I promise that this isn’t designed to depress you. It is, however, designed to make you think. Sometimes, we have to think about things that are sub-ideal.

There was a time in this world when a single income household with 2.4 children could enjoy a perfectly adequate middle-class lifestyle. The kids were in decent schools and if they showed real academic ability, further studies were possible. There was enough money for a family holiday now and then. You get the idea.

Today, there are many dual-income households with crazy working hours, a threat to “rather chop it off” than have a third child and so much stress that mental health has been thrust to the forefront of our existence.

What the hell happened?

Whatever the reasons, people are getting tired of making more people

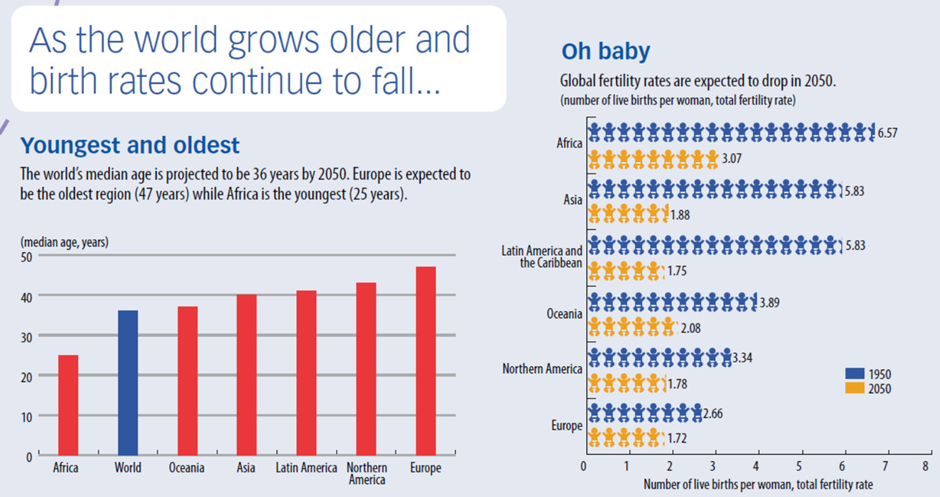

The United Nations reckons that on 15 November 2022, the world population reached 8 billion people. No, I’m not sure how they can be so precise, but anyway. It took 12 years to get from 7 billion to 8 billion. That same organisation reckons it will take 15 years to get from 8 billion to 9 billion, which means the rate of population growth is slowing significantly.

I wonder why that might be the case? Could it have anything to do with the ridiculous costs of having children and struggling to enjoy a similar standard of living to those a few generations earlier? I found this fascinating chart on the IMF website:

There’s obviously a really great humanitarian story underneath all of this, which is that mortality rates have plummeted as we’ve gotten far more advanced at keeping babies alive in even difficult circumstances. That’s a very good thing and it means that mothers don’t need to have more kids than they actually want, just to make allowance for terrible things that can happen. I just don’t think it fully explains the drop in birth rates and what people go through to have kids these days.

How did we get to this stage?

In 1950, the same IMF article that had the above chart tells me that the world had 2.5 billion people. From everything I’ve read and been told by older family members with a naughty look in their eyes, the sixties was a time of boosting the global population, usually at rock concerts. Either way, there are now more than three times the number of people on the planet and that’s in the space of seven decades, which means many people have seen that increase in their lifetimes.

It’s not like we have more space all of a sudden, so this explains why real estate costs have become ridiculous and very few people can have the typical suburban home that their parents enjoyed. Climate change is at the forefront of many conversations, perhaps because the same planet is now trying to support far more humans than ever before.

Despite Elon Musk’s opinion on the matter and certainly his practical approach to solving it, there are probably just too many humans.

What does this have to do with retirement, or lack thereof?

Assuming you went to university and that you plan to retire at 65, you’ve basically got 40 years to earn enough money to fully sustain yourself for 20 years (or more) after retirement.

Welcome to adulting.

During those 40 years, you’re probably going to have kids. That’s going to do things to your expenses that you never believed possible. Statistics aren’t really on your side in terms of divorce rates either, so that’s another potential financial nightmare. This is before we’ve even considered healthcare challenges, or the desperate need to manage your mental health through lifestyle upgrades and experiences, or your cat ripping up your brand-new rug.

You’re in a fight over a finite set of resources on the planet, with an increasing number of humans who need them.

40 years, you say? To make enough money for the next 20 or more? That’s a big ask, especially when it seems like humanity is hell-bent on using Artificial Intelligence to drive even more people into unemployment.

It’s all in the maths

To make this equation work, the retirement industry and many personal finance influencers focus on getting you to drink less coffee, thereby saving more of your income (before fees of course) in your early years and ensuring that you have a bang average 85 years on this world. This is because you’ll have very little spare money in the best years of your life, all so that you can afford Wimpy every Wednesday when you’re too old to remember what proper food tastes like anyway.

If we all knew precisely when we would die, it would be a lot easier to just work out exactly how much money we need and spend all the rest before our kids do. This is unfortunately not possible, even for the most dedicated Diamond members on Vitality.

I believe there’s another way, but you’ll have to buckle up and get ready for a wild ride to get it right.

Retirement is for salaried employees, not entrepreneurs

The biggest problem with the concept of retirement is that it assumes that at the age of 60 or perhaps 65, you suddenly become a useless amoeba who can’t add value to anything or anyone beyond falling asleep at the appropriate time after family lunches. This simply isn’t true.

If you can extend your ability to earn an income, then the maths starts to look very different indeed. Instead of hoping to live off passive income, you’re supplementing it with an active income. If you really get it right, then you’ll be living off the active income entirely for quite some time past the age of 60.

How do you do this? Well, a corporate is going to force you to retire at some point, so you then have to hope that you have a skillset that lends itself to some kind of consulting role. That’s really not easy to get right. I have some bad news for you on how useful many corporate skills are in the world outside of air-conditioned offices with full solar power backup.

When I made the decision to leap from corporate life into the very uncertain world of entrepreneurship, one of the things I imagined is how great it would be one day to perhaps have a business that can earn an income without me being involved all the time. That’s a semi-retirement that literally delivers the best of all worlds, with ongoing income and perhaps most importantly, a sense of purpose and something to keep my brain alive into hopefully much older years.

The lesson here? Learn continuously, keep your skillset relevant and be alert to opportunities to build income away from your salary. Perhaps most importantly, make sure your career is built around something you genuinely enjoy and can see yourself doing for many years. I can tell you for sure that these things are a lot more fun than cutting your coffee intake.

Great article. I am fascinated by the simplicity of this article. I also am reading it with the concepts of minimalism, downsizing, technology and preferment – coined by Felicia Mabuza-Suttle, that retirement is not as scary as it was purported to be.

I really do believe that working on a skill that (1) makes money and (2) makes you happy is the very best thing that anyone can do. Then you don’t want to run away from it at the age of 60!

Hi

Downsize and asset management?

Regards

For sure. I think those are givens in any retirement strategy. In general, avoiding wastefulness that doesn’t really make you happy and maximising returns on capital are key.

I think you need to account for the taxes you will have to pay, too.

Just about from cradle to grave, sadly.

Highly entertaining article and very true, however unfortunately it is really only a very few people that can realistically transform their day jobs into something that can keep them actively earning decent income post-retirement.

Absolutely right. It’s difficult and something that people need to think about early in the process! Being too reliant on corporates is very dangerous.

Don’t buy retirement annuities. Invest in yourself.

Maybe both 🙂

Definitely both. You get tax relief with a retirement annuity and you definitely will not regret having one once you retire.

We’ve been entrepreneurs for the past 25 years or so. One of us is now 66; the other 76. We’ve run our business successfully for nearly 30 years, built up a good reputation for it, and sustained ourselves and a small staff complement. We’ve recently started drawing on pension funds and annuities and, while they are not sufficient to fully sustain us, they help considerably. So does cutting down expenditure such as when a large, apparently reputable insurance company imposed a 15% annual premium increase on our life policy from this year in order to sustain the death benefit promised to us donkey’s years ago. So we cancelled it and ploughed the full amount into clearing the remaining bond of our property asset, so that when one of us departs this mortal coil, the other will have a fully paid asset to sell at market level prices of the day. Annoying to lose all that money we’ve ploughed into the life policy over the years, but we really felt we had no option. In the meantime, we both continue to work at the business to supplement our income. We have lots of other activities and good friends to keep us busy and interested and our health is pretty good. So, for now it’s working.

Right, I love it. Straight and simple. It comes a bit late to cause me the panic and anxiety it will no doubt inflict on the already messed up under-40s. Instead, I now feel lucky to be counting my days. I am forwarding the letter to my laatlammetjie, young adult, university-going kids. They don’t listen when I tell them there’s a bogey man under the bed, but they sure appreciate a good piece of writing. Hopefully, this letter will help them slay (the bogey-man).

Thanks for the kind words! I don’t have the solution for any of us. All I know is that the longer you can have an income for, the better your chances. Lifelong learning is key.

You have not taken ill health into account.

In what way do you mean? The risk of ill health in retirement? That’s why saving for retirement and having medical cover is so NB. I’m definitely not suggesting that people shouldn’t save for retirement.

A very well written letter and also a harsh reminder of us to make sure we do whatever it takes to plan for our retirement.

Thanks!

If you were reading this article it is probably likely that you fit into the demographic that PPS covers. According to a seminar of their’s that I attended if you reach age 65 you have a 50% chance of making it to the 100 year mark.

Frightening. Truly.

What a great article. It highlights a part of life that most people will reach, but unfortunately find themselves ill prepared for. Of course, without financial security other aspects of life become heavily constrained. However, Ghost’s point of establishing a “sense of purpose” is of equal significance.

The dream of spending one’s retirement days perpetually on a golf course sounds romantic but, in reality, it is unsustainable. In an ideal world, I would hope that when i retire I can access an environment which grants access to a community and, more importantly, a reason to stay mentally lucid; irrelevant of what that environment may look like . For different folks, that will look entirely different: part-time job, volunteer work, learning magic; whatever blows your hair back.

My belief is the next big entrepreneurial moment resides in creating opportunities to easily access these types of environments and some form of coaching course to prepare for the twilight years of retirement.

That’s a clever idea Craig – build it!

I loved this article and its insights, and as a 31-year-old who only started investing and planning for retirement last year, the economy and the value of our money have made me very depressed at times. I know I am better off than most but with a huge pay gap in where my age mates are and often articles stating that you should have started at your 20s can be off-putting, but this was a real-life picture of the difficult reality many of us will face in the future

Starting early certainly helps because of the compounding effect of money. But I also firmly believe that your best shot to stay relevant in this world is to have experiences, like travel etc. So there’s a balance. You’ll be fine 🙂

Very cool article, as always Ghost. Another scary thought of retirement is the question around “will I have enough”? I was fortunate to start in corporate quite young and have been “ahead” of others for as long as I know. Last week was the 1st time I got an amber traffic light on a member benefit statement. Scary.

It’s crazy. There is something deeply wrong with the world right now and the pressures on working families.

I agree with Craig. Not just Coaching Course for ex youngsters.

The gap between “too old to work-too young for pension” is an avenue that needs to be explored too.

Lots of knowledge and skill goes a-begging when we retire.

HR people unite.

Yes, the Taxes. The parasites keep sucking until you drop dead.

Having recently been forced into “early retirement” (retrenched) at 58, surviving on a passive income only is not an option. Starting up a new venture is the only option but means that the source of future passive income might need to be the conduit through which the new active income is generated. Scary as hell!

A great article ! Thanks Ghost.

A crucial element apart from the financial side is definitely retaining mental stimulation. You retire on Friday and on Monday, have a feeling of all that accumulated knowledge and experience being worthless.

It’s been noted by others that retirees need to find something that gives them both pleasure and income .. And find it before retirement day arrives.

Best wishes to all of us for the future.