Listen to the podcast to get the details on these insights from December 2024:

- Is Italtile’s share price a Christmas miracle?

- Bloisi’s first acquisition at the helm of Prosus is a fascinating one in Latin America

- Renergen was the most interesting announcement in the dead week between Christmas and the new year, revealing yet another risk for the business

- Metair’s selling price for the Turkish business has all but evaporated

- Bell’s share price may prove to be a cautionary tale about greed, with regret surely kicking in for those who voted against the scheme at R53 per share

The Ghost Wrap podcast is proudly brought to you by Forvis Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Forvis Mazars website for more information.

Listen to the podcast here:

Transcript:

1. Italtile’s share price: a Christmas miracle?

If you’re still looking for a Christmas miracle, then look no further than the Italtile share price. At this stage, I’m more likely to believe in Santa again than in the reasons why this stock is trading at a close to 52-week highs.

Management has given the market nothing but an honest appraisal of the state of play in the manufacturing side of the business – and it’s not good, as South Africa has an overcapacity of tile manufacturers, leading to revenue in that part of the business dropping by a further 1.6% between 1 July and 30 November. That’s after it fell 5.9% in the base period, so that’s particularly ugly over two years.

In director dealings announcements in the past few months, directors have been selling shares, so there’s another strong bear indicator. And if you’re hoping that the retail sales side will give you something to hang onto, then you would need to be happy with just 2.2% growth in system-wide sales.

I can only imagine that investors are hoping for interest rates to drop further and the two-pot system to filter through into home improvement projects. I would remind you at this point that hope is not a strategy.

I’m long Cashbuild in this sector and if you draw a 1-year chart, you’ll see that Cashbuild caught up the performance differential in December very nicely against Italtile:

If Italtile was more liquid, this would be quite the fun pairs trade I think, with my view being long Cashbuild and short Italtile. Instead, I just have to be content with my long Cashbuild position, something that I’m still happy with as we head into 2025 because they do not have a manufacturing side to their business.

As for Italtile, don’t be surprised if there’s a big shock in the market when results are released in March. You certainly can’t claim that management didn’t warn you, all while the share price is close to 52-week highs. It just doesn’t make sense to me.

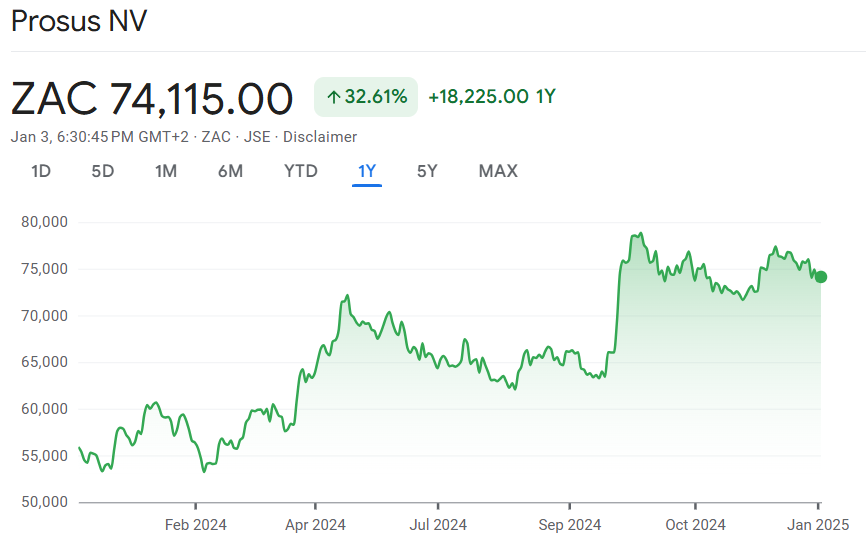

2. Bloisi pulls the trigger on Despegar for Prosus

Just before Christmas, Prosus announced the acquisition of Despegar in Latin America. Now, this is particularly interesting as recently appointed CEO Fabricio Bloisi has tons of experience in that region. That’s where he built iFood, a company that he subsequently sold to Prosus.

This hardcore experience as a successful founder and scaler of businesses is exactly why I’m a fan of Bloisi. It’s not just me – the Prosus share price is up 32% in the past year:

Now, we need to avoid making the mistake that people make all the time in Africa, which is assuming that a continent is actually just one big country. iFood was built in Brazil and Despegar was founded in Argentina. Importantly though, Despegar has scaled across Latin America, so I do think that Bloisi’s Brazilian expertise (and certainly his Latin American network) is helpful here in assessing this deal.

Either way, Bloisi clearly liked what he saw and Prosus is pulling the trigger on a $1.7 billion acquisition for what is described as a leading online travel agency. Weirdly, it suddenly sounds less exciting, doesn’t it? As you imagine Flight Centre at scale and shake your head, consider how valuable it is to have higher income South American consumers constantly on your platform, particularly in a region where the likes of Mercado Libre have shown us how powerful a platform can be.

If you want to be depressed about what Takealot has built vs. what can be built, just take a look at Mercado Libre’s story. Perhaps some of that DNA is in Despegar as well?

In terms of pricing for the deal, Prosus is paying a revenue multiple of just over 2.4x and that’s after offering a 34% premium to the 90-day VWAP (Despegar is listed). I think that’s a reasonable price for a platform in a high growth market. Let’s see how this plays out. This is Bloisi’s first big acquisition in charge and the market will hold him accountable for it.

3. Renergen: here’s another risk to add to the list

Between Christmas and the New Year, Renergen was the only announcement that I felt was particularly interesting. The company’s fight with Springbok Solar is heading to court in February 2025 for an interdict application. This really does seem like a bit of a ridiculous issue right now where someone is behaving badly. Renergen certainly wants us to believe that it is Springbok Solar, and once it gets to court, we will find out for sure.

In the meantime, Renergen needs to run their business and get access to more money for near-term liquidity. They hope to conclude negotiations in the first quarter of 2025 to get their hands on that cash.

Of course, what would help tremendously is if helium production was going smoothly. The latest headache (and yes there is another one) in this regard is that there wasn’t a helium iso container available in South Africa for a direct fill, so there’s yet another risk that you can add to your bear case for this business model. Renergen tried to mitigate this using an onsite storage container and although there were some challenges, they reckon they’ve got a solution now.

The teething issues continue, the company needs money on a regular basis and they have an awkward battle in court on the horizon. Things are never boring at Renergen, that’s for sure.

With the share price down 53% in the past 12 months and recently making new 52-week lows, they desperately need an improvement in momentum and the market will watch each of these issues very closely.

4. Metair is anything but a Turkish Delight

I finish off with cautionary tales and there are two of them. They are both in the industrials space and they are both strong reminders about risk in the markets, something you should always keep in mind.

The first is Metair, where the amount of money they are getting out of Turkey just kept getting smaller and smaller – and then even smaller! In fact, it’s now down to just $1 million, with the potential for it to be $2 million depending on how things play out as the deal closes. When the deal was first announced in September, which is just a few months ago, the price on the table was $110 million! They talked about the price being subject to customary adjustments for working capital and net debt.

Now, such adjustments are indeed customary, because as the balance sheet evolves every single day, you’re not sure how it will look when the deal closes and you make an adjustment at the time – nothing unusual. But what isn’t customary is the rate at which the Turkish business was absolutely obliterating its balance sheet. This is why the purchase price basically disappeared into nothingness. It’s also why Metair took steps to accelerate the deal, before they found themselves in a position where they were paying someone to carry the dead business away.

Owning businesses in faraway lands can be very risky, especially in countries where they have major macroeconomic concerns. With Metair’s share price down 43% in the past 12 months, at least that particular nightmare is behind them. If they can just have a bit of positive luck this year, something they’ve seen very little of recently, perhaps the share price chart can start heading the other way.

5. Is regret kicking in yet for Bell Equipment shareholders?

The second and final cautionary tale is Bell Equipment, where I am genuinely concerned about where this ends for the minority shareholders who wanted to accept the take-private deal and weren’t able to because the scheme failed.

The price on the table was R53 per share. Currently, it’s trading at just over R40 – well down from there!

An updated trading statement in December gave the unfortunate news that HEPS is expected to be at least 40% lower for the year. This suggests HEPS of up to 478 cents and quite possibly lower. The offer price of R53 would’ve been a forward earnings multiple of 11.1x based on that HEPS number. As HEPS could come in lower, the multiple might have been higher.

Will shareholders who didn’t vote in favour of the scheme end up kicking themselves? Only time will tell of course, but there’s got to be some kind of lesson in here about greed. Even if Bell does get back to those share price levels at some point, the mining cycle will need to play out accordingly and that could take years.

The old adage in the markets is worth remembering as we head into a new year of opportunity: the bulls make money, the bears make money and the pigs get slaughtered.

In 2025, don’t be a pig! Be a bull, be a bear, learn, be as consistent as you can – and most of all, join me for another fun year in the markets!

Was the initial Metair Turkey selling price indeed USD 110 million?

Hi! Yes, shockingly it was – the SENS announcement of 17 September with the detailed terms of the deal disclosed that as the selling price.