Coronation’s AUM has moved sharply higher (JSE: CML)

To their credit, the lazy disclosure format is also used when they have a good news story

As you would expect after the year that we had in the markets in 2024, assets under management (AUM) at Coronation has moved higher. It came in at R676 billion as at the end of December 2024, a long way up from R629 billion as at the end of 2023.

For some reason, Coronation never discloses the comparable number in the SENS announcement, forcing investors to dig through the SENS archive to find it. I genuinely have no idea why they do this, but at least they didn’t magically change that approach now that they have a positive story to tell.

The share price is up 24% over 12 months, but is 28% lower over 3 years. In the sector, my preference is still the companies that have built their own distribution channels. You can look at PSG Financial Services (JSE: KST) to see what I mean, or Quilter (JSE: QLT) further down in this update.

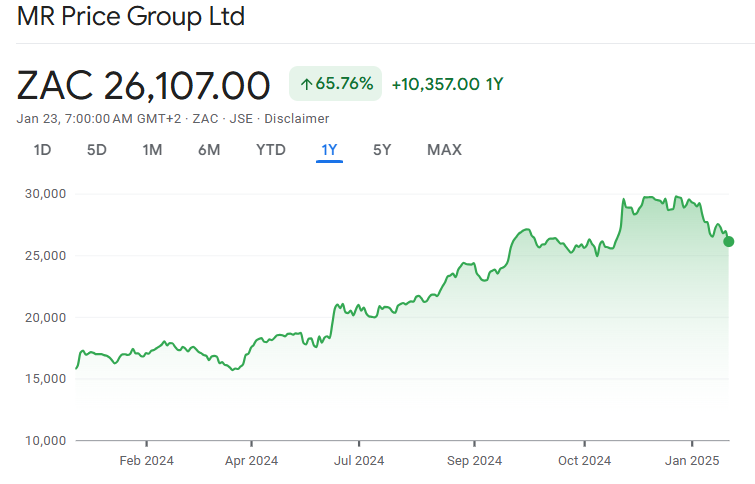

Mr Price just keeps winning (JSE: MRP)

It’s incredible how wrong I was on this one

Early last year, when the Mr Price share price started running, I wasn’t convinced by the rally. In fact, I thought it would sizzle out and possibly head lower.

Here’s a chart of how spectacularly wrong I was:

There are a few lessons here worth sharing, all of which I apply with my own money. (1) Going short is much braver than going long, not least of all because you’re betting against inflation when you’re short. I prefer to just avoid things that I feel could go down, rather than short them in the hope of a profit. I leave that for the hedge funds and traders! (2) It’s impossible to get everything right in the market (no matter who you are), so position sizing is key. I avoid a highly concentrated portfolio. (3) Momentum is a very powerful thing and the South African market loves it when a business is doing decently, so much so that getting to a P/E of over 20x is possible.

Today, Mr Price is on a P/E of 19.6x. For context, you can buy Nike on 22.6x. Do with that information what you will.

What is supporting the Mr Price story? To be fair, some really solid recent growth. In an update for the 13 weeks to 28 December 2024, they achieved double-digit sales growth and won market share as well. They managed this at a higher gross margin than in the comparable period, so it wasn’t achieving by slashing prices either. In retail, this sort of narrative is precisely what you want to see.

The two-year compound annual growth rate (CAGR) at group level is 10.3% and the latest growth is 10.6%, so that’s remarkably consistent. They’ve won market share for six consecutive quarters!

There are a bunch of other interesting nuggets in the update. For example, online sales grew 21.9% year-on-year in December, so more and more people are choosing to do their festive shopping online. This hasn’t stopped Mr Price from expanding the store footprint, with trading space growth of 4.9%.

It also seems as though people have money again, with cash sales up 11.1% and credit sales up just 5.7%. This trend is helping the entire business of course and is contributing to strong performance by recently acquired chains like Studio 88 and Power Fashion. When it comes to acquisitions though, Yuppiechef looks like the superstar. It has achieved a two-year CAGR of 18.4% and achieved its best-ever market share in December – all while increasing its gross profit margin!

This bucks the broader trend in Homeware, which was the slowest growing category at 7.9%. Although that’s a decent number in isolation, it’s much lower than 10.9% in Apparel and a really strong 16.5% in Telecoms.

Strong sales continued in January, albeit against a really tough base in which load shedding was running rampant. The performance in most of 2024 sets a difficult base off which to grow in 2025. The trailing P/E multiple is also very high, so that’s another headwind for the share price this year.

I was horribly wrong in 2024 about the share price but that doesn’t mean that I don’t still have a view on it. As always, my view is one of many you should be considering – including the most important view of all, being your own!

Personally, this isn’t a chart I want to own right now:

The fact that Mr Price closed over 3% lower despite releasing such strong numbers tells me that the market is now pricing in miracles, not just strong performance. That’s a dangerous situation.

A strong finish to 2024 for Quilter (JSE: QLT)

The momentum in net inflows is excellent

I’ve written many times about the value of building out a distribution angle to an asset and wealth management business. You need to go out there and fight for assets, as it’s too hard to hope that just sitting back and managing them will get the job done. Quilter is a great example of this and the results are clear to see.

2024 saw record core net inflows of £5.2 billion. The momentum into the end of the year was extremely encouraging, with the fourth quarter contributing net inflows of £2 billion. Most of the uptick came from the Affluent segment, boosted by Quilter’s platform business that enjoyed strong flows from both Quilter channels and independent financial advisor channels.

The combination of positive market performance in 2024 and solid inflows took assets under management and administration from £106.7 billion as at the end of 2023 to £119.4 billion by the end of 2024. That’s a particularly good performance in a year that was characterised by elections and uncertainty around tax changes for wealthy clients.

The Quilter share price closed 3% higher and is up 54% over 12 months.

Vukile’s Spanish acquisition is still on the table (JSE: VKE)

Repairs from the flood damage are going well

Last year, Vukile announced the possible acquisition of Bonaire Shopping Centre in Spain. The rain in Spain may fall mainly on the plain as the old movie goes, but in 2024 it fell basically everywhere. The torrential flash flooding caused havoc and this shopping centre wasn’t spared from the impact.

This is why every single acquisition always includes a material adverse change clause. Before a deal closes, you need to make sure you’ve got wriggle room in case something crazy happens.

The deal was delayed for a full assessment of the damage to be made. In good news, the deal is still on the table and the exclusivity arrangement that Vukile’s subsidiary Castellana has on the deal is still in force. The current owners are making progress towards fixing up and reopening the centre.

Will this affect the pricing on the deal? At this stage, we don’t know. We don’t even know if it will definitely go ahead. We do at least know that it still has a strong possibility of happening.

Nibbles:

- Reinet (JSE: RNI) has given a strong clue as to the direction of travel of its balance sheet. The company always releases the net asset value (NAV) of the Reinet Fund ahead of releasing full results. This represents most, but not all of the group balance sheet. The fund saw its NAV per share increase by 5.1% from September 2024 to December 2024, which is a strong end to the year. As at that date, the stake in British American tobacco was still included in the fund.

- Copper 360 (JSE: CPR) has acquired 100% of Mulilo Springbok Wind Power, a wind energy generation facility in the Springbok area in the Northern Cape. The project is at an advanced stage in terms of feasibility studies and engineering plans, along with fully authorised environmental impact assessments. The initial cash payment is R5 million and there are deferred cash payments of R1 million per MW of installed capacity. This obviously ticks two boxes for Copper 360: energy security and renewable energy.

- After closing the acquisition of 11.35% in Legal Shield Holdings, Trustco (JSE: TTO) has confirmed that the first tranche of 200 million shares have been issued to Riskowitz Value Fund. This increases the total issued share capital by around 20%.

- The deal between Europa Metals (JSE: EUZ) and Viridian Metals still hangs in the balance, as negotiations around funding for the deal haven’t yet resulted in anything concrete. The term sheet signed in September gives 150 days of exclusivity for the deal, so there is still time. The company has simply noted that the festive season led to delays in negotiations. Let’s hope they hit the ground running this year and get it done!

- In case anyone is keeping score, recent trades in Brait (JSE: BAT) by Christo Wiese’s investment companies (in this case Titan Premier Investments) have led to a situation in which Titan’s beneficial interest in Premier Group (JSE: PMR) has increased to 45.04%. I know it’s confusing, but Premier Group (the listed food company) and Titan Premier Investments (one of Wiese’s many private investment entities) are two completely different things.