Jubilee Metals needs to make a decision soon on the Large Waste Project (JSE: JBL)

They are trying hard to de-risk the potential acquisition

Jubilee Metals had a pretty rough time recently, with production challenges due to electricity issues at the Roan project. These problems are largely behind the group now, which frees them up to work towards making a decision by mid-May on the acquisition of the Large Waste Project in Zambia. This is part of the company’s copper strategy in the country.

The incentive to do the deal is certainly there, as the price has dropped from $30 million to $18 million. If they go ahead, the $11.5 million in remaining consideration for the full deal would need to be settled over 12 months. In deciding whether to exercise the option to acquire the assets, they’ve been busy with extensive due diligence and pilot scale trials. They’ve also locked in an off-take agreement for 10 million tonnes of the estimated 260 million tonnes, valued at $6.75 million. This will give them insight into how the material performs.

You certainly can’t fault their efforts to try and reduce risk on the potential deal, with lots of clever corporate finance strategies at play here.

The Murray & Roberts business rescue plan is out in the wild (JSE: MUR)

This is a very good reminder of the difference between secured and unsecured creditors

When the wheels come off in a business, value moves very quickly from equity holders to debt holders. Equity holders get to enjoy upside potential. In return, they give away downside protection.

Murray & Roberts Limited is in business rescue and is giving us a great practical example of this situation. The straw that broke the camel’s back was De Beers pulling back on its mining capex, which essentially means that Murray & Roberts was a downstream victim of lab-grown diamond disruption! Never, ever underestimate the power of disruption. Of course, this wasn’t the only reason why the group fell over, but it was certainly the finishing touch.

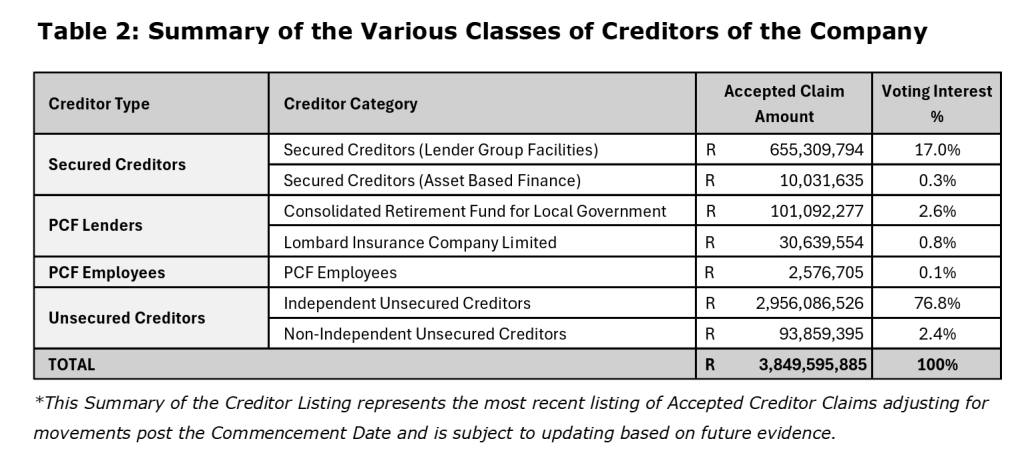

I’ll include a couple of snippets from the full business rescue plan. For example, this table shows you how the various claims against the company are tallied and categorised:

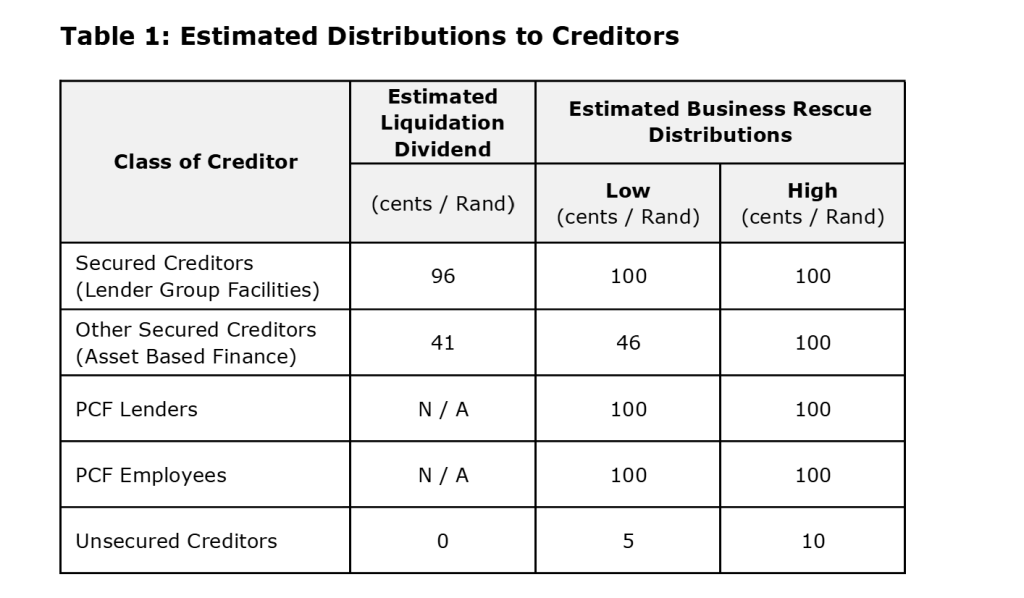

And then this table, which technically appears before the other one, shows you what each type of creditor can expect to receive under the plan:

As you can see, unsecured creditors will lose between 90% and 95% of their money. This means that there won’t be anything left for shareholders, who sit even further down the pecking order than unsecured creditors.

It’s called “business rescue” rather than “shareholder rescue” and now you can see why. So, how will the business be rescued? How will this plan be implemented? An investor named Differential Capital is swooping in on the mining assets. This transaction would facilitate the payment of the creditors as per the table above, while saving the majority of the 2,800 jobs at risk.

As this thing heads to zero, it’s hard not to think back to the ATON offer in 2018 that the board refused to back. Hindsight is perfect of course, but what a terrible journey it has been.

A change in leadership at Orion Minerals (JSE: ORN)

With the DFS reports out in the wild, Errol Smart is passing the baton

Errol Smart has been running Orion Minerals for 12 years. This journey culminated in the recent release of the Definitive Feasibility Studies (DFS) for both the Prieska Copper Zinc Project and the Okiep Copper Project. You might recall that they were released on the same day.

The focus now will be on getting these projects built, which of course means arranging all sorts of things including funding. Smart has decided that this is the moment to hand over the reins, with Tony Lennox (currently a non-executive director) stepping into the role as CEO. He has over 40 years of experience in mining, particularly in project development and operations.

This sounds like a solid succession plan.

Primary Health Properties is trying to seduce Assura shareholders (JSE: PHP | JSE: AHR)

This announcement is designed to give Assura shareholders something to chew on

As things stand, Assura is being pursued by two parties. KKR and Stonepeak are cash buyers, with the Put Up or Shut Up (PUSU – a real thing) deadline having been extended to 11 April. By that date, as the rather blunt name suggests, the parties need to either confirm that they are making an offer, or confirm that they are not making an offer.

I’ve seen the PUSU deadlines get pushed out many times in UK deals, although there aren’t usually two parties involved. I presume that the deadline has more teeth in a potentially competitive process, otherwise what would the point of it be?

The competitive tension in the deal is coming from Primary Health Properties. Hilariously, both Assura and Primary Health Properties are recent additions to the JSE. It seems like the curse of JSE delistings just won’t go away!

Primary Health’s indicative offer is a mix of cash and shares. Including the dividend that Assura shareholders would be allowed to receive, the price implies 46.2 pence per Assura share. Interestingly, if the combination of the groups went ahead, existing Assura shareholders would hold 48% of the enlarged group. Such a deal would create the eighth largest UK listed REIT.

The deal would push the combined group’s loan-to-value ratio above the targeted range of 40% to 50%. The expectation would be to return to targeted levels within 12 to 18 months of the deal being completed.

By now you must be wondering what the competing potential cash offer from KKR and Stonepeak looks like. As a reminder, the last announcement was for an offer to the value of of 49.4 pence per share (including the dividend that Assura shareholders would retain). Primary Health is therefore 6.5% below the competing cash proposal. To further complicate things, the part-share part-cash nature of the Primary Health proposal means that the value fluctuates constantly based on the Primary Health share price.

Normally, you would expect to see the part-share proposal at a premium to a clean cash proposal. I’m not sure that the promises of synergies in a combined group will be enough to get shareholders to put pressure on the Assura board to take this deal seriously.

Nibbles:

- Director dealings:

- Gold Fields (JSE: GFI) directors have made an absolute fortune thanks to the rally in the gold sector. A bunch of directors sold shares worth a total of R38 million. The announcement doesn’t indicate whether this was only the taxable portion of the gains.

- MTN (JSE: MTN) announced various sales by directors, with a mix of taxable and non-taxable portions. In my view, the important thing to highlight is that the CEO retained a portion of the share award and so did a couple of other execs, but most of the participants appear to have sold the full awards.

- The COO of DRDGOLD (JSE: DRD) sold shares worth R2.2 million.

- An associate of a director of Ethos Capital (JSE: EPE) bought shares worth R560k.

- The CFO of York Timber (JSE: YRK) sold shares worth R51k.

- In a rare show of capital allocation maturity among listed property funds, Supermarket Income REIT (JSE: SRI) has elected to suspend its scrip dividend alternative for the latest quarterly dividend. This is due to the shares trading at a discount to the net asset value per share.

- Iqbal Khan, the COO of Brimstone (JSE: BRT | JSE: BRN), has retired from the group due to health reasons. A replacement hasn’t been named as of yet.

- Rebosis (JSE: REA | JSE: REB) is suspended from trading and thus needs to release a quarterly progress report. You may recall the public sale process that the company went through as part of the business rescue initiatives. The update is that all but one of the properties sold through that process have been transferred to the purchasers. The exception is Bloed Street Mall (how’s that for an ironic name?), where the delay is around a dispute on the remaining period of the land lease agreement. The City of Tshwane council is involved here as well.

- Sail Mining Group (JSE: SGP) is another example of a suspended company that has released a quarterly update. After many delays, the audit is underway for the 2022 – 2024 financials. Also, the business rescue plan for subsidiary Black Chrome Mine (Pty) Ltd has been approved. They are moving ahead with a Mine Restart and Trade Out Plan, which is believed to achieve the best outcome for the stakeholders involved.

- Yet another company in the naughty corner is aReit Prop (JSE: APO), a listing that I warned about at the time that it came to market. The price looked like complete nonsense to me and sadly I was proven correct. They’ve also been dealing with some technical accounting issues that led to major delays to the 2023 financials. They now expect to publish them by the end of April. They expect a large impairment to the leasehold properties to be raised. It won’t impact headline earnings or distributable income.

- Nigerian energy company Oando (JSE: OAO) is also on the wrong side of financial reporting deadlines, albeit only slightly. They were meant to publish the 2024 financials by the end of March. An acquisition has delayed this process, as has the introduction of more onerous audit requirements due to a change in legislation. They expect to only get everything done by the end of May 2025.

As at 30 June 2024 Aton owned 43,81% of Murray and Roberts and as far as I know still do. What strategy are they following?

Assuming they still do, and I think they do (although not quite as much as that), the strategy they are following is the wrong one…