Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Ethos will pass the Brait hot potato to shareholders (JSE: EPE | JSE: BAT)

There is very little love for Brait in the market

In a voluntary NAV update, Ethos Capital announced that the net asset value per share has increased by 1.8% over the three months to March, now at R7.44. The share price is R4.25, so the shares trade at a significant discount to NAV per share – a common problem in the market for investment holding companies.

The unlisted portfolio contributed a R0.55 increase in NAV and the listed portfolio suffered a R0.22 reduction thanks to the sell-down in Brait.

Ethos has decided to unbundle Brait ordinary shares as part of the “value unlock” for shareholders. It’s just a pity that there isn’t much value. RMB has agreed to amend existing covenants and extend debt facilities until February 2028, when proceeds from the Brait exchangeable bonds will reduce that facility.

The group is also unwinding the Black Hawk Private Equity structure, which is held by non-executive directors of Ethos and their associates. The shares will be sold back to Ethos for nil consideration, as there is debt associated with the structure. Ethos shareholders are stuck with the guarantee in respect of that debt.

I like my money, which is why I keep it far away from Ethos and Brait.

After eight years, Peter Hayward-Butt is resigning as the CEO of Ethos. Over that period, the share price has lost 55% of its value. Anthonie de Beer will take over as CEO.

Concerning metrics in Hyprop’s local portfolio (JSE: HYP)

I get so irritated by the silly things that local management teams have to focus on – like water!

Travelling abroad is a wonderful thing, but it definitely elevates your frustrations with things that don’t work in South Africa. When a property group has to include a paragraph about initiatives for backup potable water in the most important province in South Africa, it really is time to hold our politicians to much higher standards.

Property funds in the UK and Europe aren’t stressing about where the water will come from, that much I can assure you.

Leaving the basics aside, Hyprop took a risk with the Table Bay Mall acquisition (especially at the price they paid) and the dividend suffered for it. They blamed the Pick n Pay issues for the lack of dividend, but Hyprop was the only fund in the market to take that route, so I suspect it was more of a convenient excuse against the backdrop of the balance sheet pressure from the Table Bay Mall deal. Although the mall is in a fast-growing area of Cape Town, I still worry that they’ve overpaid for it. The deal was paid for with R500 million in available cash, R250 million from revolving credit facilities and R900 million from the issuance of DMTN bonds. The group loan-to-value ratio is up from 37.4% at December 2023 to 40.2%.

Looking at the South African portfolio as a whole, tenant turnover only increased by 2.1% year-on-year for the five months to May. This is despite a 5.7% increase in footcount. We are walking around in the malls it seems, but we aren’t buying enough. As a further concern, trading density (sales per square metre) fell in both April and May on a year-on-year basis, as did tenant turnover. That’s not the trend you want to see.

Although they are achieving positive rent reversions in the local portfolio, that situation will change if tenant turnover growth doesn’t turn positive again in the aftermath of the elections.

Compare this to the Eastern Europe portfolio – a land of reliable water supply and consumers with some disposable income. With only a 0.5% increase in footcount, there was an 8.7% increase in tenant turnover. These numbers are based on the four months ended April. Unsurprisingly, there are positive rental reversions in that market.

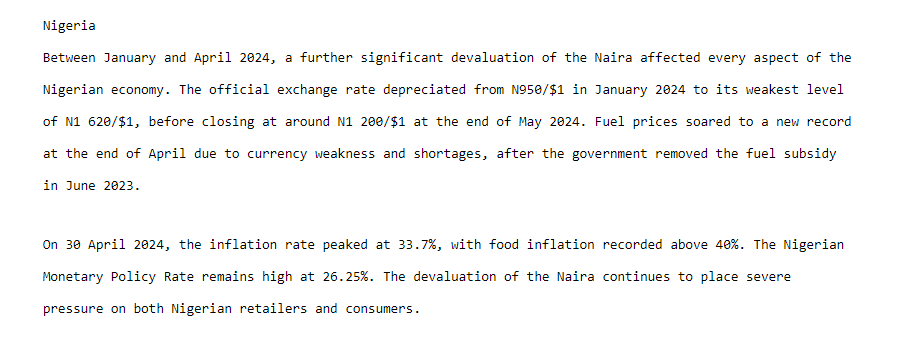

In the sub-Saharan Africa portfolio, Nigeria has been severely impacted by the devaluation of the naira. The political climate in South Africa is full of people arguing that “the markets” don’t matter and that we don’t need a business-friendly GNU. Well, here’s life on the ground when the markets go against you:

Ghana isn’t doing much better, unfortunately.

As a further challenge in Nigeria, the Ikeja City Mall sale didn’t meet the conditions precedent. Hyprop has signed a letter of intent with another party for the entire sub-Saharan Africa portfolio. Fingers crossed.

A dividend for the full financial year will be considered by Hyprop. With not a single mention of Pick n Pay in the pre-close update, that excuse has hopefully run its course now.

A flat profit performance at Invicta (JSE: IVT)

This is despite decent revenue growth

For the year ended March 2024, Invicta reported revenue growth of 7%. That sounds like it should lead to a great result at profit level, but profit was actually 0.5% lower for the year.

One of the reasons is that selling, administrative and distribution expenses were up 10%, with 400 basis points attributable to the acquisition of Imexpart Limited. There were also some asset impairments in this financial year.

A major factor was the significant jump in finance costs from R131 million to R177 million, more than offsetting the growth in equity accounted earnings from Kian Ann, which increased from R152 million to R172 million.

Although HEPS fell by 4% to 470 cents, the group also reports sustainable HEPS with further adjustments for non-trading items. This metric was up 5% to 488 cents, which is why the dividend also increased by 5% to 105 cents per share.

Jubilee is acquiring two more copper assets (JSE: JBL)

The copper strategy in Zambia is going well

Jubilee has significantly increased its copper resource base through two transactions to acquire copper resources that are currently in production (Project M and Project G). The combined value of the deals is $3.85 million. Only $0.25 million is settled in cash, with the rest paid for through the issuance of new Jubilee shares at a 30-day VWAP.

It’s great to see smaller companies being able to use their shares as acquisition currency, as this is one of the key reasons to be a listed company. This is made possible by what the company is achieving in initiatives like the Roan Upgrade.

Jubilee is pushing hard on what it calls its Integrated Copper Strategy in Zambia, which allows for targeting of copper resources ranging from tailings through to near-surface copper reef that is accessible through open-pit mining.

Kore Potash isn’t across the line with PowerChina yet (JSE: KP2)

This is anything but an easy negotiation

Negotiations where so much is on the line are always tricky. Both Kore Potash and PowerChina are heavily invested in the Kola project, with the latter having spent considerable time and resources in putting together the Engineering, Procurement and Construction (EPC) proposal. Of course, for Kore Potash, they are committed rather than just involved in the project. It simply has to work for them.

After meetings in Beijing in May, further important issues were raised around completion and performance guarantee tests. This is because the goal is to achieve a fixed price contract with only minimal variations. This puts the risk on PowerChina. If you’ve followed the South African construction industry, you’ll know that a single bad contract can sink an entire company, so it’s understandable that the parties are taking their time to get this right.

A follow-up meeting has been planned for July 2024.

Another interesting development is that PowerChina has expressed interest in operating the mine after construction, with a draft operating proposal expected to be received in July.

As soon as the EPC is finalised, Kore Potash will need to move forward with raising funds from the Summit Consortium.

The market hated the uncertainty in the news, with the Kore Potash share price closing 22% lower on much higher volumes than an average day of trade, so that wasn’t because of an isolated trade.

The flowery language continues at Orion Minerals (JSE: ORN)

Sometimes it sounds like they are selling tickets to a show

It’s very unusual to see emotive language on SENS. Companies shy away from words like “exceptional” and “outstanding” and with good reason. The use of hype words can turn against you very quickly if things go slower than expected, or aren’t quite as outstanding as was promised.

Nonetheless, Orion has referred to “More Outstanding Hits” – which sounds like a Saturday radio show – at the Okiep Copper Project. Basically, they are excited about the drilling results coming through.

Interestingly, the company notes a slow turnaround time from local laboratories, which gives an idea of the activity in the copper exploration space.

Orion is working to complete the Bankable Feasibility Studies. As the name suggests, these are needed to move forward with financing and further development activities.

Profits have declined at PBT Group (JSE: PBG)

The share price has come a long way off its highs

The PBT Group share price is a good example of why patience can pay off in the markets. Before the pandemic, nobody knew anything about this company. It then exploded onto the scene (and I think launched my career as a ghost to be honest, as writing on this company landed me my first Financial Mail opportunity). After excellent results during the pandemic, reality set in about the sustainable growth prospects and the share price washed away:

In a trading statement for the year ended March, the company has advised that normalised HEPS from continuing operations will be down by between -13% and -7.6%. This is because revenue growth is between -0.1% and 6.1%, with EBITDA expected to be -8.4% to -2.7% lower.

The normalisation adjustment always took into account the treasury shares related to the BEE structure. Those shares have subsequently been classified as ordinary shares in issue, so HEPS from continuing operations without the normalisation adjustment fell by between -26.1% and -21.5%.

The highlight is cash generated from operations, which increased by between 1.2% and 7.5%.

The discontinued operation is PBT Australia, which was disposed of on 30 September 2023.

The PPC CEO doesn’t mince his words (JSE: PPC)

There’s proper tough talk here

If you read PPC’s high level results for the year ended March 2024, you really wouldn’t think that there’s anything to be worried about. After all, revenue is up 20.6%, EBITDA margin expanded by 160 basis points and HEPS swung from a loss of 20 cents to a profit of 19 cents. Bliss, surely, especially when you consider that there’s a dividend of 13.7 cents?

The newly appointed CEO thinks otherwise, noting that “problems are pressing” and that a “meaningful organisational reset and tough decisions” are going to be necessary here. I’m very glad that PPC doesn’t pay my salary, then.

The wording is quite incredible really, with the growth in revenue in the South African and Botswana cement business described as being “marginal” – despite being +5.2%. Materials business did see revenue drop by 6% though. It’s also worth noting that the revenue growth in cement was driven by pricing increases, as volumes were negative.

Of the R502 million increase in trading profit, Zimbabwe contributed R395 million. CEO Matias Cardarelli will clearly be focusing on improving things in the local business, which is exactly why he was the chosen successor. PPC faces major market headwinds like slow economic growth and the problem of imports, so he has his job cut out for him.

Still, I can only admire someone who recognises the problem instead of pretending that it isn’t there. We have far too many executives on the JSE who have become accepting of mediocrity.

Prosus and Naspers achieved eCommerce profitability (JSE: NPN | JSE: PRX)

I like the new CEO and it will be interesting to see where this story goes

Naspers and Prosus have released results for the year ended March 2024. The group has achieved eCommerce profitability in the second half of the financial year, which is a big deal. They are well ahead of the commitment to be profitable in that business in the first half of the new financial year. The fact that the announcement starts with a note on profitability tells you that the winds of change have blown strongly in the group.

Here’s another indication of the changes: the group invested $571 million in M&A in the year, way below the peak of $6.3 billion in 2022 when the previous CEO was all about tight shirts and loose deals. Management is now trying to rectify significant underperformance in the past couple of years, which is what happens when you deploy most of your capital at the top of the cycle. They have $16 billion in capital on the balance sheet, so discipline with that money is key.

I always like to look at the Naspers results specifically to see what’s going on with Takealot Group, which includes Mr D. For this period, gross merchandise value increased by 3% and revenue was up by 8%. Mr D was profitable for the first time, with a trading profit of $3 million for the year. As for Takealot, it reduced losses by $4 million but still isn’t profitable. I also look at Media 24, which suffered an impairment of R280 million in this period as performance is below expectations.

The offshore assets are obviously where the real value lies in this group.

RCL Foods will let Rainbow go on a high (JSE: RCL)

A trading statement shows that Rainbow has been a helpful contributor in this period

With the unbundling of Rainbow by RCL Foods coming up on 1 July, RCL has released what will be its final trading statement that includes references to Rainbow.

For the year ended June, RCL Foods expects HEPS from total operations (including Rainbow) to be at least 75% higher than the prior period. Rainbow has been a major driver of that performance, as has the grocery business which has enjoyed the demise of load shedding in recent months. The sugar business is also doing well. Baking is facing volume and margin pressures though in an extremely competitive environment.

The announcement notes that Rainbow’s trading performance in the second half of the year was broadly in line with the first half, with an interesting comment that retail and wholesale volumes increased while quick-service restaurant volumes softened. It seems that South Africans are eating at home more often, presumably a combination of affordability and the abundance of electricity. Although feed costs increased in the second half of the year and volumes were under pressure in the external feed business, Rainbow navigated this with lower input costs thanks to breed performance and cost control measures as part of the turnaround strategy.

Little Bites:

- Director dealings:

- Various top Nedbank (JSE: NED) executives sold shares in the company worth over R31 million.

- The CEO of Mr Price (JSE: MRP) received share awards and promptly sold the whole lot for over R19 million. The CFO took the same approach to the value of R2.6 million, as did the company secretary to the value of R1.8 million. The company secretary also sold additional shares worth R56k.

- The former CEO of The Foschini Group (JSE: TFG) has sold shares in the company worth R25.8 million.

- An associate of directors of Astoria Investments (JSE: ARA) bought shares in the company to the value of R4.4 million and entered into a CFD trade with a value of just under R5 million.

- A director of a major subsidiary of Novus (JSE: NVS) received share awards and sold the whole lot for R973k.

- Various directors of Anglo American (JSE: AGL) were happy to receive shares in lieu of fees for services rendered, with a total value of around R700k.

- A director of Copper 360 (JSE: CPR) acquired shares i the company worth R22.5k.

- Adrian Gore has entered into replacement hedging transactions over Discovery (JSE: DSY) shares. There are two distinct tranches. The first is a put – call structure expiring mid-2025 at prices of R113.1836 and R168.5769 respectively. The second is a similar structure that expires in March 2026 at prices of R114.3028 and R184.9017. These structure protect against downside below the put price and give away upside above the call price. The current share price is R135. There are 3,000,000 options in total, so the nominal value being hedged is just over R400 million at current prices.

- Trustco (JSE: TTO) has agreed a share repurchase with University of Notre Dame du Lac in the US, which holds 12.8% in Trustco, 0.7% in Trustco Resources and 8.65% in Legal Shield. Each of those entities will repurchase their respective shares from the university. The aggregate value is $5 million. This is a related party deal, so a circular with an opinion by an independent expert will be sent to shareholders in due course.

- Tiny little Visual International (JSE: VIS) released a trading statement that reflects HEPS of 3.33 cents for the year ended February 2024. The share price is only R0.03!

- Putprop (JSE: PPR) announced the results of the odd-lot offer, in which 4,048 shares in the company were repurchased. This took 362 individual holders off the register, holding 0.01% of the shares in issue.

- MC Mining (JSE: MCM) has announced that Godfrey Gomwe is stepping down as managing director and CEO. This comes after the successful offer by Goldway Capital for the company. Don’t feel too sorry for him, as there’s an accelerated vesting of 8,000,000 share options that can be exercised before April 2027. Separately, the company announced the appointment of non-executive director Christine He as interim Managing Director and CEO, effective 1 July 2024.

- Ibex Investment Holdings (JSE: IBX) (the old Steinhoff investment vehicle) has announced the placing of up to 400 million Pepkor shares in the market. This represents 10.9% of Pepkor’s current issued share capital. Ibex currently owns 43.7% of issued Pepkor shares. Ibex may increase the size of the placing subject to demand and pricing. Barclays, Investec and JPMorgan are acting as Joint Global Coordinators and will be picking up the phone to qualifying investors to try place the shares.