Balwin: an ongoing lesson in optics (JSE: BWN)

The outlook is worrying and so is some of the narrative

If ever there was a company that desperately needed to invest in an investor relations / PR team much earlier in its life, that would be Balwin. Over time, institutional investors were put off the stock and the valuation struggled as a result. In the latest result, we see yet more evidence of this.

In case you think this is just my opinion, I saw quite a bit of commentary on Twitter on Friday from respected local accounts with an overall negative sentiment towards Balwin.

Let’s start with the good news, which is that HEPS for the year ended February 2023 is expected to increase by between 16% and 21%. A focus on gross profit margin was a major contributor here.

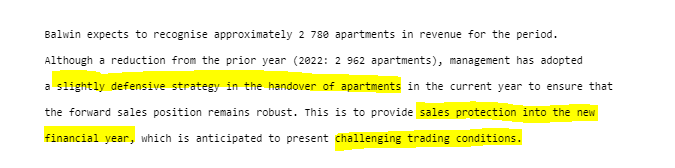

We then arrive at this wonderful paragraph, which in my mind is just a long-winded way of saying that the management team tries hard to deliberately smooth the earnings profile:

Happy to take different views here, but I’m pretty sure this means that sales were deliberately pushed out to FY24 because management is scared about what the coming year will bring.

Speaking of the coming year, here’s another unpleasant paragraph for investors:

No wonder they have a “slightly defensive strategy” going into FY24. Selling complexes in a complex trading environment isn’t any fun.

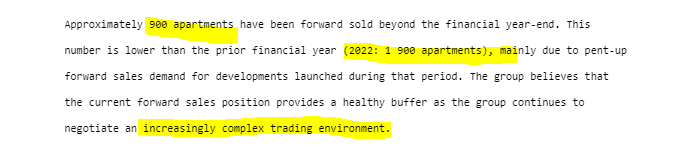

I’ll hit you with one more screenshot, as there’s another paragraph that I think is a pretty clear sign of troubles to come:

What is a CEO Loyalty Program? I truly have no idea. But aside from other incentives that won’t do gross margin any favours, the planned rental guarantee worries me. Buy-to-let is a truly horrible investment in a high interest rate environment, especially in Gauteng (the bulk of Balwin’s revenue) where tenants hold more power in negotiations than landlords. Any initiatives to make this “better” to drive sales volumes can only hurt Balwin’s margins.

This announcement gives off a very strong smell of desperation around sales volumes going into FY24. The share price closed at R3.05 on Friday, which is a trailing Price/Earnings multiple of just under 3.4x at the mid-point of the earnings range for FY23.

Does that make it cheap? Read the commentary I’ve highlighted above and decide for yourself.

Capital & Regional sells The Mall (JSE: CRP)

This has to be the least original name in the history of property

Capital & Regional has announced the disposal of The Mall, a shopping centre in Luton. This reminds me of when Ferrari named a car LaFerrari, literally “the Ferrari ” – about as imaginative as The Mall!

The price is £58 million and all the proceeds will go to the secured lender. There’s no equity in this thing. Capital & Regional was acting as property and asset manager for The Mall and earned fees of £1.4 million in 2022, a deal that now falls away with the disposal of the property.

Montauk Renewables swings into profitability (JSE: MKR)

This wasn’t enough to stop the share price dropping 17.7%

Very few people know anything about this company. It doesn’t help that you have to dig through a 10-K form for information, a format familiar to Americans rather than South Africans. This is because the company is listed on the Nasdaq!

Montauk is primarily focused on the recovery and processing of biogas from landfills to use as a replacement for fossil fuels. The group is one of the largest US producers of Renewable Natural Gas (RNG). It’s an interesting place to play, with strategic initiatives like generating biogas from dairy manure.

The engineers specialising in cow poo have probably found a better way to explain this at the dinner table on a first date.

In the year ended December 2022, the company grew revenue by 39% and EBITDA by a lovely 158%. This turned a headline loss of $2.9 million into headline earnings of $38.7 million for the year.

Montauk may get very little attention locally, but it’s a R18.6 billion market cap company. It has unfortunately lost 60% of its value in the past six months. The challenge seems to be that the company missed earnings estimates, with concerning earnings guidance for the next financial year.

The results of the Premier offer were announced early (JSE: PMR)

Brait (JSE: BAT) has raised R3.6 billion through the share placement

Premier Group’s listing will become effective on 24 March. From that day onwards, typing JSE: PMR into a trading system will give you something new to look at!

In the meantime, Brait has raised R3.6 billion by placing roughly 66.9 million shares. Titan (Christo Wiese’s investment group) took up its cornerstone shares (36.16% of the offered shares, not the entire company) and will take another 15.45 million shares which weren’t taken up in the offer. That’s a big chunk going to the underwriter, which makes me wonder about demand for this listing.

Stabilising actions regarding the share price are allowed for 30 calendar days after the admission date. After that, we will see true price discovery.

Richemont simplifies its listing structure (JSE: CFR)

The depository receipts will be a thing of the past

The best way to have learnt about Richemont’s depository receipt programme has always been to try and work out any of the earnings multiples from scratch. As you shake your head over and over again at the silly numbers your calculator is displaying, you finally work out that one Richemont “share” on the JSE isn’t actually equivalent to one share in the company.

A depository receipt programme is a way to list an instrument on an exchange that is linked to the shares in the underlying group, not always in a 1:1 ratio. This is the case at Richemont. To simplify this archaic structure, Richemont is going to get rid of the depository receipt programme and will instead list its “A” shares (the class for people whose surname isn’t “Rupert”) on the JSE.

This will make life easier for everyone. It will also facilitate cross-border trading in these shares on the JSE and the SIX Swiss Exchange.

Depository receipt holders will receive one “A” share in exchange for 10 depository receipts that they own, free of charge.

Fractional entitlements will be paid out in cash based on the volume weighted average price, less 10%. Read the circular if you’re a shareholder.

SA Corporate Real Estate inches forward (JSE: SAC)

The market can now digest results alongside the latest deal news

If you’ve been reading your Ghost Bites, you’ll know that SA Corporate is making a play for Indluplace (JSE: ILU). The goal is to substantially increase the size of SA Corporate’s residential property portfolio, making it a “buy-to-let” investment at scale.

For the year ended December 2022, the company managed mid-single digit improvements across most key metrics. Funds from operations (FFO) increased by 5.3% and the distributable income increased by 5.5%, as did the distribution itself. The net asset value only increased by 2.5% to 410 cents.

The company managed to offset the impact of a higher weighted average cost of debt of 9% by having less debt on the balance sheet. Net finance costs were flat year-on-year thanks to this. Despite the lower debt, the loan to value ratio has increased from 37.4% to 38.1% if you exclude derivatives, or a drop from 38.5% to 37.8% if you include them.

At a closing price on Friday of R1.89 per share, the dividend yield is 12.8%. The share price has fallen over 21% this year.

Little Bites:

- Director dealings:

- The CEO of Invicta (JSE: IVT) bought shares worth around R8.4 million. Importantly, several directors of Invicta also bought Invicta preference shares (JSE: IVTP) worth R9.6 million. The share price is slightly down year to date and has been trading in a range since mid-2022.

- Niel Birch’s retirement date as CEO of Novus (JSE: NVS) has been confirmed as 31 March 2023. He will consult on the integration of the Pearson South Africa deal, a very important strategic move for Novus. On an interim basis, Andre van de Veen of A2 Investment Partners has been appointed as executive chairman for six months.