Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Collins should become a REIT this year (JSE: CPP)

This will trigger the declaration of a dividend

Collins Property Group (previously Tradehold) released results for the six months to August. The net asset value (NAV) per share has increased from R12.40 at 28 February 2023 to R12.62, with the share price closing at R6.97 and reflecting a significant discount to NAV that is common on the JSE.

Strategically, the group is focused on offshore expansion, particularly in the Netherlands. They are also looking at Germany. The group already owns six assets in Austria. To fund this, properties in South Africa are being sold, although the group is happy to increase its exposure to the Western Cape.

Concerningly for the economy at large, vacant space in the portfolio of mainly industrial warehouses increased from 3% in February 2023 to 4.04%. This was due to smaller tenants downsizing or closing up shop entirely. Not good.

The group is currently trying to convert to a REIT. Once that process is completed, they intend to declare a dividend.

There might be a takeover on the table for MC Mining (JSE: MCZ)

Also, there might not be

MC Mining is also listed in Australia. If you know anything about Australians, you’ll know that they are very strict when it comes to rules. Their takeover code has some differences to South Africa and you don’t want to get on the wrong side of it, so you’ll sometimes see unusual terminology in announcements related to Aussie-listed companies.

This is why you’ll see “take no action” in the heading of the latest SENS announcement by MC Mining. This is because although MC Mining has received a proposal letter from Senosi Group and Dendocept, there are certainly regulatory dispensations being sought that make the offer conditional at best.

The letter is described as being on behalf of shareholders and associates representing in aggregate 64.5% of the issued capital in the company. Further down, Senosi is noted as owning 23.4% and Dendocept holds 6.9% of shares outstanding. The maths isn’t mathing here and I’m not 100% sure what the reason for the difference is.

The point is that these two parties want to form a consortium to make an off-market cash offer for all the shares not currently held by the consortium. A letter had been previously sent to the board in September about an indicative offer, but it was an incomplete proposal. A pricing range of A$0.20 to A$0.23 per share was given in that letter. The latest letter doesn’t give an idea of pricing, but the previous range is obviously an interesting anchor.

The market latched onto it, with the share price jumping over 17% after the release of the announcement.

For now, the board has advised the market to take no action in regard to this proposal until further guidance has been received from the independent board committee.

If only MTN Uganda was bigger… (JSE: MTN)

Here’s some strong growth ahead of inflation

After MTN Nigeria released a very worrying update and MTN Ghana put out big growth numbers that are sadly below in-country inflation (and thus reflect negative real growth), it was good to see MTN Uganda grow EBITDA by 15.6% in a country where inflation is only 3.3%.

It looks good on literally all metrics, with subscribers numbers up and service revenue growing by 15.2%. while data revenue grew 22% and fintech revenue grew 18.1%. EBITDA margin was stable at 50.6%, which is also quite a big deal in this environment. Another important number is capital expenditure, which only increased by 4.7%.

MTN Uganda is also declaring cash dividends.

Is this the jewel in MTN’s African crown? It just might be. For MTN shareholders, the pity is that this is one of the smaller jewels, even though it might be the brightest.

Murray & Roberts reflects on the year that was (JSE: MUR)

There’s also news on the balance sheet

Murray & Roberts has lost three quarters of its value this year. There have been some ugly performances on the market, but Murrays makes a strong case for itself as one of the biggest disappointments.

At the AGM, the company reflected on some of the major points in the last financial year. Essentially, the balance sheet broke and couldn’t sustain the Australian business, so they put that side of things into voluntary administration and focused on keeping the rest of the group alive.

The balance sheet as at 30 June 2023 holds an important lesson. Net debt is only R300 million, but international groups are more complicated than simply a “net debt” number – and the clue is in the first part of that name. This is gross debt net of cash, but what if the gross debt and the cash are in two different places?

Murray & Roberts has R1 billion in debt in South Africa and its cash is predominantly offshore. To address this issue, the North American business units have revised their debt facility with their bankers and they will pay dividends to Murrays in January and June 2024. Other initiatives will add another R180 million to the pot for debt reduction, with the hope that South African debt will reduce from the current level to R300 million by June 2024.

It was R2 billion in March 2023, so that would be a massive improvement.

There’s a particularly interesting comment that the board is not considering a rights issue to reduce debt, but it is working towards a “sustainable capital structure” over the next six months, including a refinancing of debt. My view is that the risk is never gone until the balance sheet is completely fixed.

In other news, the Mining platform has grown its order book since June 2023. Sadly, the Power, Industrial & Water platform still has no “near orders” on the books. Finally, as previously announced, the company will still target opportunities in Australia on a selected basis.

It’s a smaller group now. Within the next year, it might even be a sustainable group. That won’t help shareholders recoup their losses in the near-term, but at least people will keep their jobs.

Pepkor’s like-for-like growth is still problematic (JSE: PPH)

There’s improvement at Ackermans, but HEPS for the year is in the red

Pepkor’s group revenue for the year ended September was 7.7% higher, but of course we need to dig a lot deeper than that. The first adjustment is for the 53rd trading week in this period. If we exclude that, revenue was up 6.5%.

It was firmly a tale of two halves, with growth of only 4.3% in the first half and a better performance in the second half.

Avenida in Brazil is working out well, now contributing 4.3% to group revenue vs. 2.4% in the prior year (as it was only acquired during that year). Most importantly, this is in line with guidance and well ahead of the original envisaged performance. I liked the thought of a South American expansion when that deal was first announced, as it feels like a more natural market for South Africans to enter.

Like-for-like sales growth is such an important metric, as it shows the underlying performance in the business. PEP managed 4.5% like-for-like growth for the full year, which means negative volumes because inflation was 7.3%. This is a direct result of pressure on local consumers. I must also point out that 4% of PEP’s sales are now on credit, vs. 0% historically.

Although Ackermans had a better second half after a disastrous first half, it could still only manage a like-for-like sales decline of 5.1%.

JD Group experienced a 2.1% decline in like-for-like sales and The Building Company was down 0.8%.

Due to impairments, there is going to be a collapse in reported earnings and Pepkor will report a loss. This is a function of underlying business performance and higher discount rates. Based on headline earnings from continuing operations, the expected drop is 5.2% to 15.2%.

The share price is down around 10% year-to-date.

Sibanye-Stillwater published a novel on SENS (JSE: SSW)

This quarterly update is huge

For the quarter ended September, Sibanye-Stillwater’s EBITDA was just over R3 billion. In the quarter ended June, it was R6.4 billion. In the quarter ended September 2022, it was R8.5 billion. Hopefully you now understand why (1) the share price broke and (2) this quarterly update is practically a published novel on the underlying performance.

In fact, it’s so huge that it has a table of contents!

You are welcome to go read the entire thing. The key points for the purposes of Ghost Bites are as follows:

- EBITDA has gotten worse in all major operations, with the exception of zinc in Australia

- The average basket price for the commodities has gone in the wrong direction (again, other than for zinc)

- Against this backdrop of price pressure for commodities, all-in sustaining cost has increased because of inflationary pressure in costs

- Restructuring activities are underway in the South African gold and PGM operations to try and address the slide in profitability

Sibanye’s share price has fallen 49% this year.

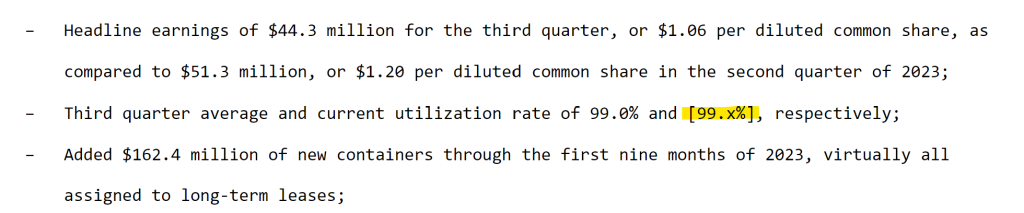

Textainer releases third quarter results (JSE: TXT)

Remember, the company is currently the subject of a takeover bid

Textainer has released numbers for the third quarter of 2023. Unfortunately, they also include this number:

Leaving aside the Dezemba levels of proofreading going on here, net income for the third quarter was $1.07 per share, down from $1.20 per share in the second quarter. Although the share repurchase program has been suspended in light of the potential transaction with Stonepeak, a dividend of $0.30 per share has been declared.

Little Bites:

- British American Tobacco (JSE: BTI) announced that Soraya Benchikh will join the company as CFO from 1 May 2024. She is currently President, Europe at Diageo, one of the largest alcoholic beverage groups in the world.

- They won’t win any corporate governance awards for this one, but Primary Health Properties (JSE: PHP) has announced the founder and CEO as the new non-executive chairman. Harry Hyman is stepping down as CEO, so he is moving straight into the chairman role. To make up for it, the company will beef up the independent non-executive directors.

“For the quarter ended September, Sibanye-Stillwater’s EBITDA was just over R3 billion. In the quarter ended June, it was R6.4 billion. In the quarter ended September 2022, it was R8.5 million.”

September 2022 should read R8.5 billion

100% – thanks Ian, and fixed. Although with some of the volatility we are seeing at the moment, we can’t rule out being in the millions at some stage! Appreciate it.

I love it:

Insightful; and also

“… Dezemba levels of proofreading …” 🙂

I think we might have three months of Dezemba this year!