Conduit Capital sells another business (JSE: CND)

Constantia Risk and Insurance has attracted a buyer

Before you get confused, the subsidiary within Conduit Capital that suffered liquidation is Constantia Insurance Company. There were a couple of other businesses within the group that could be sold to help it at least realise some value.

One such entity is Constantia Risk and Insurance, which is being sold for R55 million. The buyer is TMM, a diversified pan-African investment group. Half of the purchase price will be held in escrow due to the liquidation process within the broader group and the potential for claims. This means that the money will be kept on one side to settle such claims if they arise. If the claims never come, the money will be released.

Negative Delta (JSE: DLT)

The property fund is struggling

In maths, delta is the symbol for change. The change in earnings at Delta Property Fund is unfortunately negative, with distributable earnings per share for the year ended February 2023 expected to be between 69% and 74% lower than the prior year.

This is a function of the issues plaguing the entire sector, ranging from negative reversions through to vacancies and higher interest rates.

“Distributable” is a relative term here, as there’s no dividend anyway for this period because of the challenges being faced.

Indluplace releases detailed results (JSE: ILU)

With 9,282 residential units, this is buy-to-let delivered at scale

Indluplace is more than just a residential fund, with a significant retail portfolio as well. The portfolio value is R3.4 billion and the company is currently under offer from SA Corporate Real Estate (JSE: SAC) for R3.40 per share. The price is now anchored to that number, trading at a slight discount to take into account the time value of money and what seems to be low deal risk.

There isn’t much for investors to think about here in terms of the share price because of the offer, but it’s interesting to note that residential occupancies improved from 89.7% to 94% over the past year and the student portfolio is back up to 98% from a dire level of 43% in March 2022.

The net asset value (NAV) per share is 5.5% lower at R6.5983, so the offer price is a discount to NAV of roughly 48.5%.

As highlighted previously by Indluplace, there is no distribution based on these interim numbers but there will be a clean-out distribution before the scheme is implemented, assuming all goes ahead.

MiX Telematics will have tricky results to work through (JSE: MIX)

A trading statement reveals a major impact on earnings from deferred tax

With detailed results due to be released on Thursday this week, MiX released a trading statement on Wednesday giving an indication of earnings. This is another great example of a company releasing a trading statement far too late in my view. It’s meant to be an early warning system, not something that comes out one day before results!

HEPS will be between 42% and 46% lower than the in year ended March 2022. This is mostly because of a deferred tax charge on forex movements linked to an intercompany loan. Investors will need to dig into this properly to understand it, with adjusted earnings per share (excluding the forex move and tax) actually increasing marginally.

Liberty Two Degrees’ pre-close update is worth a look (JSE: L2D)

There are useful insights here into the broader retail environment

Liberty Two Degrees has exposure to some of the strongest properties in the country. This is a quality portfolio, yet it certainly hasn’t been immune to what has been going on out there. For example, office occupancy remains problematic at just 80.7% vs. retail occupancy of 97.7%.

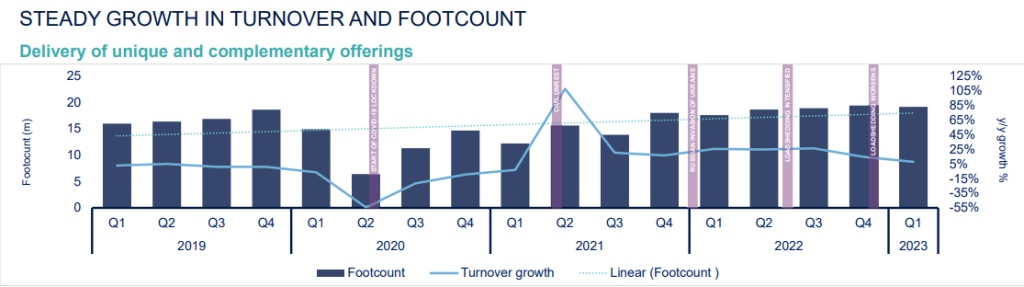

But for me, the most interesting part of the update is the charts that give us an indication of the operating environment. For example, this chart from the update is pretty interesting, although that y-axis for growth is wild if you look closely:

It tells the story of the pandemic: wild volatility, huge pain in 2020 and then a strong recovery in 2021 driven by global stimulus. 2022 was a consolidation year, with 2023 growth taking a knock from load shedding.

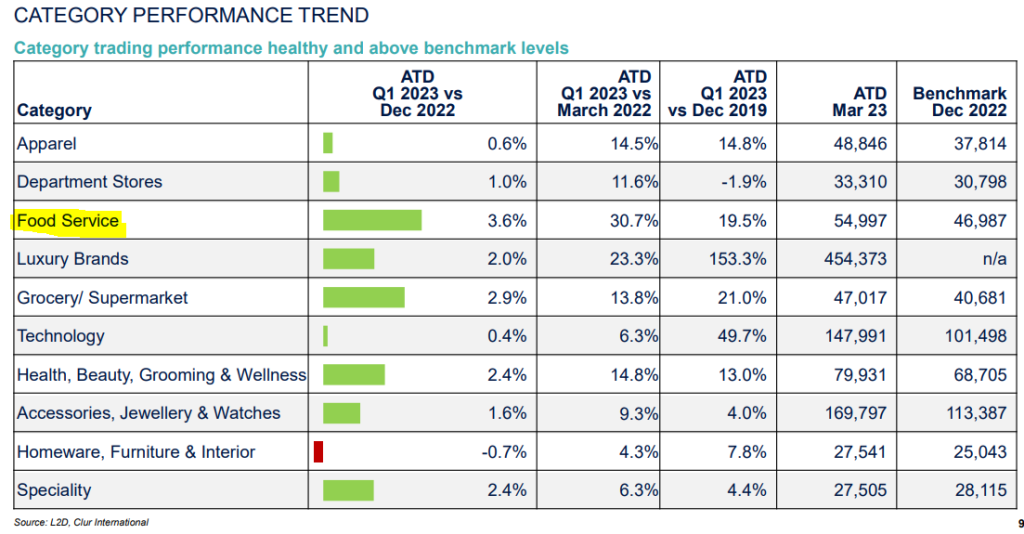

Here’s another interesting graphic, which supports my view that fast food businesses are doing very well in this environment (despite Famous Brands telling us otherwise):

And in hospitality, occupancies are up sharply and there were 67 events at the Sandton Convention Centre between January and April 2023 vs. 47 in the same period last year. Investors in hotel groups will also be pleased to know that RevPar (a measure of room pricing) has increased significantly vs. 2022.

Nampak calls 2023 a “defining year” – no kidding (JSE: NPK)

Interim CEO Phil Roux sounds believes in the future of the business at least

It is entirely possible that Nampak can emerge from this mess as a sustainable business. It’s also possible for shareholders to lose a ton of money along the way, despite a rally of 9% after the release of results on Wednesday. I would remind you that even over 3 years (which means the worst of the pandemic as a starting point), the share price is down 44%.

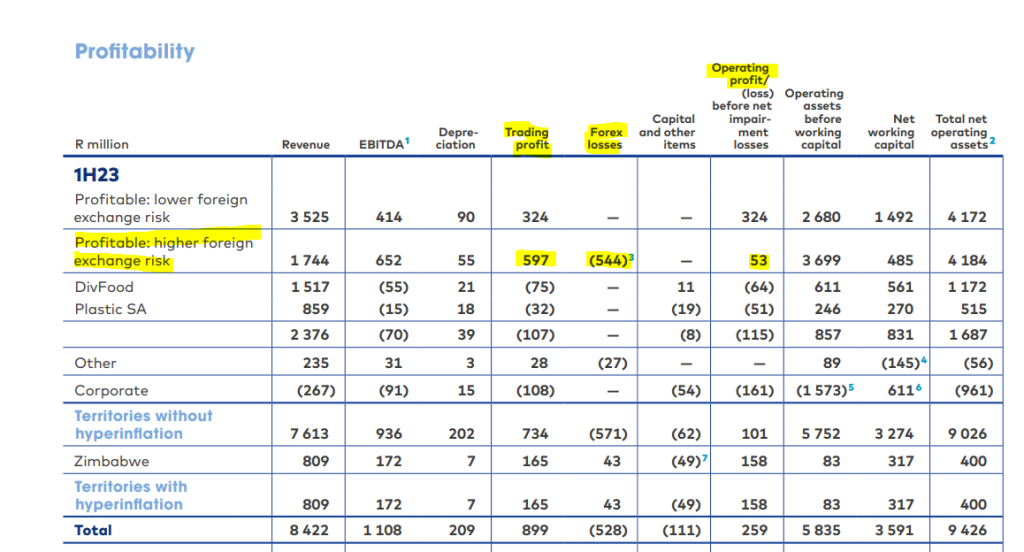

With revenue of R8.4 billion and trading profit of R899 million, this hardly sounds like a basket case. But once you include net forex losses of R571 million because of Angolan and Nigerian profits, the situation deteriorates rather quickly. Operating profit before impairment losses was R259 million for the six months ended March and net finance costs were R494 million (up by a whopping 77%), so not even the debts are being serviced by these assets, let alone the shareholders.

Even if we ignore the very large impairment losses, the headline loss for just the interim period is R342 million.

Is there any good news? Well, the originally envisaged rights offer of R1.5 billion has been reduced to a rights offer of R1 billion. A circular will be published at the end of May to this effect. With a market cap of under R500 million, this is still a massively dilutive rights offer.

In addition to the rights offer, there is an asset disposal plan that needs to be delivered before Nampak can breathe a sigh of relief on the balance sheet.

Finally, if you really want to understand how severe those forex losses are, take a look at this:

The tide went out on Premier Fishing’s profitability (JSE: PFB)

HEPS has more than halved

For the six months to February 2023, Premier Fishing and Brands suffered a significant drop in profitability. HEPS has tanked by between 51.56% and 71.56%, which means interim HEPS of between 0.87 and 1.49 cents per share.

That share price of R1.62 is looking very high relative to those earnings.

No further details behind the drop are given in the trading statement, but detailed results are due this week.

Reunert is on the right side of this environment (JSE: RLO)

When industrials businesses do well, they tend to do really well

Most industrials in South Africa are struggling at the moment, with load shedding as a major driver. But with significant export and renewable energy businesses, Reunert is about as well positioned as one can hope to be in this environment.

In the six months to March, revenue is up 21% and operating profit increased by 33%, so the joy of operating leverage is coming through here. We need to be careful though, as this period included a business interruption insurance payout of R44 million. Without that, operating profit would be 23.8% higher, so the positive operating leverage effect is far more muted than initially appears to be the case.

Major drivers of revenue growth were better cable volumes in the Electrical Engineering Segment and growth in sales in the Applied Electronics Segment thanks to demand for renewable energy products and the defence export business.

I must also note that the ICT Segment is acquiring IQbusiness, a management and technology consulting firm with revenues in excess of R1 billion. Remember this reference if someone says to you that “selling time” isn’t a business. It sure is one!

Although HEPS was 37% higher, the dividend per share is only up by 11%. This might be due to the R324 million increase in working capital across debtors and inventory.

RFG Holdings has been a beacon of hope (JSE: RFG)

There aren’t many local companies growing HEPS, let alone by 37.7%

Food producer RFG Holdings has put in a very strong performance in the six months ended 2 April 2023, with the international business operations as a major contributor. The rand has really helped here, particularly as the base period included a failed peach crop in Greece that was a temporary boost to RFG’s business.

Group revenue increased by 10.2% with price inflation of 14.8%, which means that volumes dropped. Ultimately, all that matters is total revenue, so it’s not a big deal if price increases more than make up for a drop in volumes. There are many companies out there suffering a drop in volumes even without price increases.

We do need to note foreign exchange gains and the Today acquisition that contributed 2.7% and 2% to revenue respectively. This means that the group volume decline was actually 8.5%, so RFG’s ability to still grow HEPS in this environment is very impressive.

Interestingly, the fruit juice category delivered the best market share gains for RFG. These food businesses are just a roll-up of a number of categories, which can make it very difficult for investors to forecast growth. A lot of it comes down to belief in the management team that they can keep doing the right things.

To give a sense of the effect of load shedding, operating profit in this period was R346 million and diesel costs were R37.8 million. This means that operating profit is roughly 10% lower than would be the case if dear Eskom was functioning.

Overall, HEPS increased by 37.7% and the group even managed to reduce net debt slightly despite net working capital increasing by 13.7%. Return on equity has increased from 9.9% to 14.1%.

Trematon’s INAV is under pressure from Generation Education (JSE: TMT)

But the overall drop in INAV is also largely due to a capital distribution to shareholders

Trematon is an investment holding company, which means that intrinsic net asset value (INAV) per share is the key metric when assessing performance. This is based on director valuations of the underlying assets and is the market standard for a company like this.

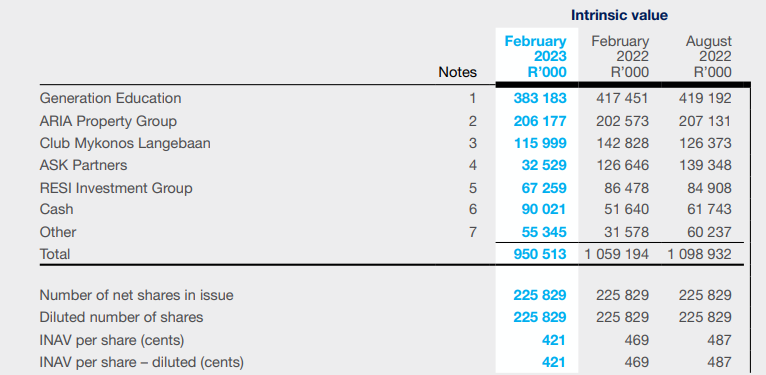

When a capital distribution is made to shareholders, this reduces the size of the group and hence the INAV. The shareholders receive that cash, so it’s not a loss in value. Of the drop in INAV from 487 cents to 421 cents as at February 2023, 40 cents was because of the capital distribution. The remaining 26 cents is because of the assets.

The major pressure was in Generation Education, where profit from operations fell from R11.5 million to R4.7 million. This was driven by slower growth in student numbers and higher costs, so margins were squeezed. The ARIA property business also suffered a drop in profitability, yet the contribution to INAV has somehow remained flat. I’ll also touch on the Club Mykonos resort in Langebaan, which generated operating profit of R3 million vs. break-even in the prior interim period.

There are various business units that you could dig into with detailed analysis. Overall, the share price of R2.45 means that the group is trading at a discount to INAV of 42%. I must point out that INAV per share should always take into account deferred tax and I see no evidence of that here (happy to be corrected if I’m wrong). Investors also need to allow for centralised costs, so this discount often isn’t as high as it initially seems.

Vunani reports a drop in earnings and the dividend (JSE: VUN)

Asset administration saved this result from being a lot worse

Vunani has a variety of business units that really need to be considered separately in order to understand the group’s results for the year ended February 2023.

The largest contributor to profit is now asset administration, achieving profit of R33.7 million out of a group total of R61.7 million. It has jumped sharply from R19.8 million in the prior year, which is just as well because there have been major negative swings in some other business units.

The only other unit with a good news story for this period is insurance, with profit of R14.6 million vs. R11.8 million in the prior period.

Businesses linked to the markets have come under pressure, like fund management where profits dropped from R37.4 million to R21.2 million and institutional securities broking which slipped from a profit of R1.4 million to a loss of R9 million. Stockbroking really is one of the toughest business models around at the moment.

Finally, advisory services increased revenue by over R12 million but somehow only managed a flat profit performance of R1.3 million.

Overall, Vunani’s revenue increased by 10% but HEPS dropped by 14.4% to 29.7 cents. The dividend of 11 cents per share puts the trailing dividend yield on 3.9% based on the current share price of R2.80.

Little bites:

- Director dealings:

- Directors of Harmony Gold (JSE: HAR) have sent a pretty clear message about where they think we are in the cycle, with two directors selling a combined R10.2 million worth of shares.

- An associate of a director of Ascendis (JSE: ASC) has bought shares worth over R373k. In a separate transaction, an associate of a different director of the company bought shares for R232k.

- A director of Brimstone (JSE: BRT) and one of his associates bought a combination of ordinary shares and “N” shares worth R70.7k.

- It’s lovely to see a censure on a director of a listed company for trading in a closed period without permission. It’s grossly unfair that these types of things happen in the market and the rules are there to protect minority shareholders who don’t sit on the inside of these companies. With many years of experience, Dipula Income Fund (JSE: DIB) director Brian Azizollahoff should’ve known better when he sold shares worth R108k in a closed period without clearance. He earned himself an embarrassing public censure and a fine of R50k. Having been in top executive roles for a long time, I doubt the fine stung very much but the censure probably did. Hopefully the public censure sends a message to directors across the JSE.

- Choppies (JSE: CHP) announced that the charge against the company by the Botswana accounting authorities for alleged non-compliance in 2017 – 2020 has been withdrawn.

- Mustek (JSE: MST) announced that its Chairperson would be stepping down at the AGM in November, with Reverend Vukile Mehana having served in that role since 2016. The board has commenced a process to find a successor.

In “Liberty Two Degrees” se verslag rapporteer julle “vacancies as 80.7% en 97.7%. Dit kan sekerlik nie reg wees nie. Moet seker besettings wees, of okkupasie. Pietman

Well spotted! And thank you. Will fix that.