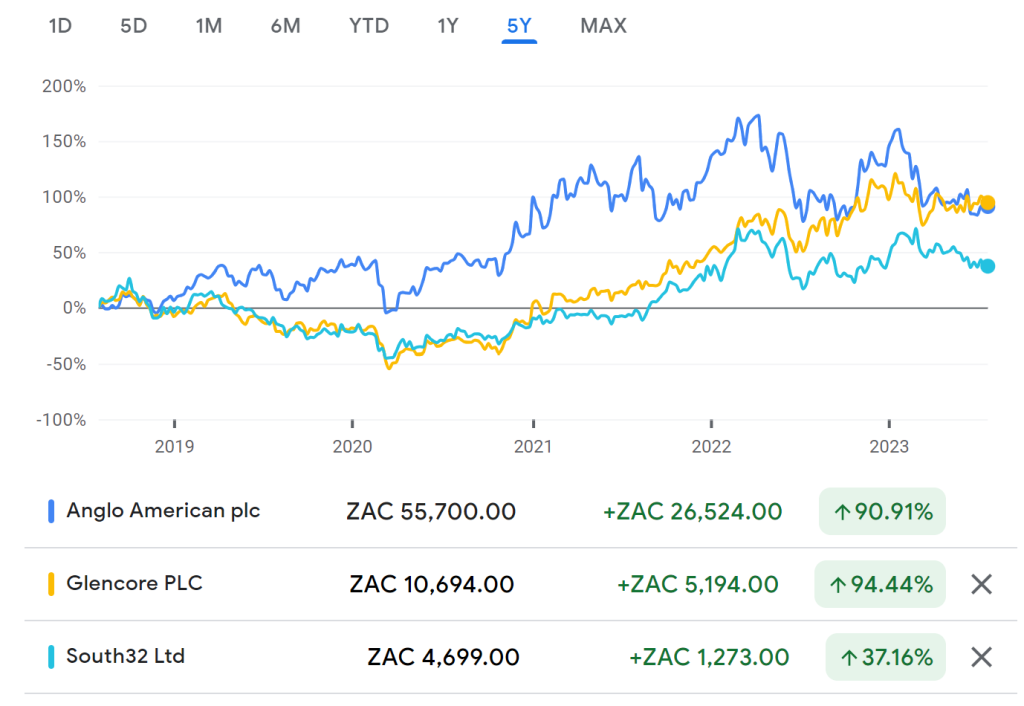

Over five years, you’ve still done alright in these names:

For the six months to June 2023, EBITDA fell by 41% in an environment of lower commodity prices. The basket price across the group fell by 19% and unit costs increased by 1%. Volume increases of 10% partially offset the impact, with group revenue down by 13%.

Net debt of $8.8 billion is less than 1x annualised EBITDA, so the balance sheet is ok. This is why the dividend payout policy of 40% has been maintained.

Here’s one for the books though: attributable free cash flow fell from $1.56 billion to -$466 million. Yes, that is negative free cash flow! Welcome to mining, where capital expenditure is huge.

Return on Capital Employed has fallen from 36% to 18%. This isn’t a good enough return for the risk in my opinion.

ArcelorMittal releases detailed results (JSE: ACL)

A headline loss of R448 million broke the share price when warning was first given

Let’s kick off with a share price chart, showing you exactly when news broke of how bad these ArcelorMittal numbers will be:

As you can see, the price partially recovered, although the downward trend is clear.

In the six months to June, a drop in realised rand prices of 8% ruined the fun. Although volumes were up 3%, there’s so much operating leverage in this business that EBITDA crashed by 86%. Operating leverage refers to the extent of fixed costs, something that is incredibly important in manufacturing and mining businesses. With vast fixed costs, a small drop in revenue can cause havoc for profitability.

EBITDA of R499 million was eaten up by the banks before we get to the headline loss of R448 million. Net borrowings increased from R2.8 billion to R2.9 billion, so ArcelorMittal is the poster child for the dangers of combining operating leverage and financial leverage.

As you’ve probably guessed, there is no dividend here.

With cash from operations of R891 million and a huge capital expenditure bill of R818 million, free cash flow is almost non-existent here. The company will need to make some major internal changes before it can make a dent in the debt.

Hammerson is paying dividends again (JSE: HMN)

This is important for local fund Resilient

A property fund that doesn’t pay dividends is about as useful as a leaky bucket. Nobody is buying property funds purely for capital growth, that much I can promise you.

After considerable pressure from shareholders (not least of all local fund Resilient), Hammerson has returned to paying cash dividends with the release of interim results. The disposal of £215 million worth of non-core assets has helped repair the balance sheet. Net debt to EBITDA is now at 7.7x vs. 10.4x at the end of the last financial year. The more common metric is loan-to-value, which is at 33% vs. 39% at the end of the last financial year.

Adjusted earnings increased by 15%, although most of that is because of lower net finance costs because debt was reduced. Like-for-like net rental income only increased by 2.3%.

The interim cash dividend is 0.72 pence per share, which works out to around 16 ZAR cents. The current share price is around R5.88.

A massive payday for Liberty Two Degrees shareholders (JSE: L2D)

There’s nothing quite like a 42% jump in the share price in a single morning

Liberty Group wants to take Liberty Two Degrees private. This will be via a scheme of arrangement, with a proposed cash price of R5.55 per share. Liberty Two Degrees closed at R3.90 the day before the announcement, so that’s a lovely premium for shareholders. Well, recent shareholders at least. If you held since listing, then I’m afraid you’ve had a bad time:

The net asset value per share at the end of December 2022 was R7.51, so Liberty is also getting a pretty good deal if we believe that number.

You may recall that Liberty Group is now a wholly-owned subsidiary of Standard Bank Group. This deal is ultimately a big property play by Standard Bank.

Liberty group already owns around 61% of the shares in Liberty Two Degrees It also owns 66.7% in the underlying portfolio, with Liberty Two Degrees holding 33.3%. In other words, this transaction is about taking out the minority shareholders.

Mazars Corporate Finance was appointed as independent expert on this one, concluding that the transaction is fair and reasonable to Liberty Two Degrees shareholders.

Non-binding letters of support have been received from Coronation (holding 22.5% of the shares or 61.1% of shares eligible to vote) and Sesfikile Capital (holding 1.3% of the shares or 3.6% of shares eligible to vote). This gets them very close to having a successful scheme of arrangement, which requires 75% approval.

Hot potato Royal Bafokeng Platinum is loss-making (JSE: RBP)

Impala Platinum will need to work this asset

Things aren’t great in the platinum group metals (PGM) industry at the moment. Royal Bafokeng Platinum is dealing with additional issues, like operational challenges at the Styldrift mine and a decrease in production.

Even if production went according to plan, it’s hard to do well when the rhodium price tanked by 50% and the 4E basket price fell by 23.6%. As a further squeeze on profitability, mining costs increased by more than CPI inflation.

The headline loss per share is a nasty -113.8 cents, which is way off HEPS of 767.3 cents in the comparable prior period. Impala Platinum is about to own this entire thing, so hopefully it can only get better from here.

Sirius recycles capital in the UK (JSE: SRE)

In other words, it has bought properties after recently selling a couple

In the property sector, funds are forced to “recycle capital” because raising money is expensive. There was a time on the JSE a few years ago when property groups could raise seemingly endless capital in literally a couple of hours. The days of accelerated bookbuilds are long gone, so management teams must earn their salaries by buying and selling properties intelligently.

Sirius Real Estate has announced that UK subsidiary BizSpace has acquired two mixed-use industrial assets for £9.5 million on a net initial yield of 9.6%. This comes after recent sales in the UK at a combined premium to book value. Sirius will want to demonstrate value creation to shareholders by actively managing these new assets.

Spur: people with a taste for Italian (JSE: SUR)

I have fond memories of the Doppio Zero group from my Joburg days

The Doppio Zero / Piza e Vino / Modern Tailors group is focused on Gauteng, so don’t feel bad if you haven’t heard of the restaurants in other provinces. In fact, with a footprint of 37 franchised and company-owned restaurants, only 4 of them are outside of Gauteng.

Spur is acquiring a 60% stake in the chain, as well as the central supply business and bakery. The sellers are the founders, who will remain as executives of the group for a minimum of five years.

The rationale for the deal is to almost double the size of Spur’s “speciality” portfolio, which includes The Hussar Grill, Nikos and Casa Bella.

The Doppio Zero group generated total sales of over R600 million in the year ended February 2023. That’s impressive for a group that was only founded in 2002 as a bakery and cafe in Greenside! There are 669 employees.

The announcement doesn’t disclose the transaction value. It also doesn’t indicate whether there are put / call option structures over the remaining 40%. For the sake of the founders, I hope they negotiated a liquidity mechanism to realise the rest of the value after the five year period as executives.

Super Group reports a super jump in earnings (JSE: SPG)

These are properly impressive numbers in this environment

For the year ended June 2023, Super Group has reported a 20% to 27% increase in HEPS. That’s juicy. Even more impressive is the fact that the base period included once-off benefits of 38.8 cents per share in the HEPS number of 380.7 cents.

The narrative sounds good, with market share gains on the top line and solid cost management to boost profitability. On top of this, the group remained highly cash generative. This supports the ongoing strategy to look for useful acquisitions to supplement organic growth.

The earnings range for the period is 456.8 cents to 483.5 cents. The share price is just over R35, suggesting a Price/Earnings multiple of around 7.5x.

Trustco finally announces the Meya Mining deal (JSE: TTO)

Perhaps unsurprisingly, it’s complicated

The overall story here is that Trustco has raised $75 million for the completion of the Meya Mining development, a diamond mine in Sierra Leone. If you read carefully though, it looks like only $50 million is confirmed.

Sterling Global Trading is subscribing for shares in Meya Mining for $25 million. This gives the company a 70% shareholding. Trustco Resources will hold 19.5% and Germinate will hold 10.5%.

On top of this, Sterling will advance a loan of $25 million to Meya. A mystery market lender is going to lend another $25 million, taking the total to $75 million. It sounds like only the $50 million has been finalised, though.

Trustco is going to subordinate its shareholder loan of $45.4 million in favour of this new debt. In other words, the new debt is repaid first and takes preference in a liquidation event.

Trustco has invested $116 million in this asset since inception. I’m not sure if this included any debt that has been previously repaid, but the current subscription price implies an equity value of $35 million. If we add in the shareholder loan, we get to Trustco having total value here of $45.4 million + $6.8 million = $52.2 million. That sounds like a significant loss, but I’m happy to be corrected here.

This is a Category 1 transaction and so a circular will need to be distributed to shareholders. Irrevocable undertakings have been received in respect of 63.26% of shares in issue, so that should be a done deal as it only needs an ordinary resolution.

Little Bites:

- Director dealings:

- An independent non-executive director of RECM & Calibre (JSE: RAC) bought shares worth R516k.

- An independent non-executive director of Balwin (JSE: BWN) has bought shares in the company worth R135k.

- Weirdly, the CEO of Argent Industrial (JSE: ART) is now selling shares after buying just a couple of weeks ago. The sale was for R51.8k.

- A director of Mantengu Mining (JSE: MTU) has bought shares worth R31k.

- Anglo American Platinum (JSE: AMS) has named Craig Miller as the incoming CEO to replace Natascha Viljoen from 1 October. Viljoen is moving into the COO role at Newmont Corporation. Miller is currently the finance director, a role he has held since 2019. This means that the company needs to find a new finance director, with no successor named as of yet.