Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

A very odd turn of events at Barloworld (JSE: BAW)

The market panicked on Friday

Barloworld’s share price fell 12.5% in just one day – and traded volumes were nearly 3x higher than the average day. The intraday move was even more severe, with an initial drop of 24% in response to a worrying SENS announcement. Believing that the move was overcooked and hoping that the gap would close, some punters bought in the afternoon and reduced the extent of the pain on the day.

The reason for this chaos? A voluntary self-disclosure to the US Department of Commerce, Bureau of Industry and Security regarding potential export control violations relating to sales of certain goods to the Russian subsidiary.

When the Russian sanctions came out, Barloworld (which is not an American company of course) took the practical approach of trying to manage the situation in a way that doesn’t leave the Russian employees high and dry. Unlike US firms that basically had to donate their businesses to oligarchs, Barloworld did the smart thing and managed the problem. This is of course a very technical issue though, with potentially severe outcomes if something is wrong, hence why the market panicked on the news of even a potential violation.

For now, there are more questions than answers. The market hates that.

Choppies is selling a hot potato to related parties (JSE: CHP)

Throwing good money after bad is rarely advisable

Choppies has announced the disposal of Mediland, a medical equipment and consumables distribution business in Botswana. Mediland is owned by Kamoso Group, which in turn is 76% held by Choppies. There are a number of other related party triggers going on here, including the Chief Compliance Officer of Choppies being one of the parties willing to take Mediland off the group’s hands.

Choppies acquired Kamoso in July 2023 and thus Mediland on an indirect basis as well. Mediland has been suffering losses for so long that Choppies doesn’t see a path to profitability and won’t be investing new capital in the entity. The most recent annual loss is BWP 8 million.

The current CEO of Mediland and the Chief Compliance Officer of Choppies will buy Mediland for a nominal amount, as the equity is worthless. More importantly, they will take over the revolving trade credit facility obligation of BWP 40 million and settle it over five years.

The buyers have also agreed not to retrench any staff, so good luck to them trying to turn the business around.

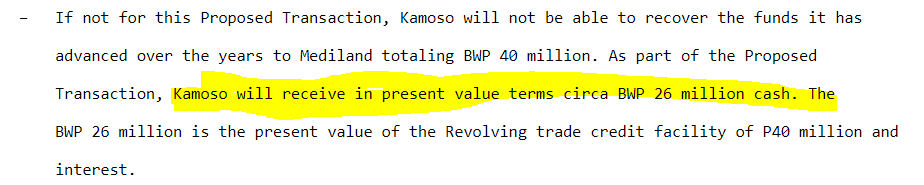

The problem is that the BWP 40 million is owed to Kamoso, not an independent bank, so any hope of recovering that amount rests with the buyers finding a way to improve the business. While the facility is outstanding, no dividends can be paid by Mediland.

There’s a very dicey paragraph in the announcement that in my view doesn’t reflect the reality of the deal. If Choppies is lucky, Kamoso may receive repayments on the BWP 40 million facility, partially or in full. This paragraph makes it sound like there’s an up-front payment, which there isn’t:

Kore Potash is close to getting the EPC agreement signed (JSE: KP2)

The company is valuing its exploration and evaluation assets at $173 million as at June

Kore Potash has released its financial report for the six months to June. If you’ve been keeping even half an eye on the group, you’ll know that the focus has been on trying to conclude an Engineering, Procurement and Construction (EPC) contract with PowerChina. This has been going on since 2022!

Construction companies can literally go bankrupt if they get contractual terms wrong, hence why we are here two years later and still reading about the conclusion of this contract. PowerChina has put maximum effort into avoiding getting it wrong, including an extended period of having representations on the ground with Kore Potash to develop the project plan.

After recent meetings in Beijing and Dubai, the agreements are now sitting with legal counsel of both parties for finalisation. Once that is complete, a signing ceremony will need to be arranged in Brazzaville, with the Minister of Mines of the Republic of Congo as a key signatory.

This process should give you insight into both the risk and potential reward at junior mining groups. Kore Potash values its exploration and evaluation assets at $173 million as at the end of June and is sitting on cash of just under $1 million.

They are close now, with the share price up around 220% this year in appreciation of their efforts. Of course, nothing is guaranteed until there’s a signature.

MTN releases the circular to extend MTN Zakhele Futhi (JSE: MTN)

This deal is a great example of why B-BBEE deals need to be structured more carefully

MTN’s B-BBEE deal was designed to give investors exposure to the entire group, not just South Africa. This is why MTN Zakhele Futhi holds shares in the listed group.

History has shown us that this probably isn’t the best way to do things. For comparison, MultiChoice’s B-BBEE structure (Phuthuma Nathi) is based on the South African subsidiary only, which means those shareholders aren’t subjected to all the volatility in Africa. It also means that the MultiChoice deal isn’t based on a listed share price that can be thrown around. Finally, the MultiChoice deal doesn’t have an expiry date, whereas the MTN deal does – and this simply adds to the risk when referencing listed shares that might be going through a rough patch as that date approaches.

So, for quite a few reasons in the end, here we are: the MTN Zakhele Futhi structure is being extended for three years to avoid it expiring worthless or close to worthless later this year. They estimate the break-even point (i.e. where the shares held in the structure can cover the debt) to be R88 per MTN share. The group is trading at R94 per share but has recently been below R73 per share.

The costs of restructuring these deals is no joke, with nearly R22 million in fees for MTN, of which R10 million will be going to RMB as financial advisor, as well as a gigantic R33 million in fees incurred by MTN Zakhele Futhi, with Tamela Holdings making R18.6 million as financial advisor and sponsor – in addition to the R2 million they made from MTN group as lead sponsor. MTN Group is going to bear all the fees anyway, so that’s a cool R55 million in fees just to keep the deal alive.

One day, someone with time on their hands should do a study on the fees earned by investment bankers vs. the value actually created for B-BBEE scheme shareholders over the past two decades in South Africa. I suspect that the results would be shocking.

Nampak wants to incentivise its key executives – but the share price ran away from them (JSE: NPK)

The company has released a circular to deal with this issue

Nampak has been under new management for the past 12 months. Due to the need to recapitalise the company, followed by a cybersecurity issues that caused further delays, they haven’t been able to finish off the plan to incentivise and align top executives Phil Roux and Glenn Fullerton.

Last year, the directors complied with the initial requirement to acquire R4 million worth of shares each at R175 per share. The problem is that the share price has gone a little nuts recently, currently trading at R435. To incentivise the directors at that price wouldn’t be fair, as they would lose out on the upswing from the first year of the turnaround.

To get around this problem, Nampak wants to issue further shares to the two directors at a price of R175 per share. This looks like a huge discount to the current price (and it is), but I also understand the arguments why. The share subscriptions will be funded by loans from the company of R16 million to Phil Roux and R10 million to Glenn Fullerton.

You can read the circular here.

Nibbles:

- Director dealings:

- A prescribed officer of Standard Bank (JSE: SBK) sold shares worth just under R3 million.

- Titan Premier Investments, one of Christo Wiese’s main investment vehicles, bought another R755k worth of shares in Brait (JSE: BAT).

- Associates of a director of Brimstone (JSE: BRT) bought shares worth “N” ordinary shares worth R270k and ordinary shares worth R59k.

- Mondi (JSE: MNP) has confirmed the exchange rate for its interim dividend, with South African shareholders due to receive 459.48435 cents per share.