")

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Goldway has declared its MC Mining offer unconditional (JSE: MCZ)

There is yet another twist in this tale

The MC Mining soap opera continues, with bidder Goldway announcing that it has in fact met the minimum acceptance condition. This means that holders of at least 50.1% of ordinary shares in MC Mining (other than those already held by Goldway) have accepted the offer.

This is going to come as a surprise to the MC Mining board based on their recent communication (and of course the recommendation they made to shareholders not to accept the offer). To further increase the acceptances , the offer has been extended by 10 business days for acceptance until 11am South African time on 22 April.

MC Mining was unhappy about the extension that they believe came as a surprise. As Goldway very smugly points out, the intention was always to extend the offer once the minimum acceptance condition was met. MC Mining just wasn’t expecting the condition to be met.

MultiChoice announces the terms of the Canal+ mandatory offer (JSE: MCG)

The offer price of R125 is well above the required mandatory offer price

The MultiChoice – Canal+ journey has been interesting. The firm intention announcement by the group includes the timeline of events, starting in February 2024 with Canal+ announcing that it wanted to make an offer of R105 per share. MultiChoice rejected that offer, as the board believed that the price undervalued the group.

It was a brave strategy, but it worked. After Canal+ acquired more shares in the market and triggered a mandatory offer at R105 per share, the parties negotiated further and decided to propose a price of R125 to shareholders. It’s still a mandatory offer, but at a price higher than the minimum regulatory requirement of R105 per share based on the trading history of Canal+ in MultiChoice shares.

This avoids a silly and expensive situation of a mandatory offer followed by an offer at a higher price. It seems like a win for all concerned.

Canal+ currently holds 36.6% of MultiChoice shares in issue and is allowed to buy more shares while the offer is live, provided they don’t pay more than R125 per share or the offer price will need to be increased to whatever the higher amount is.

The very important thing to note is that this is being structured as a mandatory offer rather than a scheme of arrangement. This isn’t an expropriation mechanism that binds all holders to the outcome of a vote that needs 75% approval. Instead, the squeeze-out provisions may apply, which allow Canal+ to force a 100% acceptance provided 90% of holders say yes to the offer.

It is therefore highly likely that MultiChoice will remain listed on the JSE, as achieving a 90% acceptance rate is no joke. There’s potentially a much more interesting outcome here, as the parent company of Canal+ (Vivendi) is considering a split into various entities. If this happens, it seems that Canal+ might be available for a separate spin-off and merger with MultiChoice, which would suddenly create a far more interesting media and entertainment group with a seriously impressive footprint.

The circular to shareholders is due by 7 May 2024 and should make for very interesting reading.

Personally, with no financial horse in this race, I would love to see a MultiChoice – Canal+ merger. It would give local investors the opportunity to hold shares in a proper media powerhouse. I bet there would also be further benefits for the local film industry.

Great for Sasol, perhaps not great for your lungs (JSE: SOL)

This is going to upset the environmental groups

Investors in Sasol have had to stomach a situation where the longevity of Secunda Operations has been in doubt because of environmental concerns. Naturally, environmental groups would love to see the back of this thing, although that would lead to far more boring Sasol AGMs with less disruption. Investors with a purely financial lens just want to see Sasol return to a financially appealing position, with the share price having lost more than a third of its value in the past year.

The right approach, as is so often the case, is probably somewhere in the middle. This is why regulators exist, as they need to balance the needs of all stakeholders. There is always an economic cost that has to be balanced against environmental costs. Sadly, the trade-off is air quality vs. loss of jobs. There are no easy decisions here.

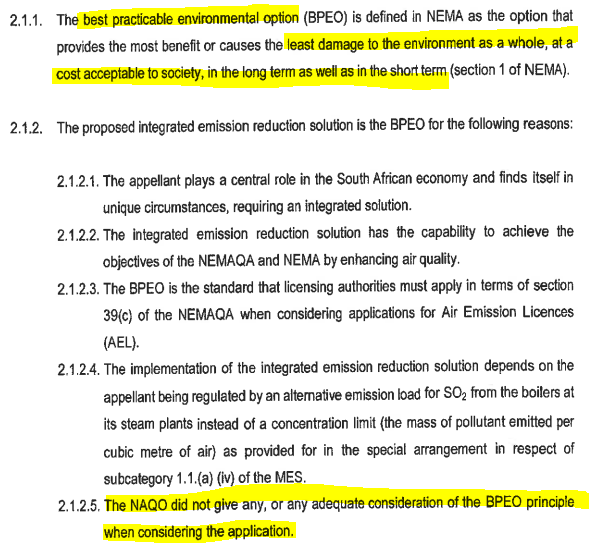

The major recent scare for Sasol was the National Air Quality Officer (NAQO) refusing Sasol’s application to be regulated on an alternative emission load basis for the boilers at Secunda Operations. Sasol’s argument is that they are working hard to reduce the environmental footprint, but shouldn’t be measured against the concentration-based limits.

The Minister of Forestry, Fisheries and the Environment has upheld Sasol’s appeal after the NAQO said no. Load-based limits will be applied from 2025 until 2030.

You can read the full appeal decision here, with this as just one interesting extract dealing with Sasol’s grounds of appeal. It clearly shows how the trade-offs mentioned above come into play:

Sirius makes more progress on its portfolio (JSE: SRE)

This group isn’t shy to do deals

There are many property funds on the JSE that seem to do deals for the sake of it, paying market value for properties and selling at market value as well. That doesn’t really do much to create shareholder value, let’s be honest.

Sirius is more interesting than that. Although I’ve commented many times on how silly the valuation got during the pandemic, that wasn’t a negative reflection on the management team. If anything, the market simply got too carried away.

To help justify the valuation, Sirius tries hard to acquire properties at appealing prices and to dispose at strong prices as well. The group previously announced acquisitions in both Germany and the UK with a total value of over €100 million. These four deals have now been completed. They were paid for with the proceeds of the November €165 million capital raise.

Separately, Sirius has completed the sale of a light industrial asset in Stoke-on-Trent in the UK for £3 million. It’s a small transaction for a non-core asset, with the price set at a 1% premium to the last reported book value.

The share price is up 30% in the past year. Here’s the pandemic craziness I was talking about, clearly visible in this five-year chart:

Little Bites:

- Director dealings:

- The CEO of Primary Health Properties (JSE: PHP) has bought shares worth nearly £69k.

- Powerfleet (JSE: PWR), the newly merged group with MiX Telematics, has gotten its locally listed life off to a complicated start thanks to accounting rules. The group needs to restate the accounting treatment of convertible preferred instruments. This will require restatement of financials for the 2021 and 2022 financial years as well. This has non-cash impacts on the financials. Still, it makes the group late in filing its annual report, which earned the company a warning letter from the Nasdaq giving it 60 calendar days to respond. They definitely need to get this sorted in the required time period, as a listing suspension is not the way to win the trust of investors.

- To give you an idea of the cost of borrowing for sub-scale REITs in Europe, Deutsche Konsum (JSE: DKR) is issuing subordinated secured convertible bonds in euros. The repayment date is October 2025, so this is very short-term money where the convertibility into shares is important. They pay interest at 12% per annum and with an issue price of 98.5% of the nominal amount, the effective rate is actually slightly higher. Compare this to the yields on properties and you’ll see the problem.

- Four non-executive directors have resigned from Ellies (JSE: ELI), so things are going from bad to worse there it seems.